How to Remove NPA from CIBIL Report: A Step-by-Step Guide for Indians

Your loan got tagged as NPA (Non-Performing Asset). Banks are rejecting every new application you submit. Your CIBIL score crashed by a few hundred points. And every helpline person you've spoken to gives you a different answer. Here's what NPA actually means, whether it can be removed, and the realistic path to a clean credit report.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

NPA stands for Non-Performing Asset. Banks tag your loan NPA after 90+ days of missed EMIs.

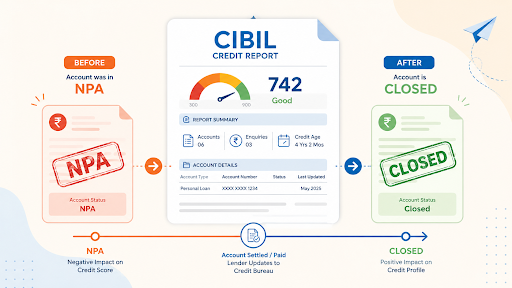

NPA cannot be deleted from CIBIL. It stays for upto 7 years from the closure date. But the status can be updated.

Only 2 legal ways to change NPA status: full repayment OR settlement with the bank.

A "Settled" tag still hurts your CIBIL but is far better than active NPA. A settled tag gets removed after 7 years.

Getting your loans settled with banks becomes really hard if your loan has been written off. FREED helps negotiate with banks and get you a settlement offer.

What Does "NPA" Mean in a CIBIL Report?

NPA stands for Non-Performing Asset. In simple words, it's a loan that the bank has stopped earning money on because you haven't paid your EMIs for 90 days or more.

This is the standard rule set by the RBI. The moment your missed payments cross 90 days, the bank is required to classify your loan as NPA. It's not the bank punishing you. It's a rule they have to follow.

After classification, the RBI also tracks how old the NPA is. There are three stages:

- Substandard: NPA for less than 12 months

- Doubtful: NPA between 1 and 3 years

- Loss: NPA for more than 3 years

On your CIBIL report, the account status will show one of four words: "NPA", "Written-off", "Suit Filed", or "Settled". Each word means something different to the next bank or NBFC checking your file. The RBI's own reports show that more and more Indians are getting NPA tags on personal loans and credit cards every year. You are not alone in this.

Can NPA Be Removed From CIBIL?

No. An NPA entry cannot be deleted from your CIBIL report. What can be done is update the status to "Closed" once you clear the dues. The entire record then drops off automatically after 7 years from the closure date.

You may have seen ads or got calls from agents promising to "remove NPA from CIBIL in 7 days" or "clean your credit report overnight". These are illegal. CIBIL records are maintained only by RBI-approved credit bureaus. No agent has the power to delete a real NPA entry.

The four bureaus approved by RBI are TransUnion CIBIL, Experian, Equifax, and CRIF High Mark. At FREED, we have direct tie-ups with Equifax and Experian. This helps us track your CIBIL status changes faster after a settlement.

What you actually can do:

- Update the account status from NPA to Closed or Settled (after clearing dues)

- Dispute any genuine error in the report

- Negotiate a One Time Settlement with the bank

Why NPA on CIBIL is a Serious Problem

An NPA tag is not just a label. It changes how every bank and NBFC sees you.

Your loan applications start getting rejected automatically. Most banks have a filter in their system that flags any CIBIL report with an active NPA. The application is rejected before a human even looks at it. Even credit cards become impossible to get.

Your CIBIL score drops sharply. A fall of 150 to 300 points is common once an account is tagged NPA.

The entry stays on your CIBIL report for 7 years from the date of closure. Not from the date the NPA was tagged. So the sooner you close it, the sooner the clock starts.

Recovery calls begin. The calls usually start from the bank or NBFC, and later from recovery agents. If the loan is a secured loan like a home loan or car loan, the bank may also send a SARFAESI notice (a legal notice that lets them act against the property). Some company HR teams and embassies also check your credit before a job offer or visa. An active NPA can show up there too.

Stuck with an NPA tag and don't know where to start?

Our team has helped 15,000+ Indians settle and clean up their credit. Free first consultation. No judgment.

Connect with a FREED ExpertHow to Remove NPA from CIBIL: The 2 Real Options

There are exactly two legal ways to change the NPA status on your CIBIL report. Both involve closing the loan account, just in different ways.

Option 1: Pay the Full Outstanding Amount

You pay the bank everything you owe, including principal, interest, and penalties. The bank then reverses the NPA tag to "Standard" and finally to "Closed". This is the cleanest option for your CIBIL. But it's also the hardest, because most borrowers stuck with an NPA are stuck precisely because they don't have a lump sum.

Option 2: One Time Settlement (OTS)

You and the bank agree on a reduced lump sum amount that closes the loan. The bank issues a No Objection Certificate (NOC) and updates CIBIL to "Settled". The "Settled" tag still stays on your report for 7 years, but your recovery journey starts the day the account is closed.

This is where most borrowers with multiple loans actually land. And this is where it gets complicated.

Settling with a bank after NPA classification is not the same as paying a late EMI. The bank's recovery team has already written your loan off as a loss in their books. Getting a reasonable settlement percentage requires knowing the bank's internal write-off thresholds, RBI rules around provisioning, and the right escalation contact inside the bank. At FREED, we negotiate directly with banks and NBFCs on your behalf. Our team has handled 2015,000+ settlements and knows what each bank typically accepts. Settlement terms depend on the loan provider; FREED is not a lender, final approval rests with the bank, and we never guarantee any specific outcome.

FREED Expert Tip

The first settlement quote from a bank is usually 70-80% of the outstanding amount. With proper negotiation, this figure can come down. Talk to a FREED counsellor before saying yes to any first offer.

Talk to a FREED Expert →Step-by-Step Process to Clean Up NPA from CIBIL

Here is how we walk our clients through the full clean-up process at FREED. Six simple steps.

1. We pull your full CIBIL report together We check the exact NPA status, the bank name, the outstanding amount, and any errors.

2. We tell you what to say (and not say) to bank callers You stop ignoring calls, but you also stop agreeing to anything verbally.

3. We give you a likely settlement estimate for each loan Based on the bank and your loan stage, we share what's realistic before you commit to anything.

4. We negotiate with the banks directly You don't need to handle the back-and-forth. Our team takes over the communication.

5. We make sure you get the NOC in writing A settlement is not real until you have the closure letter in hand. We chase the bank till it's done.

6. We track the CIBIL status update The bank must report the closure to the bureau within 30 days. If they don't, we help you raise a formal dispute.

What the Law Says

Under RBI's Fair Practices Code, banks must update credit bureaus within 30 days of any loan settlement or closure. If your CIBIL still shows the old NPA tag after 45 days, you have the legal right to raise a dispute with the bureau. FREED handles this dispute for you.

Talk to UsHow Long Does NPA Take to Clear from CIBIL?

The full NPA record drops off your CIBIL report 7 years from the date of closure. Not from the date the NPA tag first appeared. So the clock only starts ticking once you close or settle the loan. Every month you delay, you delay the day your report becomes fully clean.

Your CIBIL score, though, starts recovering much faster than 7 years.

Here's the realistic timeline most of our FREED clients see. The first small score improvement usually shows 6 to 12 months after closure. Crossing the 700 mark takes 18 to 24 months of careful credit behaviour after that. By that point, the NPA is still on your report, but a lot of banks will start considering your applications again because they can see the closure and your fresh good history.

The two things that decide how fast you recover are: how quickly you close the account, and how disciplined you are with any new credit you take after.

Common Mistakes That Keep NPA Stuck on Your Report

These are the most common mistakes we see when borrowers try to handle this alone:

- Paying a partial amount without a written agreement, hoping the bank will close the account anyway

- Agreeing to a settlement on a phone call, with no email or letter to back it up

- Forgetting to collect the No Objection Certificate after paying

- Not checking the CIBIL update after 30 days of closure

- Falling for agents who promise to "fix CIBIL in 24 hours" (this is not legal)

- Taking a new loan to pay off the NPA, which is the textbook start of a loan trap

How FREED Helps Remove NPA Status from CIBIL

We work with you on three main fronts.

Direct bank negotiation: At FREED, we talk to your banks and NBFCs directly. Provide Support against Recovery Harrasment Calls. We open a structured conversation with the recovery team and negotiate a settlement that fits your real financial position.

A structured payment plan: Depending on what you can afford, the settlement amount can be paid as a single lump sum or broken into 2 or 3 instalments. The plan is built around your monthly income, not the bank's first offer.

CIBIL follow-through: After settlement, we ensure the bank reports the closure to the bureaus within the 30-day rule. Our tie-ups with Equifax and Experian help us track changes on your file faster than most.

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions