How Debt Consolidation Can Improve Your Financial Management

Paying 3-4 EMIs to different banks every month - on different dates, at different interest rates? There's a simpler way. Debt consolidation brings all of it into one payment - and often costs you less in total. Here's exactly how it works.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

Debt consolidation means combining all your loans and credit card dues into one single loan, with one lower EMI and one due date every month.

According to the RBI's Financial Stability Report (December 2024), nearly 50% of Indian borrowers with a credit card or personal loan also have at least one other active loan running simultaneously.

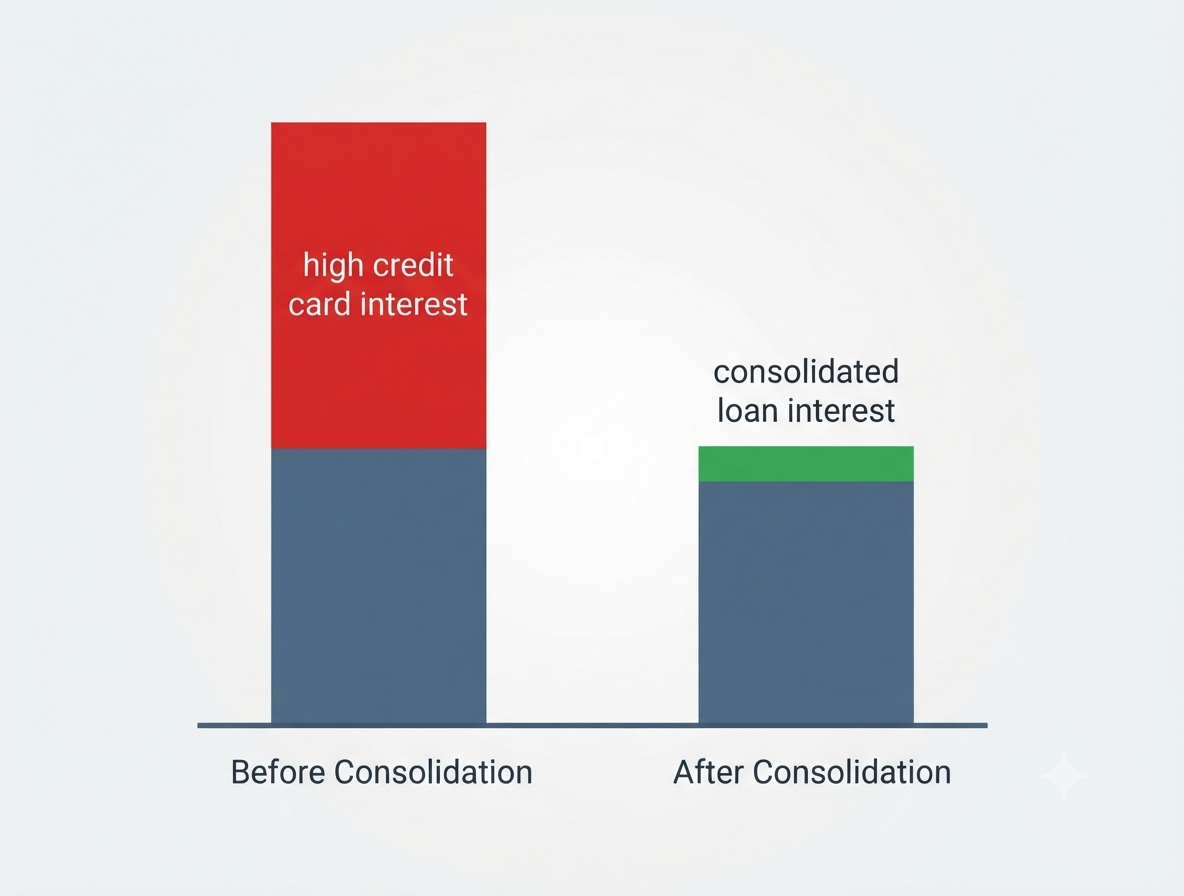

Consolidation typically reduces your interest cost because the new consolidated loan rate (14–20%) is much lower than credit card interest (36–42%).

Managing one payment instead of many reduces the risk of missed payments, which protects and gradually improves your CIBIL score.

FREED's Debt Consolidation Program connects you with lending partners and handles the entire process, so you don't have to run between banks.

How Common is Managing Multiple Loans in India?

More common than most people realise.

According to the RBI's Financial Stability Report of December 2024 nearly 50% of Indian borrowers who have a credit card or personal loan also have at least one other active loan running at the same time. That means roughly half of all unsecured loan borrowers in India are juggling two or more debts simultaneously.

Different banks. Different EMI amounts. Different interest rates. Different due dates. Different customer care numbers to call when something goes wrong.

That is a lot to manage even for someone who is financially organised. For someone who is already stretched thin, it is a recipe for missed payments, late fees, and a CIBIL score that keeps dropping.

Debt consolidation solves this problem directly. It doesn't reduce what you owe. But it makes repayment dramatically simpler - and often cheaper.

What is Debt Consolidation?

Debt consolidation means taking one new loan and using it to pay off all your existing loans and credit card balances.

After consolidation:

- All your old loan accounts are closed

- You have one new loan with one EMI

- You pay one amount, on one date, to one lender

That is the entire concept. One payment instead of many.

- The new consolidated loan usually comes with:

- A lower interest rate than your existing high-interest debt

- A fixed monthly EMI that doesn't change

A clear repayment timeline, you know exactly when you'll be debt-free

How Debt Consolidation Works - A Simple Example

Meet Ravi. He has three credit cards and two personal loans.

Debt | Monthly Payment | Interest Rate |

Credit Card A | ₹3,000 (minimum) | 38% per year |

Credit Card B | ₹2,500 (minimum) | 42% per year |

Credit Card C | ₹1,800 (minimum) | 36% per year |

Personal Loan 1 | ₹5,200/month | 22% per year |

Personal Loan 2 | ₹3,800/month | 18% per year |

Total | ₹16,300/month | Varies |

Ravi consolidates all of this into one personal loan at 15% interest. His new single EMI: ₹11,500 per month.

Result: He saves ₹4,800 per month. Over 2 years, that is ₹1,15,200 in reduced outgo plus significant savings on interest.

He also has only one due date to remember. One bank to deal with. One payment to set up on auto-debit.

His stress reduces dramatically. His CIBIL score starts recovering. And he has a clear date when the debt will be completely gone.

That is what debt consolidation does.

Key Benefit 1: One Payment, One Due Date - Simplicity That Protects You

Managing multiple due dates is harder than it sounds.

The 5th - Credit Card A. The 10th - Personal Loan 1. The 15th - Credit Card B. The 20th - Personal Loan 2. The 25th - Credit Card C.

One busy month. One overlooked reminder. One account without enough balance. And suddenly you have a late payment, a late fee, penalty interest, and a CIBIL score drop.

Debt consolidation removes this risk entirely. One payment. One date. Set up one auto-debit and you are protected for the entire tenure.

This simplicity is not just convenient. It is a structural protection against the missed payments that quietly damage credit scores over time.

Key Benefit 2: Lower Interest Rate: Real, Measurable Savings

This is the financial engine of debt consolidation.

Credit cards in India charge 36-42% annual interest. High-interest personal loans from app-based lenders can be even more. These are among the most expensive financial products available.

A consolidated personal loan through a bank or NBFC typically comes at 14–20% per year - sometimes lower for strong profiles.

The difference is massive.

Example: Outstanding credit card balance of ₹80,000 at 38% annual interest. Interest cost per year at 38%: approximately ₹30,400. Interest cost per year at 16%: approximately ₹12,800. Annual saving from consolidation: approximately ₹17,600.

That is not a small number. On larger outstanding amounts, the saving is even more significant.

More importantly - at lower interest, more of each EMI goes towards reducing the actual debt rather than just servicing interest. You get out of debt faster on the same monthly payment.

FREED Expert Tip

Before consolidating - calculate the break-even point. Add up the processing fee on the new loan and any foreclosure charges on the old loans. Divide that by your monthly interest saving. That is the number of months it takes to "earn back" the fees through savings. If your remaining loan tenure is longer than that - consolidation saves you money. If it is shorter - it may not be worth it.

Talk to FREED

Key Benefit 3: Protects and Improves Your CIBIL Score

Multiple loans create multiple opportunities for missed payments. And missed payments are the single biggest driver of CIBIL score drops.

When you consolidate, you reduce multiple risk points to one. One payment. One chance per month to either protect or hurt your score.

And when that one payment is set up on auto-debit, your score starts recovering through consistent on-time payments month after month.

There's another effect too. When you close multiple credit card accounts as part of consolidation your outstanding on those accounts drops to zero. This reduces your credit utilisation ratio, which is 30% of your CIBIL score. Lower utilisation = better score.

Most people who consolidate responsibly see their CIBIL score start improving within 3–6 months. This opens doors to better interest rates and financial products in the future.

Key Benefit 4: Emotional Relief: Less Stress, Clearer Mind

This benefit is real, even if it doesn't show up in a spreadsheet.

Living with multiple loan EMIs is mentally exhausting. The constant calculation "Which one is due this week? Do I have enough in this account? What if I run short?"

The anxiety before every due date. The shame of a missed payment. The dread of collection calls.

Debt consolidation removes the complexity. One payment. One date. One amount you know is going out. That clarity - knowing exactly what you owe and when you'll be done - provides genuine emotional relief.

People who consolidate often describe it as a weight being lifted. Not because the debt disappeared - but because the noise disappeared.

What the Law Says

Under RBI's Fair Practices Code, any lender offering a consolidation loan must disclose the full Annual Percentage Rate (APR), which includes the interest rate plus all processing fees, GST, and other charges - before you sign any agreement. The advertised interest rate is often not the full picture. Always ask for the APR, not just the interest rate, before agreeing to any consolidated loan. This is your legal right.

Talk to a FREED CounsellorHow to Make Debt Consolidation Work for You

Consolidation is a tool, not a magic fix. Its effectiveness depends entirely on what you do after.

- 1

Compare loan options carefully before committing

Look at the interest rate, processing fee, tenure, and prepayment terms. Calculate the total cost, not just the monthly EMI. FREED's Debt Consolidation Program does this comparison for you across our lending network, so you see the best available offer for your profile.

- 2

Stay disciplined after consolidation

This is the most important point. Once your credit cards are paid off through consolidation, do not start using them for daily expenses again. This is the most common reason people end up worse off after consolidating. The cards now have zero balance and feel "free" but using them recreates exactly the problem you just solved. Use them for one

- 3

Anchor everything in a monthly budget

Consolidation reduces your EMI. Use the freed-up money wisely, some towards an emergency fund, some towards savings. Don't let the reduced EMI become extra spending money. That defeats the purpose.

- 4

Build a small emergency fund with the savings

The reduction in monthly outgo gives you cash that wasn't there before. Even ₹1,000–₹2,000 per month into a separate emergency account builds a buffer. This prevents the next unexpected expense from sending you back to a credit card.

When Consolidation Is the Right Choice: And When It Isn't

Consolidation works well when:

- You have 2 or more active loans or credit card dues

- Your combined EMI is more than 40% of your monthly income

- Your CIBIL score is above 650, making you eligible for a new loan

- You are still paying but finding it very hard to manage multiple payments

- The new loan's interest rate is meaningfully lower than what you're currently paying

Consolidation may not work when:

- Your CIBIL score has already dropped below 650 due to missed payments - you may not qualify for a new loan

- You've already paid 70%+ of your loan tenure - interest is largely already paid, the saving will be minimal

- The foreclosure penalty on your existing loans eats up the interest saving

- You've already defaulted on multiple accounts - debt settlement may be more appropriate

Not sure which applies to you? FREED's free first consultation answers this in one call.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

How FREED's Debt Consolidation Program Works

FREED's Debt Consolidation Program is built for people who are managing multiple loans but need one lower, simpler monthly payment.

Step 1 - Free Consultation We understand your full debt situation - all loans, interest rates, income, and expenses. No fees. No commitment.

Step 2 - Eligibility Check We check your profile against our network of lending partners. We identify the best available rate and tenure for your specific situation.

Step 3 - You Get One Clear Offer We present you a consolidation loan offer, showing your new single EMI, the rate, tenure, and your exact debt-free date. You decide.

Step 4 - All Loans Are Paid Off The consolidation loan amount clears all your existing loans and credit card balances. Those accounts are officially closed.

Step 5 - One EMI Every Month One lender. One date. One fixed amount. That's it.

Throughout the process, if any recovery agent contacts you, FREED Shield protects you immediately.

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions