ICICI Bank Debt Consolidation Loan: How It Works, Who Qualifies, and What to Know First

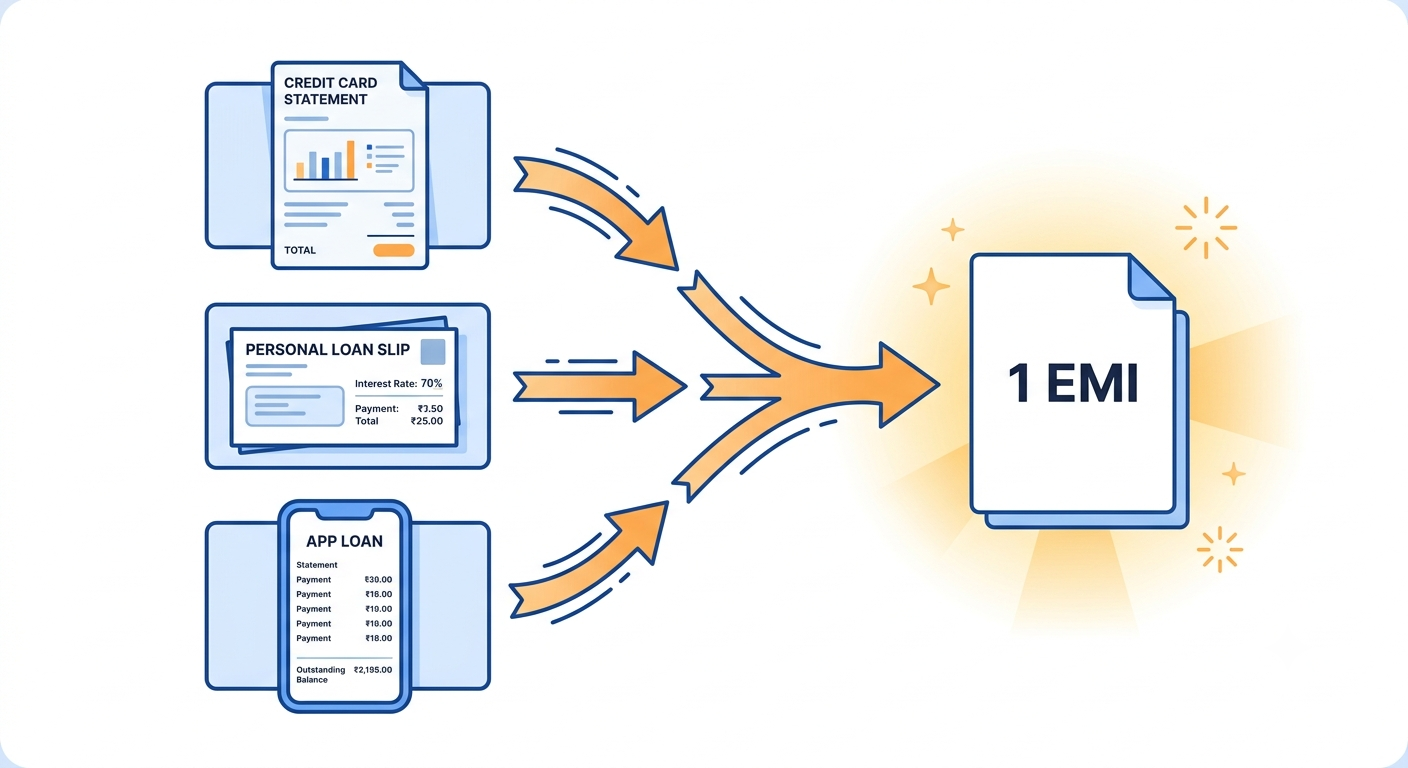

Doing this yourself usually means applying bank by bank, each application leaving a hard inquiry on your credit report whether you're approved or not. FREED's Debt Consolidation Program checks multiple lending partners through a single soft inquiry first, so you only take one hard inquiry, at the bank you actually move forward with. An ICICI Bank debt consolidation loan is a personal loan you use to pay off multiple existing debts, credit card dues, personal loans, app loans, and replace them with a single EMI. ICICI Bank doesn't offer a product literally called a "consolidation loan." What they offer is a personal loan that can be used for this purpose. Whether it helps you depends on your income, credit score, and total debt load.

FREED India

Reviewed by FREED India, SEO Intern

Key summury

An ICICI debt consolidation loan is actually a personal loan used to merge multiple debts into one EMI.

ICICI personal loan amounts for this purpose may go up to ₹25 lakh, with repayment tenures up to 6 years.

You typically need a CIBIL score of 700+ and a stable income to be eligible. Not everyone carrying debt will qualify.

Consolidation lowers stress and simplifies payments, but it doesn't reduce the total amount you owe.

If you're already missing EMIs or have a low CIBIL score, consolidation may not be available to you. FREED's Loan Consolidation Program can check your eligibility across multiple lending partners with a single soft inquiry, before you apply anywhere directly.

What Is an ICICI Bank Debt Consolidation Loan?

ICICI Bank doesn't have a standalone product called a "debt consolidation loan." What people mean by this term is ICICI's regular personal loan, used specifically to pay off several existing debts at once.

Here's what that looks like in practice: you take a new personal loan large enough to cover what you currently owe across credit cards, other personal loans, and app loans. You use that amount to pay everything off, and you're left repaying just one loan, with one EMI, to one bank.

It's worth being clear about what this is and isn't. Consolidation can simplify your monthly payments and may bring your overall interest cost down if your existing debts were at higher rates. It's a loan, not a discount. You still owe the full principal amount.

For consolidation purposes, ICICI personal loan amounts can go up to ₹25 lakh, with repayment tenures of up to 6 years. Interest rates vary based on your credit profile and income, so it's best to check the current numbers directly with ICICI Bank rather than relying on a fixed figure here.

Who Can Apply for an ICICI Personal Loan for Debt Consolidation?

Eligibility comes down to a few practical things: your age, your income, your employment type, and your credit score.

Salaried applicants are generally considered within a working-age range, and self-employed applicants are evaluated a little differently, usually with more documentation. A minimum monthly income applies for salaried applicants, and it's higher in practice for higher loan amounts.

Here's the part worth being upfront about: a CIBIL score of 700 or above tends to improve your approval chances, though it doesn't guarantee anything. Banks look at the full picture, not the score alone. If you're already in financial difficulty, it's worth knowing this in advance rather than after a hard inquiry.

You'll generally need: ID proof, address proof, your PAN card, the last 3 months of salary slips, and 6 months of bank statements. Self-employed applicants typically need additional income documentation, such as ITR filings.

Gathering all of this is exactly the kind of legwork FREED's team can take off your hands if you'd rather not chase down paperwork for an application that might not go through.

Why Use FREED Instead of Applying to ICICI Directly?

Applying yourself means picking a bank, applying, and finding out only afterward whether you'd have qualified somewhere else, with a hard inquiry already on your record either way. If ICICI says no, the next application starts the same risk all over again.

FREED's Debt Consolidation Program works differently. It checks your eligibility across multiple lending partners using a soft inquiry, which doesn't affect your CIBIL score, and only takes you to a hard inquiry once, at the one bank that's actually likely to approve you.

FREED handles the matching and the paperwork. This isn't a replacement for knowing how ICICI's own process works. It's a way to find out where you stand before you spend a hard inquiry finding out the hard way.

FREED has worked with over 20,00,000 customers and helped settle more than 20,000 accounts. [STATS FLAG: the ₹3,200 Cr+ debt managed and 4.7-star/3,000+ reviews figures should be verified against FREED's current published numbers before publish, as these change over time.]

Applying to ICICI Directly vs. Using FREED's Debt Consolidation Program

Factor | Applying to ICICI Directly | Using FREED |

|---|---|---|

Number of applications | One bank at a time | Multiple lending partners checked at once |

Hard inquiry risk | One hard inquiry per bank you apply to | One soft inquiry upfront, one hard inquiry only at the bank you proceed with |

Who handles the paperwork | You do | FREED prepares and manages it for you |

If rejected | You start over with a new bank and a new hard inquiry | FREED can check other lending partners without repeating the hard-inquiry risk |

Fee structure | No fee to apply, but rejection costs you a CIBIL hit | Success-based; you pay only if a loan is disbursed |

This table is for general comparison only. FREED is not a Bank or NBFC, and loan approval is always decided by the lending partner. Verify current terms directly before applying anywhere.

How Does ICICI Debt Consolidation Work, Step by Step?

List every debt you currently have. Write down the outstanding amount, EMI, and interest rate for each loan or card you're paying off.

Check your CIBIL score. You need to know where you stand before applying anywhere.

Work out if consolidation actually saves you money. Compare your new estimated EMI against the total of what you're currently paying across all your debts.

Apply for the ICICI personal loan. This can be done online through ICICI's website or at a branch, along with your documents.

Use the disbursed amount to close your existing loans right away. Pay off each outstanding balance and collect a No Objection Certificate (NOC, a clearance letter) from each bank.

Repay the new single EMI on time. This protects your CIBIL score and keeps you from drifting back into multiple debts.

This is exactly the legwork FREED's Debt Consolidation Program takes off your plate, checking eligibility, comparing lending partners, and handling the paperwork, so you're not doing steps 1 through 4 manually and hoping for the best.

What Does an ICICI Debt Consolidation Loan Actually Cost?

The interest rate is only part of the cost. Processing fees and prepayment charges also factor in, and it's worth checking ICICI's current fee schedule directly with the bank before applying, since these change over time.

Tenure matters more than people expect. A longer repayment period brings your monthly EMI down, but it also means paying more total interest over the life of the loan. A shorter tenure does the opposite: higher EMI, less total interest.

Here's a simple way to picture it. Say you're juggling ₹3 lakh spread across three different debts, each at a relatively high rate. If you consolidate that into a single ₹3 lakh personal loan at a lower combined rate, your monthly outgo can drop, though the actual numbers depend entirely on your approved rate and tenure. It's worth running your own numbers rather than assuming a fixed outcome.

It's a detail people commonly miss when comparing their current debts to a new consolidation loan: focusing only on the interest rate and overlooking prepayment charges. It's worth asking your bank about this directly before you sign anything, and a FREED counsellor can walk you through what to ask for if you're unsure.

These are indicative figures only. Actual rates and charges are decided by ICICI Bank based on your profile. FREED is not a Bank or NBFC. Verify all figures directly with ICICI Bank before applying.

When Does an ICICI Consolidation Loan Actually Help?

It tends to work well when your CIBIL score is healthy, your income is stable, your existing loans carry meaningfully higher interest than what a new personal loan would offer, and you haven't missed any payments yet. In that situation, consolidation can genuinely simplify your finances and reduce what you're paying in interest overall.

It tends not to help when you've already defaulted, your CIBIL score has dropped significantly, your income is irregular, or your total debt is more than a personal loan is likely to cover. In those cases, applying for a new loan often adds risk rather than removing it.

This is the honest part worth sitting with: consolidation is a tool for people who are still managing, just want things simpler. It isn't built for someone who's already struggling to make payments at all.

What If You Don't Qualify for an ICICI Consolidation Loan?

Not qualifying doesn't mean you're out of options. It usually means a different option fits better right now.

Ask your bank about EMI restructuring (changing how you repay). Some banks will revise your terms directly if you ask.

Look into a moratorium (a temporary pause). This can buy you breathing room during a genuinely difficult stretch.

Ask about a tenure extension on your current loans, which can bring your EMI down without taking on anything new.

If you haven't defaulted yet, ask FREED about its own Debt Consolidation Program. One rejection from ICICI doesn't necessarily close the door on consolidation altogether. FREED assesses your full profile and can match you with a suitable lending partner from its network, so the loan doesn't have to come from the same bank that turned you down. This is still for borrowers who are managing their payments, just stretched across too many EMIs, and it doesn't carry the CIBIL impact that settlement does.

If none of that is realistic, settlement becomes the option that's left. This is only for someone who genuinely cannot repay, not someone who's stressed but able to manage with adjustment.

It's worth being honest about what settlement actually costs. Your account gets marked "Settled" on your CIBIL report, and that status can stay there for up to 7 years, affecting your ability to get new credit during that time. [LEGAL FLAG: any reference to cheque-related legal risk under the Negotiable Instruments Act should be reviewed and verified by the legal team before publish, since this depends heavily on individual circumstances.]

FREED's role here is to help people see all of their options clearly, starting with whichever one protects their credit score the most. Settlement is never framed as a good outcome. It's the option that exists for when the others genuinely don't work.

What the Law Says

Banks and NBFCs must follow RBI's Fair Practices Code when recovering dues. No threats, no calls before 8 AM or after 7 PM, and no contacting your employer without consent.

[Know your credit rights →]ICICI vs. Other Banks for Debt Consolidation: What to Know

There's no single best bank for this. Each one has a different profile of strengths, and what fits depends on your own situation.

ICICI is reported to offer flexibility around prepayment for personal loans used this way. SBI may suit government employees particularly well, given its scale in that segment. HDFC may move faster for customers who already bank with them. None of this makes any one of them the right or wrong choice in general. It depends on where you already bank, your income type, and your credit profile.

Bank | Loan Amount | Tenure | Key Feature | CIBIL Indicative Threshold |

ICICI Bank | Up to ₹25 lakh | Up to 6 years | Reported prepayment flexibility | 750+ |

HDFC Bank | Varies by profile | Varies by profile | May be faster for existing customers | 720+ |

SBI | Varies by profile | Varies by profile | May suit government employees | 650-670+ |

Axis Bank | Varies by profile | Varies by profile | Varies by individual offer | 720+ |

Kotak Mahindra Bank | Varies by profile | Varies by profile | Varies by individual offer | 685+ |

This table is for general comparison only. Rates, eligibility, and terms are set by each bank independently. FREED is not affiliated with any bank listed here.

See If Consolidation Could Reduce Your EMI Burden

Debt Calculator

[Inputs: total current debt, expected new interest rate, repayment tenure. Outputs: estimated new monthly EMI, total interest saved versus your current scenario, time to becoming debt-free.]

These are estimated figures only. Actual interest rates and loan eligibility are decided by ICICI Bank based on your individual credit profile. FREED is not a Bank or NBFC and does not guarantee loan approval or specific savings. Always verify directly with ICICI Bank before applying.

Not Sure if Consolidation Is Right for You?

Free assessment. No commitment. Real options for your situation.

[Get My Free Assessment]Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

Tips That Help When Using a Consolidation Loan

A few habits make a real difference once your loan comes through.

- Close old credit card accounts once they're paid off. It removes temptation and improves your credit utilisation ratio (the percentage of your card limit you're using).

- Set up auto-pay for the new EMI right away. A NACH mandate (an auto-payment authorisation) takes the risk of a missed payment off your plate.

- Avoid applying for new credit while you're repaying. It's not the moment to add anything else.

- Build a small buffer each month, even ₹500 to ₹1,000, so a small emergency doesn't push you toward another loan.

Ready to Decide? Here's the Quickest Way to Find Out

If you've read this far, you already know more about how ICICI's consolidation route works than most applicants do going in. The next step is finding out where you actually stand, without spending a hard inquiry to do it.

FREED's Debt Consolidation Program checks your eligibility across multiple lending partners with one soft inquiry, handles the paperwork, and only charges a fee once a loan is actually disbursed. If consolidation is the right move for you, this is the fastest way to know for sure.

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions