Debt Snowball Method: How It Works and When to Use It

The debt snowball method is a way to pay off many loans by clearing your smallest balance first, while paying only the minimum on the rest. Once the smallest loan is gone, you add that money to the next smallest. Each loan you clear frees up more money for the next one.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

KEY TAKEAWAYS

The debt snowball method lists your loans from smallest balance to largest, and clears them in that order. It ignores the interest rate.

Clearing your first small loan quickly gives you a real win early, which helps you keep going.

Research on borrowers who focus on one account at a time, starting with the smallest, found they stayed more motivated and got out of debt faster than those who spread money across every loan.

As per RBI’s latest Financial Stability Report, India’s household debt stood at 41.3% of GDP at the end of March 2025, remaining above its five-year average.

Debt Consolidation may combine eligible debts into a single EMI, depending on the approved loan terms.

What Is the Debt Snowball Method and Why Does It Work?

The debt snowball method is simple. You line up all your loans from the smallest amount owed to the largest. You pay the minimum on every loan so none of them fall behind. Then you put every extra rupee you have onto the smallest loan until it is fully paid off. After that, you move to the next smallest.

The name comes from a snowball rolling downhill. It starts small and picks up size as it goes. Your repayment works the same way. The money you free up from one cleared loan gets added to the next one, so your paying power keeps getting bigger.

Here is the honest part. On paper, this is not the cheapest way to clear debt. If two loans have very different interest rates, paying the smallest balance first can mean you pay a little more interest overall. So why do people still use it?

Because paying off debt is not only about maths. It is about staying in the game long enough to finish. When you clear that first small loan in a month or two, you feel something move. That feeling is what keeps most people going. Research that followed borrowers found that those who put their money into one account at a time, starting with the smallest, stayed more motivated and cleared their total debt faster than those who chipped away at everything at once.

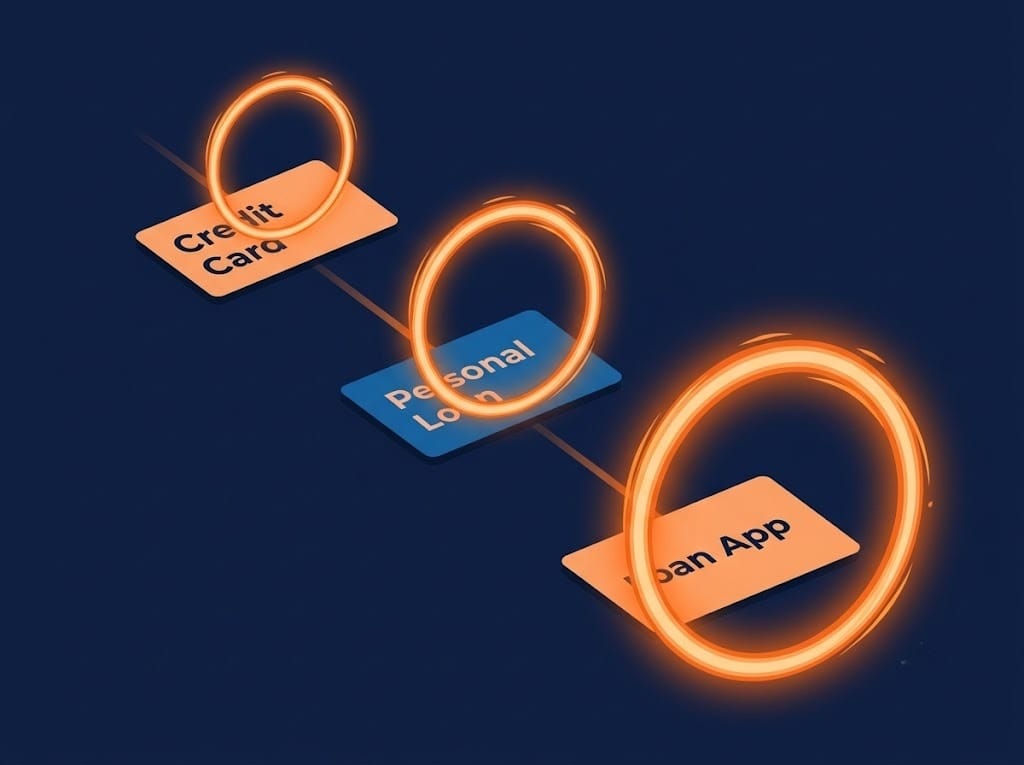

This matters in India right now. By the end of 2024, household debt had reached around 42% of GDP, up sharply over five years. And nearly half of people with a credit card or personal loan were also carrying at least one more active loan. Many people are not managing one debt. They are managing three or four at the same time.

Feeling buried under three or four EMIs?

FREED's Debt Consolidation Program can combine them into one lower monthly payment, 100% online.

Check If I QualifyHow Does the Debt Snowball Method Work, Step by Step?

The best way to understand it is with a real example. Say you have three unsecured debts:

- A BNPL (buy-now-pay-later) balance of ₹8,000

- A loan app balance of ₹22,000

- A personal loan balance of ₹65,000

Your minimum payments across these three might come to around ₹9,500 a month. On top of that, suppose you can spare an extra ₹4,000 each month after your household costs.

You keep paying the minimum on the loan app and the personal loan. Then you throw your extra ₹4,000, plus the small BNPL minimum, at the ₹8,000 BNPL balance. At roughly ₹5,000 a month, that balance clears in under two months.

For example, BNPL is gone, but you do not spend that ₹5,000. You roll it onto the loan app. Its minimum was around ₹2,500, so now you are putting close to ₹7,500 a month on the ₹22,000 balance. It clears in about three months.

Then you roll the whole thing into the personal loan. Your paying power has grown from ₹5,000 to ₹7,500 to well over ₹13,000 a month. The biggest loan, which felt impossible at the start, now has the most money hitting it.

That is the snowball. Each loan you finish makes the next one easier. The numbers here are only an example. Your actual minimums will depend on your loans, but the method stays the same.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

What Are the Advantages of the Debt Snowball Method?

The biggest advantage is emotional, and that is not a small thing. When you are tired and stressed, seeing one full loan disappear gives you proof that this can work. On a modest extra amount of ₹3,000 to ₹5,000 a month, a small balance of ₹10,000 to ₹15,000 can be cleared in two to four months. That early win is often what stops people from giving up.

There is also a mental load benefit. Every open loan is one more due date, one more app, one more thing to remember. When you close a small account, that is one less thing on your mind. Fewer open accounts means fewer chances to miss a payment by mistake.

The method is also easy to run. You do not need a spreadsheet or any knowledge of interest maths. You just sort your loans by size and follow the order. It works even when your spare money is small, because the whole point is to build the habit and let it grow.

The one honest limit is that it is not tuned for interest savings. If one of your loans has a very high rate, you may pay a bit more by clearing a smaller, cheaper loan first. For many people that small extra cost is worth it, because a method you actually finish beats a cheaper method you abandon halfway.

FREED Expert Tip

Not sure which of your loans is actually the smallest? Pull your Experian credit report through FREED's Credit Insights to see all your outstanding balances in one place before you start.

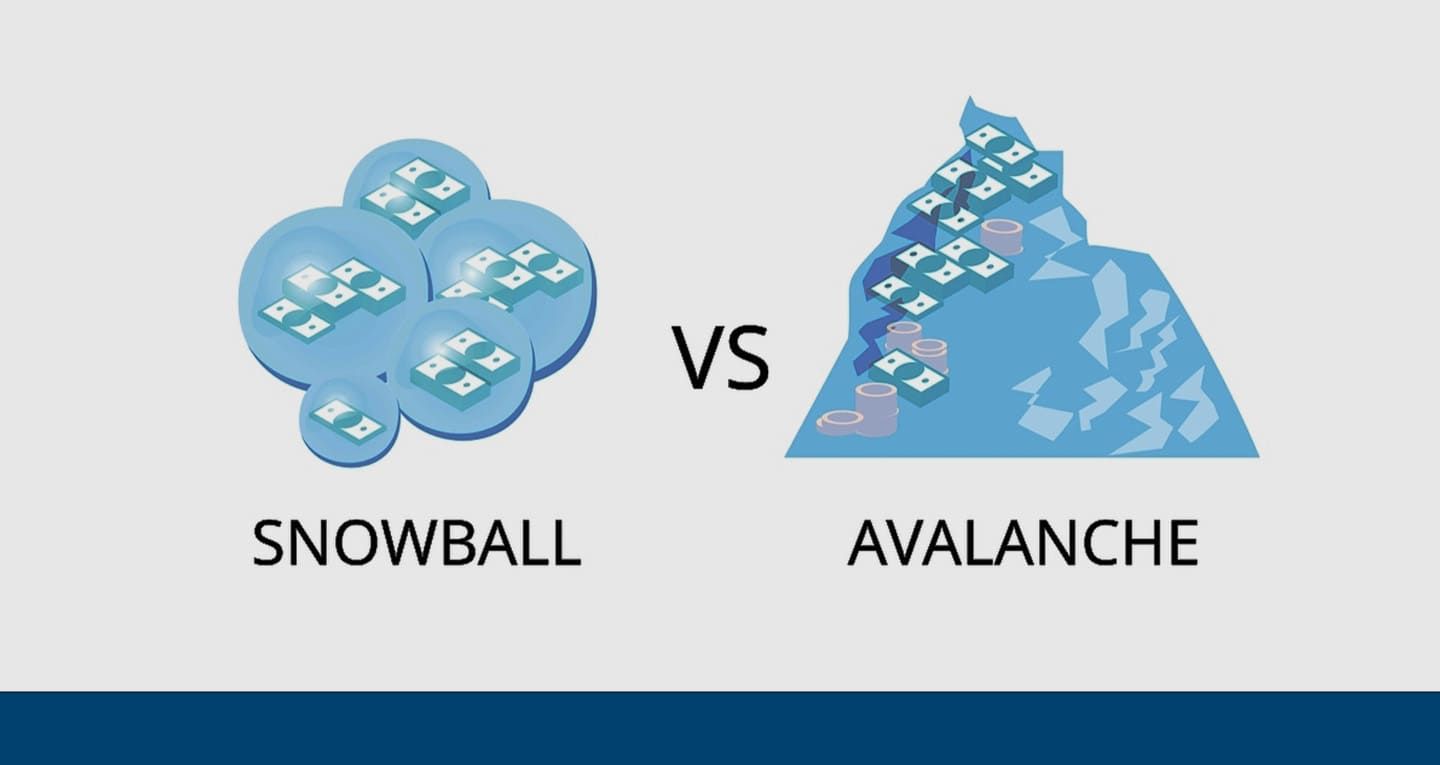

Check Your ScoreDebt Snowball vs. Debt Avalanche: Which One Should You Use?

These are the two main ways to pay off several loans, and they differ on one point: which loan you clear first.

The debt snowball starts with the smallest balance. The debt avalanche starts with the highest interest rate. The avalanche saves you more money, because you kill your most expensive debt first. On paper, it wins.

But paper is not real life. The avalanche can ask you to grind away for months on a big, high-rate loan before you see a single account close. If you lose motivation and stop, the maths advantage means nothing. The snowball gives you a visible win early, which is why more people who start it actually finish it.

So the choice comes down to what your real problem is. If your problem is staying motivated, the snowball is usually the better fit. If your discipline is strong and your loans have very different interest rates, say a credit card charging a much higher rate than a personal loan, the avalanche can save you real money. Neither one is right for everyone.

A small time difference in payoff rarely justifies picking the harder path if that path is the one you are more likely to quit. We have a full comparison if you want to go deeper into the numbers.

When Does the Debt Snowball Method Stop Working?

The snowball method has one requirement. You need at least a little spare money each month after paying every minimum. When that is true, it works well. The trouble starts when it is not true.

The first sign is when your balances are too large to move. If your loans run into lakhs and your extra money is a few thousand rupees, the smallest loan can still take a long time to clear. The early win that keeps the method alive never arrives.

The second sign is when your income barely covers the minimums. If there is no surplus at all to redirect, the snowball has nothing to roll forward. It stalls before it starts.

The third sign is when interest is growing faster than you can pay it down. High-rate credit card dues can build up month on month, so the balance you are chasing keeps refilling itself.

The fourth sign is when one or more accounts are already in default or close to it. At that point you are no longer trying to pay smart. You are trying to stay afloat.

A useful line to check yourself against is the EMI burden. If a significant share of your income is already committed to EMIs, or your debt has become difficult to service with your current income, a DIY repayment strategy alone may not be sufficient. As a rough guide, if your total unsecured debt is more than about 12 months of your take-home pay, the snowball alone is unlikely to break the cycle. None of this is a moral failure. It is a structural problem, and a structural problem needs a structural fix. The good news is there are real options, and we will walk through them next.

What the Law Says

If you start falling behind and recovery calls begin, know your timing rights. The RBI has told banks and NBFCs that recovery agents must not call you before 8:00 AM or after 7:00 PM for overdue loans. Any call outside that window is a violation you can report. (Source: RBI notification, 12 August 2022.) If calls turn abusive or threatening, FREED Shield can help you understand your rights and document what is happening.

Know Your Recovery RightsWhat Are Your Options When the Snowball Method Isn't Enough?

If the snowball has stalled, you have real choices. Here they are, from the softest to the most structural.

Option 1: Free up more money to feed the snowball. Before changing anything, look for a bit more surplus. A cut in non-essential spending, or a small side income, can lift your extra amount from ₹3,000 to ₹6,000 a month. Sometimes that is enough to get the smallest loan moving again and restart the snowball.

Option 2: Bring your many EMIs into one lower EMI with debt consolidation. If you are still paying your EMIs but you are stretched thin across several loans, consolidation is built for exactly this.

FREED's Debt Consolidation Program looks at your full financial picture and matches you to a suitable lending partner from its network. That partner gives you one new loan, which instantly pays off all your existing unsecured loans and credit card dues. You are left with one loan, one lender, one due date, and one EMI that is lower than what you were paying across everything before. It is a 100% online process, and FREED charges a fee only when the consolidation is completed. Debt consolidation may simplify repayment for eligible borrowers, depending on repayment behaviour and lender reporting. If you have missed an EMI or two and are not sure whether you qualify, FREED's team can assess your situation in a free call and tell you what options are open to you.

Option 3: Loan settlement, only as a last resort. This one is different, and it is not for everyone. Settlement is not something a borrower chooses out of preference. Banks only consider it when you are in a genuine financial difficulty and are truly unable to repay the full amount, usually after you have already defaulted. In a settlement, the bank agrees to accept a reduced lump sum as full and final payment, and the loan is marked as "Settled". FREED helps borrowers settle their unpaid/overdue loans at up to 50% less*, and the account is reported as 'Settled' on your credit report. The reporting period is determined by the credit bureau's policies. Consolidation and settlement are for two very different situations, and they should never be mixed up. If you are still paying, consolidation is your path, not settlement.

Rates and ranges shown are indicative. Final terms decided by the bank. FREED is not a Loan Provider. No outcome is guaranteed. Please verify directly with your bank.

Too many EMIs? There's a smarter way to manage them.

FREED combines all your loans into one lower EMI, 100% online.

Check If I QualifyHow to Start the Debt Snowball Method (Step by Step)

- 1

List every unsecured debt you owe.

Write down the outstanding balance, the minimum due, and the lender name for each one. This gives you a clear, honest starting number.

- 2

Rank them from smallest balance to largest.

Ignore interest rates for now. Sort by the amount owed only, because the order is what makes the method work.

- 3

Set the minimum payment on every debt.

Keep all accounts current so none of them slip. Keeping all minimum payments current helps maintain a consistent repayment history that future lenders may consider.

- 4

Put all your extra money on the smallest debt.

Even ₹2,000 to ₹3,000 extra a month creates real movement on a small balance and gets you your first win faster.

- 5

Roll the freed-up payment into the next debt.

Once the smallest is cleared, add that whole amount to the next loan's minimum. This is the step that makes the snowball grow.

- 6

Repeat until every debt is cleared.

Each loan you finish makes your paying power bigger, so the method speeds up on its own the further you go.

Debt Snowball vs. Debt Avalanche: Quick Reference

Feature | Debt Snowball | Debt Avalanche |

Order of payoff | Smallest balance first | Highest interest rate first |

Interest savings | Lower (not the cheapest) | Higher (best on paper) |

Motivation | High, early wins keep you going | Lower, first payoff can take longer |

Best for | Borrowers who need visible progress | Disciplined borrowers with wide interest rate gaps |

Complexity | Very simple | A little more tracking needed |

Completion rate | Higher (backed by research) | Lower if motivation fades |

Both of these methods assume you can still make your payments. Neither one handles debt that has already gone into default. If you have missed EMIs and the balances are not moving, talk to FREED. Structured options like consolidation exist for exactly that situation.

Sources

Claim in blog | Verified source (opened and confirmed) |

Recovery agents must not call borrowers before 8 AM or after 7 PM for overdue loans | RBI notification RBI/2022-23/108, DOR.ORG.REC.65/21.04.158/2022-23, 12 Aug 2022 — rbi.org.in |

India household debt around 42% of GDP by end-2024; nearly half of credit card / personal loan borrowers hold another live loan | RBI Financial Stability Report, December 2024 — rbi.org.in FSR archive |

Borrowers who focus on one account at a time, starting with the smallest, stay more motivated and clear debt faster | Kettle, Trudel, Blanchard & Häubl (2016), "Repayment Concentration and Consumer Motivation to Get Out of Debt," Journal of Consumer Research 43(3); popular write-up: Trudel, HBR (Dec 2016) |

Softened (no regulator doc, left out of table per sourcing rule): credit card rates "often around 36% a year" and personal loan rates spread — written as market-typical, not sourced facts.

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions