What is Loan Consolidation? Meaning, How It Works & When It's Not Enough

Five EMIs. Five due dates. Five reminder calls before the 10th. By the time salary hits your account, half of it is already spoken for. Loan consolidation is one fix people hear about and it works for some people in some situations. But it is not the only option, and it is not always the right one. Let's break it down properly.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

Loan consolidation means combining multiple loans into one bigger loan with one EMI.

It works only if your CIBIL score is decent usually 700 or above and your income comfortably supports the new EMI.

The real benefit is simpler tracking and sometimes a lower interest rate. The real risk is that a longer tenure means more total interest paid over time.

Consolidation does not reduce what you owe. It only rearranges it.

If your EMIs already cross 50% of your salary or your CIBIL has dropped due to missed payments, a consolidation loan will likely get rejected. Debt settlement may be the better route. FREED can assess which path fits you in one free call.

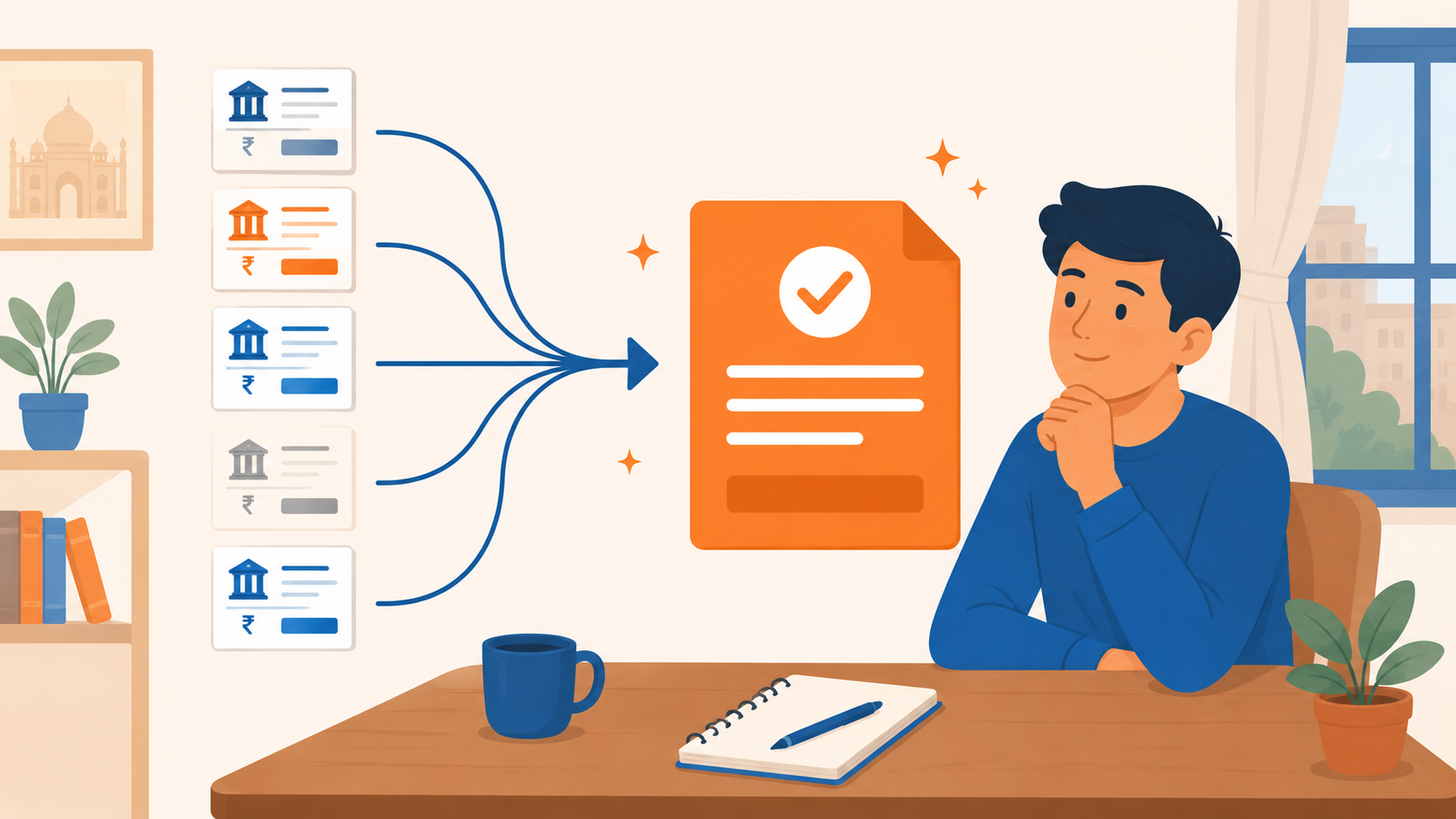

How Does Loan Consolidation Work in India?

Step 01 List every loan you owe Write down each one name of bank or NBFC, amount still outstanding, interest rate, and monthly EMI.

Step 02 Check your CIBIL score Most banks and NBFCs offering consolidation loans want a score of 700 or above. Below that, your application may be rejected or approved at a high interest rate.

Step 03 Apply for a consolidation loan or balance transfer You can apply directly with a bank or NBFC. A balance transfer moves your outstanding dues to a new bank at a different rate.

Step 04 Wait for approval and disbursement If approved, the new bank disburses a loan amount equal to your total outstanding balance across all old loans.

Step 05 Use the new loan amount to pay off all old loans Every old account gets paid off. Each gets marked as paid in full.

Step 06 Pay one EMI to one bank going forward From here, you pay a single monthly EMI to one bank for one fixed tenure.

Benefits of Loan Consolidation

One EMI, one due date no more missed payments because you forgot which app was due when.

Possibly lower interest if your CIBIL is 700 or above, you may qualify for a rate lower than your current average, especially on credit card debt.

Easier to budget you know exactly how much leaves your account every month. No surprises.

Pays off high-interest debt, credit card balances and app loans carrying very high rates get paid off in one go. That stops the compounding.

One point of contact for one bank or NBFC to deal with instead of 5 or 6. Less stress, fewer calls.

CIBIL can improve over time if you pay the new consolidated EMI on time every month, your credit score gradually rebuilds.

Risks and Hidden Costs of Loan Consolidation

This is the section most blogs skip. We don't.

What Looks Like What Reality Is

Lower EMI → Tenure is longer, so total interest paid over the full period is higher.

One simple payment → Processing fee of 1% to 3% on the new loan eats into any savings.

Lower interest rate → This only happens if your CIBIL is 720 or above. Below that, the rate may stay high or the application gets rejected.

Pays off old loans → It does not reduce the amount you owe. It shifts it to a new place.

Improves credit score → Only if you stop taking new loans after consolidating.

There is also a bigger risk that most people do not talk about.

Many borrowers consolidate, feel relieved, and then swipe a credit card or take a small app loan within 3 to 6 months. Now they have the consolidation EMI running plus fresh new debt on top. The trap does not just return. It doubles.

Consolidation fixes the structure. It does not fix the habit. Both need attention.

FREED Expert Tip

If your total EMIs already eat up more than 50% of your take-home salary, consolidation may not be available to you and may not help even if it is.

FREED counsellor first freeLoan Consolidation vs Debt Settlement Which One Is Right for You?

Both are legitimate paths. They fit different situations.

Loan Consolidation Works When:

- Your CIBIL is 700 or above.

- Your income comfortably covers a new single EMI.

- Your total debt is under 40 to 50% of your annual income.

- You have had no missed payments in the last 6 months.

- You can commit to zero new borrowing from today.

Loan Settlement Fits Better When:

- Your CIBIL has already dropped because of missed EMIs.

- Recovery calls have started.

- You have multiple unsecured loans: credit cards, personal loans, app loans.

- The total amount feels impossible to repay in full.

- You need actual debt reduction, not just rearrangement.

Settlement is not something a borrower chooses out of preference. Banks and financial companies only consider it when you are in genuine financial difficulty and are truly unable to repay the full amount. It is a last resort, not a shortcut.

When settlement is the path, having someone handle the back-and-forth with the bank makes a real difference. FREED counsellors handle the communication with your banks, help put your documents together, and get the settlement letter worded correctly so your CIBIL can begin to recover afterwards. FREED has helped banks and borrowers arrive at settlements that reduce total debt by up to 50%* in eligible cases.

*Rates and ranges shown are indicative. Final terms decided by the bank or NBFC. FREED is not a loan provider. No outcome is guaranteed. Please verify all terms directly with your bank.

Not sure if consolidation or settlement fits your situation?

60,000+ Indians have used FREED to find the right exit from debt. One free call. No pressure.

Get My Free Debt AssessmentWho Should Avoid Loan Consolidation?

You have already missed 2 or more EMIs. Your CIBIL is likely too low for a fresh consolidation loan to be approved.

Your income has dropped or your job is not stable taking on a new structured loan when income is uncertain adds risk.

You are consolidating just to buy time, not to change the actual income vs. spending gap.

The consolidation loan rate you are being offered is higher than your current average rate in that case, you are paying more, not less.

You cannot commit to zero new borrowing for at least the next 12 months.

If any of these apply, consolidation will likely not solve the problem. Other paths exist debt settlement, loan restructuring (changing the repayment plan with your bank), or a Debt Management Program (a structured plan where all your debts are handled together under one payment). A free FREED call can map the right one for your situation.

What the Law Says

Under the RBI's Fair Practices Code for Banks and NBFCs, you have the right to a full loan agreement that clearly shows the total cost, processing fees, prepayment terms, and effective interest rate before you sign any consolidation loan. Fees cannot be bundled or hidden. You can also prepay or pay off the new loan early, with limited or no charges on floating-rate personal loans, as per RBI guidelines.

Know your full borrower rights →How to Choose the Right Consolidation Loan

Compare the effective interest rate, not just the headline rate shown in the ad.

Ask for processing fees, prepayment charges, and late payment fees in writing before you sign.

Match the new tenure to how stable your income is not just to the lowest possible EMI.

Do not accept a top-up loan bundled with the consolidation. It adds more debt, not less.

Keep all loan closure letters from your old banks and NBFCs safely. You will need them if there is a dispute later.

Still stuck choosing?

Let an expert do the math for you. Free 15-minute call. Honest plan. Zero sales pressure.

Talk to a FREED CounsellorFREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions