What is debt consolidation and how it helps reduce monthly financial stress

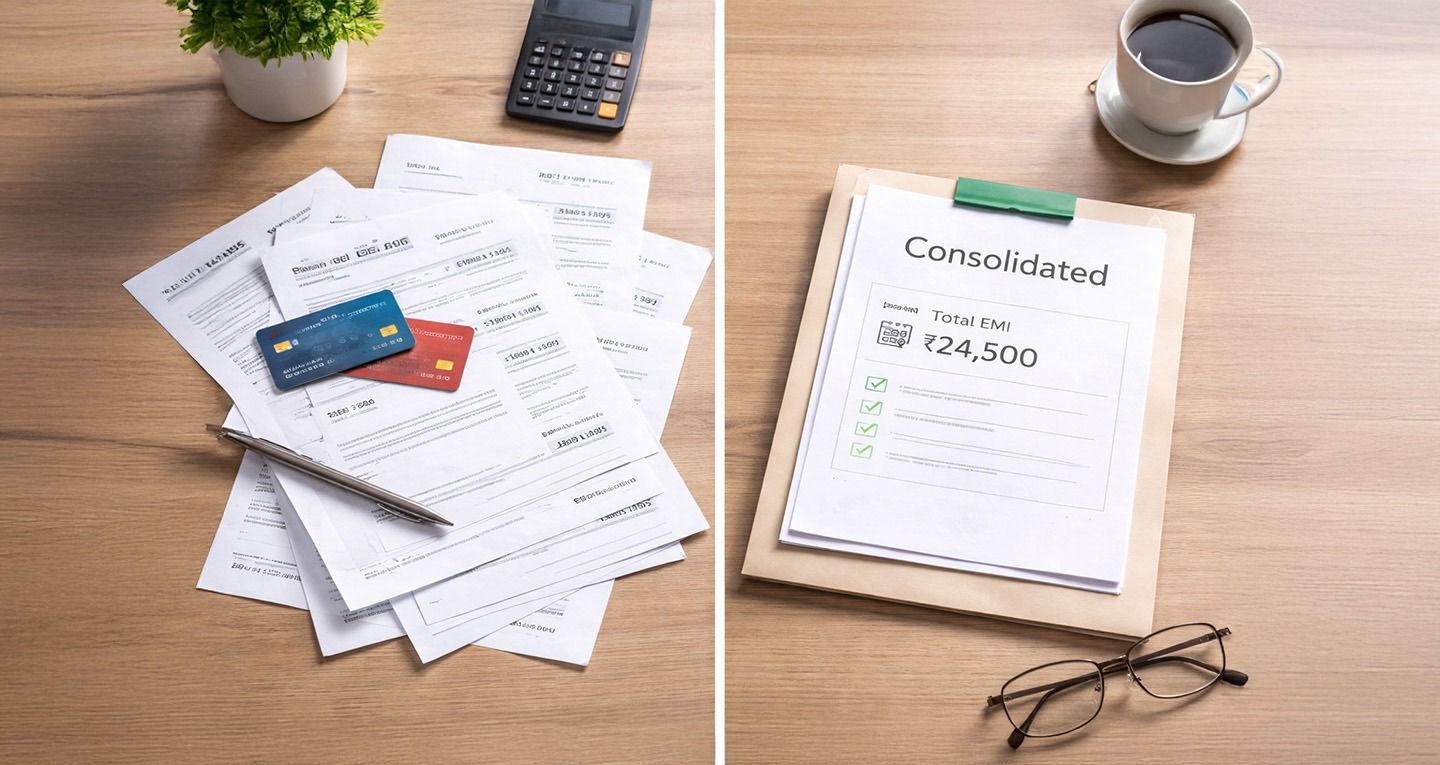

Debt consolidation is when you take out a new loan to pay off multiple (existing) loans. You will take the multiple EMIs that you currently have to pay each month and turn them into 1 single loan, with 1 single EMI each month.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Introduction

You’re juggling three EMIs (equated monthly installments), two credit cards, and dozens of different due dates. You're not the only borrower in India!

Many borrowers in India find it to be extremely difficult to keep track of multiple loans, when they try to manage multiple loans they frequently lose control over paying off their loans. You have different interest rates; Different due dates; daily increasing penalties; Overall they add to your mental and financial stress, and that’s where loan debt consolidation in India can help you.

But first let’s talk about what it actually means and how it will help reduce your financial pressure each month.

What is debt consolidation?

Debt consolidation is when you take out a new loan to pay off multiple (existing) loans. You will take the multiple EMIs that you currently have to pay each month and turn them into 1 single loan, with 1 single EMI each month.

NOTE: The loan debt consolidation doesn’t eliminate your debt, but it consolidates them into one loan so you can pay your bills in a much more manageable way.

For example:

If you have multiple personal loans and credit card debt, you can take out a loan called a consolidation loan (which is typically a personal loan), and use that larger loan to pay off the smaller loans and credit card debts at once and then at the end of the month you would only send in one payment/EMI to that bank.

It simplifies your repayments process as shown in the example above; in many cases it reduces your stress.

Debt Consolidation Motivation

Common reasons for seeking loan consolidation include:

- Many installment payments (EMIs) each month with different payment due dates.

- High-interest credit card debt.

- Difficulty keeping track of payments to various lenders.

- Increased late fees and penalties for missed payments.

- Financial stress as a result of poor planning.

When loan repayment becomes too difficult, consolidation makes things more straightforward.

How Debt Consolidation Operates in India

To receive a debt consolidation loan in India, you will typically apply through a bank or a non-banking finance company (NBFC). Lenders generally take into consideration your:

- Income level

- Credit score

- Current debts

- Capacity to repay

If approved, lenders will provide borrowers with the funds to pay off existing loans. Once existing loans are paid off, the borrower will only have to make payments on their loan, as all loans have now been consolidated.

It is usually not possible to borrow additional funds during the consolidation process; this is done for the purpose of establishing a solid financial position.

Key Features of a Debt Consolidation

1. Combining Current Loans

You combine multiple individual loans or unsanctioned debt balances (like credit cards) into one liability rather than needing to keep track of several payments, just one.

2. One Payment Per Month

One EMI (Equated Monthly Installment), one due date, one lender.

Reduces confusion about payments and is more likely to cause on-time payments than having several EMIs from different lenders.

3. Possibly a More Advantageous Rate on Interest

Credit card interest can be extremely high in India. By borrowing through personal loans with a lower interest rate, you could lower the total amount of interest you pay out over time.

Your credit score and your ability to pay back the loan will impact whether or not this is advantageous.

How will Consolidation of Loans lessen Financial Pressure?

To demonstrate how, let’s consider the following breakdown:

1. Full Understanding of Repayment Terms

Once you have consolidated all of your loans into one, you will have a single point where you can view everything you owe. You will have better control over beginning a new budget.

2. Improved Chance of Paying on Time

Each loan you have has its own EMI date, and since you will not receive a reminder about a loan paid off and you might have more than one EMI due at that time, your chances of paying on time will increase when you only have to remember one EMI due date each month.

3. Reduction in Mental Stress

Financial stress is not just money; it is lack of or a feeling of no certainty in one's finances. When all of your debts are consolidated, you feel a greater level of financial security since you are taking a fully structured approach to pay off your debts.

4. Improving your Credit

If you properly manage your consolidated loans, you will be able to establish a positive new credit habit that can build your credit. If your credit score does not show a positive trend or if you feel as though your credit history has not improved as substantially as you had hoped, you can contact FREED and get a copy of your credit score and determine whether you qualify for loan consolidation.

A Definitive Guide to Consolidating Debt Through Debt Consolidation in India

- You will begin this process by compiling a list of all your debts currently owed, including the balance left on each loan, the respective interest rate, and the EMI for that loan.

- By reviewing your credit report and score, you can identify what kind of rate you may be able to qualify for an interest on your new debt.

- You should always compare the rates of your current loans against the rate for a consolidation loan so as to determine if consolidating your loans will reduce your interest payments.

- It is important to apply for your consolidation loan through a lender that you have vetted or worked with via an advisory service.

- After you pay off your old loans be sure to obtain closure letters or No Dues Certificates from those lenders.

When you are looking to consolidate debt the best time to consider it is when you are in a good position with your employment, collecting multiple EMIs each month, have a credit score that is above average, and/or have high-interest rates on the loans you are currently carrying.

If any of these factors you are struggling with and/or if you are already in serious default on one or more of your existing loans or under significant pressure to pay off your loans a loan settlement may be a better option than a loan consolidation.

FREED offers a comprehensive review of your specific situation to determine whether a debt consolidation or loan settlement would be the best options available to you and to help proceed with the appropriate course of action.

Mistakes to Avoid

Some common mistakes made by borrowers are:

- Getting a new consolidation loan but using their credit cards excessively as well.

- Not comparing the total cost of repaying a bought financial product.

- Choosing a long time period without estimating the total amount of interest.

- Applying for a loan before checking credit score.

Applying to several lenders at one time (this will hurt credit score because of many hard inquiries).

Using Debt Consolidation is a strategy, cannot use it as a quick fix.

Debt Consolidation

Always calculate the total amount that will need to be repaid on your loan, in addition to your monthly payment.

- Do not raise your living expenses after doing consolidation.

- Don’t have more than one repayment plan in place at any time.

- Make sure to behave responsibly with your credit after doing consolidation.

- Review your credit report at least once every three months.

Your Financial stability comes from your discipline and habits, not from restructuring.

The FREED Methodology

If you aren't certain if debt consolidation, debt restructuring or loan settlement is right for you, FREED can provide structured education for citizens struggling with their finances.

Through FREED, we can:

- Help you understand your overall financial situation

- Discuss different debt consolidation options

- Assist with legal debt settlement (if required)

- Help you find ways to improve your credit score

FEED Expert can help you understand all of the options available and help you decide before taking on an obligation to your financial future.

The Final takeaways

The act of consolidating multiple debt liabilities into one monthly EMI does not mean to run away from debt; it means to help you plan your payments into something easier to follow.

By changing all of your debts into one structured EMI, you will save money because you will not have as many accounts to manage, which means less confusion and lower levels of anxiety regarding payment amounts and dates.

If you have multiple EMIs and feel overwhelmed or stressed about the amount of money due each month, take a moment to evaluate your situation with the help of FREED, find out what type of debt you currently have, and choose a path forward that will help protect your long-term financial stability.

Debt can be reduced and managed effectively with good time-management skills!

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions