The Complete Guide to Debt Management Plans - What They Are and How They Work

Loans piling up and no clear way to manage them? A Debt Management Plan can give you a structured path to repay your debts - without panic, without confusion. Here's everything you need to know.

FREED India

Reviewed by FREED India, SEO Intern

Key Takeaways

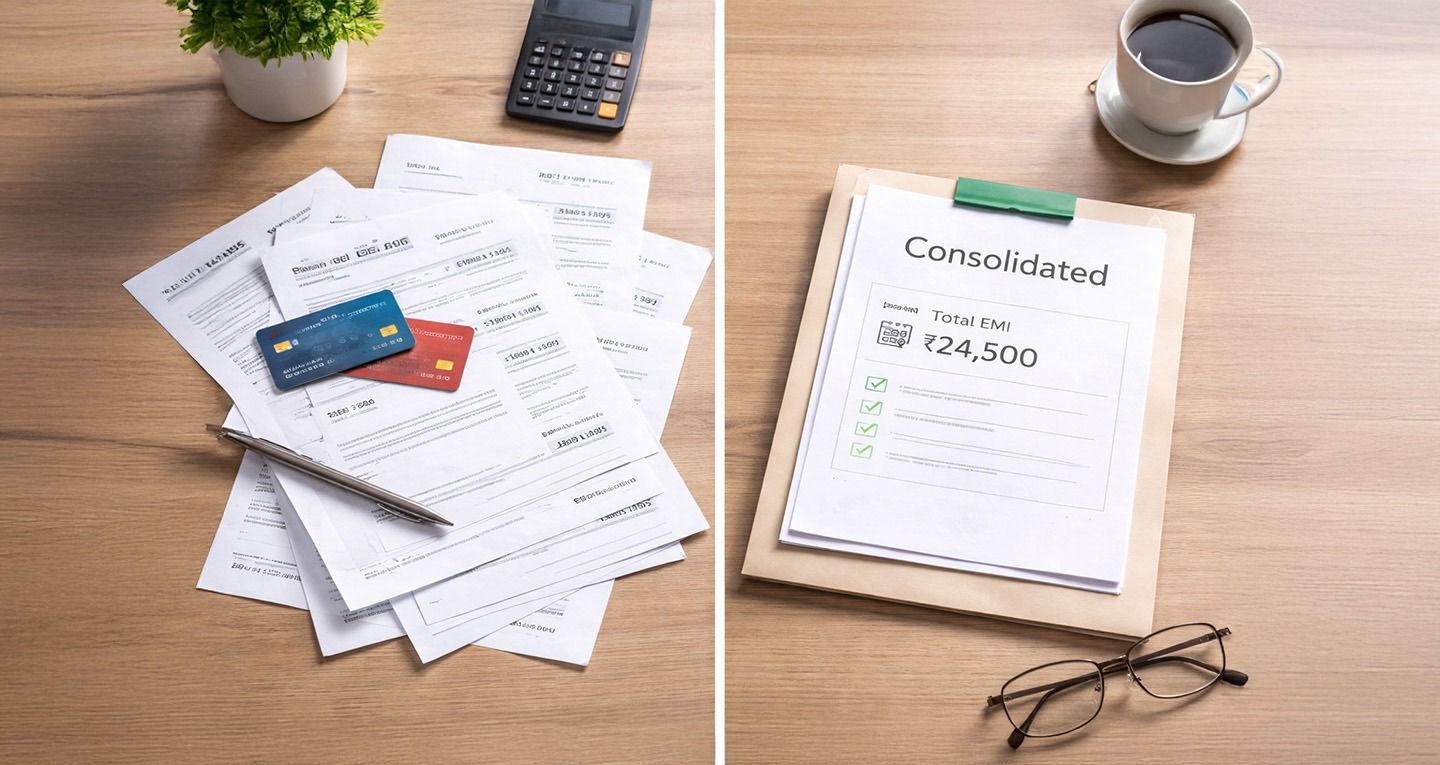

A Debt Management Plan (DMP) is a structured repayment strategy - you pay your full debt back, but in a more organised, manageable way that fits your income.

DMPs work best for unsecured debts - credit cards, personal loans, app-based loans. Secured loans like home loans are generally not included.

A good DMP includes budgeting, repayment prioritisation, creditor negotiation, and ongoing counsellor support - not just a payment schedule.

DMPs are a long-term commitment - typically 12–36 months. They require financial discipline and consistency to work.

If you can still repay but feel overwhelmed - a DMP is a strong first step. If you genuinely cannot repay in full - debt settlement may be more appropriate.

What is a Debt Management Plan?

A Debt Management Plan - or DMP - is a structured plan to repay your debts in a way that fits your actual income.

It is not about getting out of paying. You still pay everything you owe. What changes is how you pay - in an organised, prioritised, and realistic way that doesn't break your monthly budget.

Think of it as a financial GPS. You're still going to the same destination - debt-free. But instead of taking a chaotic, stressful route - a DMP gives you a clear, step-by-step path.

A DMP typically involves:

- Understanding your full debt picture - all creditors, all amounts, all interest rates

- Building a monthly budget based on your actual income and expenses

- Deciding which debts to prioritise and in what order

- Sometimes negotiating with creditors for reduced interest rates or waived penalties

- Making consistent monthly payments - and tracking progress

You can create a DMP on your own. Or you can work with a certified debt counsellor who helps build and execute the plan - which tends to be more effective, especially with multiple creditors.

Who is a Debt Management Plan For?

A DMP is not for everyone. It works best in a specific situation.

A DMP is right for you if:

- You have a regular monthly income - however modest

- You can afford to repay your debts - but need a clearer, more organised way to do it

- Your debt is mostly unsecured - credit cards, personal loans, app-based loans

- You haven't yet missed many payments - or have only recently started missing them

- You want to avoid any further damage to your CIBIL score

A DMP may NOT be the right fit if:

- You genuinely cannot repay the full outstanding amount

- You have already defaulted for 3+ months with no income to pay

- You need the debt amount itself to be reduced, not just reorganised

- In these cases - debt settlement or debt consolidation may be more appropriate options

The key question is this: "Can I repay what I owe if I had a clear, structured plan?" If the answer is yes - a DMP can work. If the answer is no - talk to FREED about settlement or consolidation.

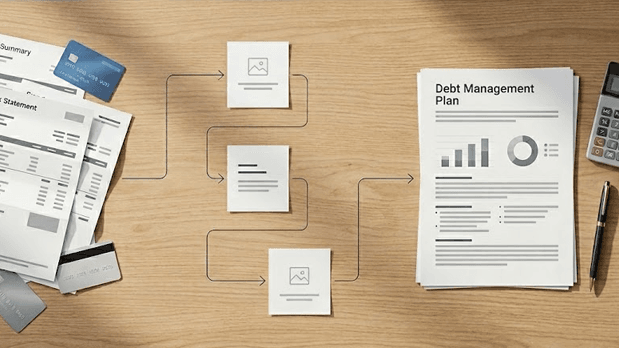

How Does a Debt Management Plan Work - Step by Step?

- 1

Step 1 - Know Your Full Debt Picture

List every debt you have. For each one, write down: Lender name Total outstanding amount Monthly EMI or minimum due Interest rate Payment due date Whether it is secured (home loan, car loan) or unsecured (credit card, personal loan) This exercise alone is powerful. Most people carrying multiple debts have only a rough idea of what they owe in total.

- 2

Step 2 - Build a Realistic Monthly Budget

A DMP only works if your monthly payments fit your actual income. Write down your monthly take-home income. Then list all fixed expenses - rent, school fees, essential utilities. Then list variable expenses - groceries, travel, eating out. What remains after all expenses is available for debt repayment. This number is your starting point. If this number is very small

- 3

Step 3 - Prioritise Your Debts

Not all debts are equal. Some cost you more than others. Prioritise based on: Urgency - which lender is likely to take action soonest? (accounts in late payment are more urgent) Cost - which debt has the highest interest rate? (credit cards at 36–42% cost you the most) Consequence - which debt has the worst outcome if not paid? (secured

- 4

Step 4 - Negotiate With Creditors if Needed

Many people don't know this - but creditors can sometimes be negotiated with to: Waive accumulated penalty interest Reduce your interest rate temporarily Accept a revised repayment schedule Pause penalties while you get back on track This negotiation works best when you approach the lender proactively - before the account goes into default - and show them a realistic repayment

- 5

Step 5 - Make Consistent Monthly Payments

The DMP only works if you follow through - every month, without fail. Set up auto-debit for every payment. Keep your budget updated. Track your progress monthly. Celebrate small wins - every cleared account is a step forward. The most common reason DMPs fail is inconsistency. Life gets in the way. One month is missed. Then another. The plan falls

What Types of Debt are Covered in a DMP?

Included in a DMP (Unsecured debt):

- Credit card outstanding balances

- Personal loans

- App-based instant loans

- Consumer durable loans (phone, TV, appliance EMIs)

- Medical bills (in some cases)

Not typically included in a DMP (Secured debt):

- Home loans (secured against property)

- Car loans (secured against the vehicle)

- Gold loans (secured against gold)

- Loan against property

Secured loans have their own resolution mechanisms (like the SARFAESI Act) and are generally handled separately. A DMP focuses on unsecured debt - where there is no collateral involved.

Benefits of a Debt Management Plan

1. Clarity and Structure Instead of multiple EMIs, multiple due dates, multiple lenders to worry about - a DMP gives you one clear plan. You know exactly what you owe, in what order to pay, and when you'll be done.

2. Financial Discipline A DMP teaches - and enforces - the habits that prevent future debt problems. Budgeting. Prioritising. Tracking. These skills stick long after the debt is cleared.

3. Potential Interest Reduction If your counsellor negotiates with creditors - you may get penalty interest waived or your rate reduced. This directly reduces the total amount you repay.

4. Credit Score Protection Unlike settlement - a DMP that is executed well (consistent on-time payments) can actually improve your CIBIL score over time. Lenders see you making regular payments, which is positive behaviour.

5. Counsellor Support You don't figure this out alone. A certified debt counsellor guides you - answers your questions, helps you stay on track, and adjusts the plan if your situation changes.

6. Legal Protection During the Process A DMP with a professional provider gives you a degree of protection against escalating creditor actions - as long as you are making payments under the plan.

Limitations You Should Know

1. Long-Term Commitment A DMP typically runs for 12–36 months. It requires consistent discipline throughout. This is not a quick fix.

2. Restrictions on New Credit While in a DMP - you should not be taking on any new credit. No new loans, no new credit cards. This is necessary to make the plan work - but can feel restrictive.

3. Not Suitable for Secured Loans DMPs cover unsecured debt only. If your biggest problem is your home loan or car loan - a DMP alone won't solve it.

4. You Still Pay the Full Amount A DMP does not reduce your debt. You pay everything you owe. If your income is genuinely too low to cover even restructured payments - a DMP won't be enough and settlement may be necessary.

5. Requires a Trustworthy Provider Choosing the wrong DMP provider - one that charges high upfront fees without delivering - can make your situation worse. Research carefully before committing.

DMP vs Debt Settlement vs Debt Consolidation - Which is Right for You?

These three options are often confused. Here's the clearest comparison:

Debt Management Plan | Debt Settlement | Debt Consolidation | |

Do you pay full amount? | Yes | No - less than owed | Yes - but as one lower EMI |

CIBIL score impact | Positive (if done right) | Negative (Settled status) | Minimal to positive |

Works when | Can repay, need structure | Cannot repay in full | Multiple loans, need simplicity |

Debt amount reduced? | No | Yes - significantly | No |

New loan involved? | No | No | Yes - one new loan |

Best for | Organised repayment of full debt | Genuine hardship, cannot repay | Multiple EMIs, CIBIL still decent |

What to Look For in a DMP Provider

Green Flag ✅

Free first consultation

Certified, trained counsellors

Transparent about all fees

Clear, written plan before you commit

Regular check-ins and progress tracking

Does not guarantee impossible outcomes

Builds a plan based on your actual income

Red Flag ❌

Charges fees before assessment

No visible credentials or qualifications

Hidden charges revealed only after signing up

Vague verbal promises only

No ongoing support after enrolment

"We'll clear your debt in 3 months guaranteed"

Generic plans that don't account for your situation

How FREED Helps With Debt Management

FREED offers two structured programs - both focused on giving you a clear, personalised path out of debt.

FREED Debt Resolution Program For people who have already defaulted or genuinely cannot repay the full amount. We save towards settlement in a Special Purpose Account. We negotiate with lenders for maximum reduction (on average 56% less). You pay less. Debt is closed. Fresh start.

FREED Debt Consolidation Program For people with multiple loans who can still repay but need one lower EMI. We combine all your loans into one through our lending partners. One payment. Lower interest. Simpler to manage.

For people who want to build a debt management plan themselves - our certified counsellors help you understand your full debt picture, build a realistic budget, and identify which debts to address first. We also help you understand how your current debts are affecting your financial health - so you know what to focus on.

Throughout any program - FREED Shield protects you from recovery harassment.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

About FREED

FREED is India's first and leading Debt Relief Platform. We help people who are overwhelmed by credit card bills, personal loans, and EMIs find a legal, stress-free path to becoming debt-free.

We offer Debt Resolution (settle for less when you genuinely can't repay in full) and Debt Consolidation (combine all loans into one lower EMI). We also guide people on building realistic debt management plans - based on their actual income and debt situation.

We protect you from recovery harassment through FREED Shield - trusted by over 15,00,000 Indians.

Over 60,000 Indians have used FREED to take back control of their finances.

No hidden charges. No judgement. Just honest, practical help.

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions