How to Get a Loan Without a CIBIL Score in India

A loan without a CIBIL score is a loan approved without relying on a credit history report. It applies to two very different groups: people who have never borrowed before and have no score yet, and people whose score has dropped due to past defaults. Both can still access credit in India, but through different routes and at different costs.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

A loan without a CIBIL score is possible in India. Gold loans, FD-backed loans, and NBFC loans don't require a score to apply

As of August 2025, the Ministry of Finance confirmed in Parliament that banks cannot reject first-time borrowers simply for having no credit history, per RBI's Master Direction dated January 6, 2025.

No CIBIL score and a low CIBIL score are different problems with different solutions.

Gold loan rates start from roughly 8.05% to 8.55% per year regardless of CIBIL status. NBFC personal loans for no-score borrowers typically run 18% to 36% per year

Every new loan application creates a hard enquiry that may be considered by lenders when assessing future applications. Apply to 1 to 2 places only

What Does "No CIBIL Score" Actually Mean?

Most articles skip this part. They assume you already know which situation you're in. You might not. These are two completely different things.

The first situation: you have never taken a loan or a credit card. There is no record of your repayment behaviour anywhere. CIBIL shows your score as "NH" (No History) or "-1" because there is simply nothing to score. You are not a risk. You are a blank page. Lenders call this new-to-credit.

The second situation: you have borrowed before, missed payments, defaulted, or settled a loan. Your score exists but reflects previous repayment issues. Lenders can see the full history. That history is the problem, not the absence of one.

Both situations make borrowing harder. But for different reasons and with different solutions. A bank offering a product designed for new-to-credit borrowers is not the right product for someone with a 520 score and a default on record. And vice versa.

Two more things worth knowing. First, 68% of borrowers in India did not know their CIBIL score even though they had already taken a loan, according to a Home Credit India survey cited in Business Standard. Many people searching for this topic don't actually know which group they're in. Second, the RBI has not prescribed any minimum CIBIL score for loan approvals. Banks use their own board-approved criteria. As of August 2025, the Ministry of Finance confirmed in Lok Sabha that banks cannot reject first-time loan applications solely because the applicant has no credit history, per RBI Master Direction dated January 6, 2025. (Source: Business Standard - https://www.business-standard.com/finance/personal-finance/cibil-score-not-mandatory-govt-tells-banks-not-to-reject-first-time-loans-125082500426_1.html )

Why Does Having No CIBIL Score Make Loan Approval Harder?

A bank approving a loan is making a bet. It is betting that you will repay on time. CIBIL is the evidence it uses to make that bet with confidence. When there is no CIBIL score, there is no evidence. Not bad evidence, no evidence.

So the bank falls back on other signals. Your income. How stable your employment is. What your bank account looks like over the last 6 months. Whether you have an existing relationship with them, a salary account or a recurring deposit that shows a track record of some kind.

The most common profiles who land in this situation are straightforward. Fresh graduates who have never had a credit card. Salaried employees in their first job with a salary account that is less than 12 months old. Self-employed professionals or gig workers who have always dealt in cash or UPI and never applied for formal credit. People who have moved back from abroad and whose Indian credit file is completely empty.

None of these situations reflect irresponsibility. They just reflect a gap in the formal credit record.

NBFC personal loans for no-score borrowers are typically available for amounts between Rs. 10,000 and Rs. 3 lakh. These are smaller amounts than what a scored borrower with a clean history can access, but they are real and accessible.

Having no score is in some ways a cleaner position than having a low score. There is no negative history to overcome. The first repayment you make starts building something positive from scratch.

Signs You May Be Trying to Get a Loan Without a CIBIL Score

Check which of these fits your situation. The action you take depends on which one applies.

- You have never taken a loan or credit card and are applying for the first time

- You are a fresh graduate or early-career professional whose first salary account is less than 12 months old

- You are self-employed or a gig worker who has always paid in cash or UPI and never had a formal credit product

- You moved back from abroad recently and your Indian credit file is empty

- You were told by a bank that "no credit history was found" on your CIBIL report

- Your loan application was rejected and you don't know why. Your score isn't low, it simply doesn't exist yet

- You have a score below 600 due to past defaults and banks are treating you as if you have no usable credit history

If you fall into the first six bullets, you are a new-to-credit borrower. The options and process in this guide are built for you. If you fall into the last bullet, the loan options listed below still apply, but the path to rebuilding is different and covered further down.

FREED Expert Tip

Check your CIBIL report for free at cibil.com before applying anywhere. If the report shows "NH" (No History) or "-1", that means no score exists yet, not that your score is bad. Some NBFCs and banks have specific products for new-to-credit borrowers that are different from products for low-score borrowers. Knowing which you are saves time and protects your score from unnecessary hard enquiries.

Talk to a FREED ExpertWhat Loan Options Are Available Without a CIBIL Score?

Here are the real options, in order from lowest cost and risk to highest.

- 1

Gold loan

Pledge gold jewellery or coins of 18 to 24 carat purity. No minimum CIBIL score required. The bank holds the gold and lends against its value. The RBI sets tiered limits on how much you can borrow against gold: up to 85% of the gold's value for loans under Rs. 2.5 lakh, 80% for Rs. 2.5 lakh to Rs. 5

- 2

Loan against fixed deposit (FD)

Borrow up to 90% of your FD value at 1 to 2% above the FD interest rate. No CIBIL check. This is the cheapest credit option available in India for anyone at any credit stage. The FD stays intact but is locked until the loan is repaid. This option is only available if you already have an FD sitting unused.

- 3

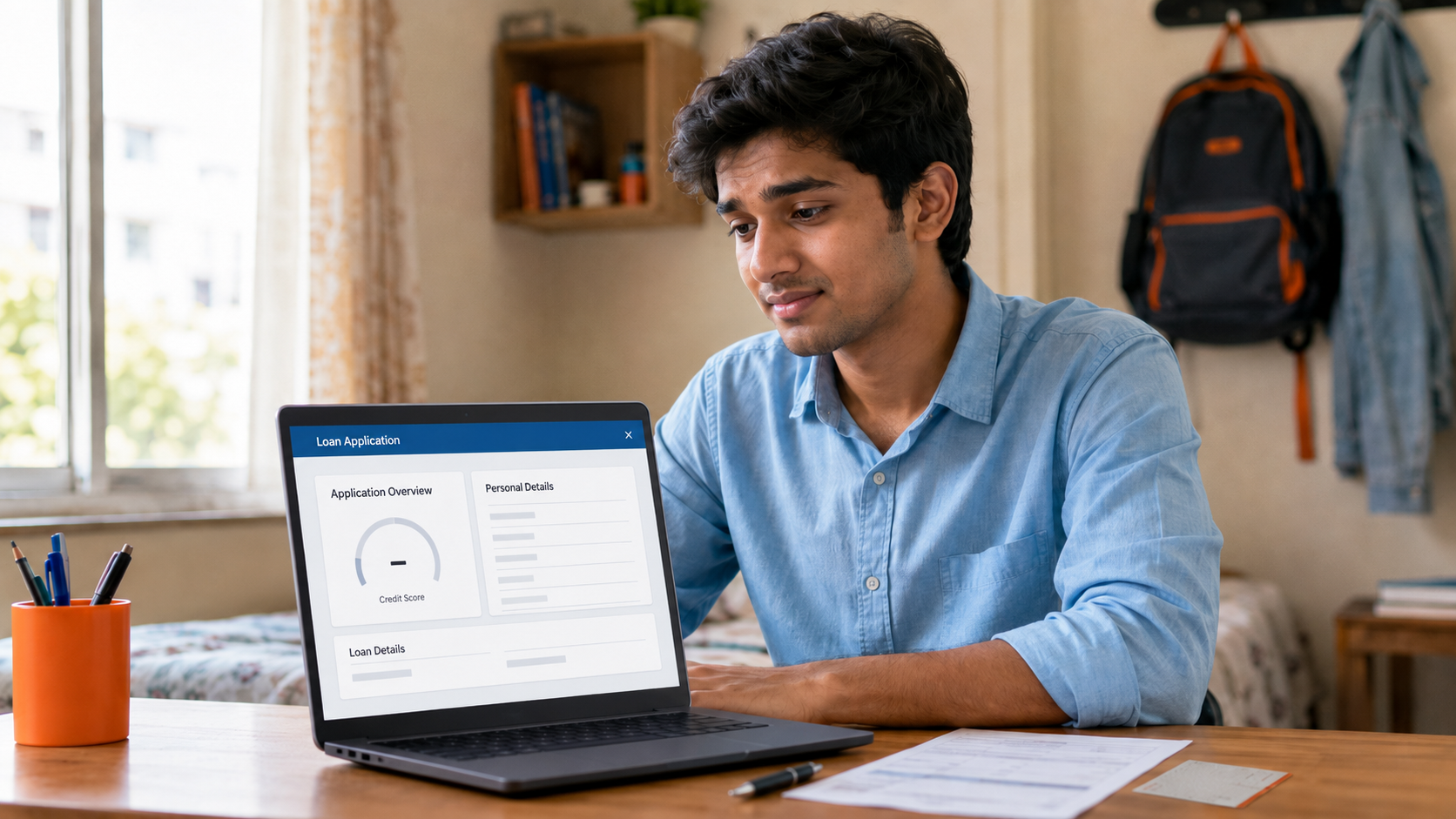

NBFC personal loan using alternative data

NBFCs (non-banking financial companies) and fintech companies assess income stability, bank transaction patterns, utility payment history, and employer type instead of CIBIL. Loan amounts for no-score borrowers are typically Rs. 10,000 to Rs. 3 lakh. Rates run 18% to 36% per year. Before signing anything, read the KFS (Key Fact Statement, a document listing all loan costs that every regulated

- 4

Co-applicant route

Add a family member with a CIBIL score of 700 or above as co-applicant. The loan terms are primarily based on the co-applicant's credit profile. Rates and approval chances improve meaningfully. The co-applicant must understand: Their credit profile may also be affected if repayments are missed. This must be discussed clearly before adding someone.

- 5

Existing bank relationship

If you have a salary account, recurring deposit, or a long-standing savings account with a bank, that bank may extend a small loan based on transaction history alone. It is not guaranteed, but it is worth trying before approaching an unfamiliar institution. The bank already knows your cash flow pattern

- 6

Microfinance institutions (MFIs)

Available for low-income individuals and small business owners who have never accessed formal credit. Loan amounts are modest. Rates typically run 15% to 26% per year. No CIBIL required. One thing to know: repayment schedules at MFIs are often weekly, not monthly.

Loan Without CIBIL Score: Options at a Glance

Option | CIBIL Score Needed | Typical Rate | Loan Amount | Key Caveat |

Gold loan | None (gold value matters) | 8.05% to 8.55% p.a. at banks | Rs. 20,000 to Rs. 50 lakh | Gold auctioned if you default |

Loan against FD | None | FD rate + 1 to 2% | Up to 90% of FD value | Only if FD exists |

NBFC personal loan | None, income assessed instead | 18% to 36% p.a. | Rs. 10,000 to Rs. 3 lakh | Read KFS carefully before signing |

Co-applicant route | Co-applicant needs 700+ | Tied to co-applicant profile | Varies by bank | Co-applicant's score affected by any default |

Existing bank relationship | Bank's discretion | Varies | Varies | Not guaranteed |

Microfinance (MFI) | None | 15% to 26% p.a. | Small amounts only | Weekly repayment often required |

Note: These are general indicators. Final terms are decided by the bank, NBFC, or financial company. FREED is not a Loan Provider. No outcome is guaranteed. Please verify directly with your bank or NBFC.

How to Apply for a Loan Without a CIBIL Score, Step by Step

Gold loans and FD-backed loans are simple. Walk into a branch with your gold or FD details, pledge the asset, and the loan is often disbursed the same day. No CIBIL check, no income documents in most cases.

For an NBFC personal loan without a CIBIL score, here is the process.

- 1

Check your CIBIL report first to confirm you have no score

Go to cibil.com and download the free annual report. Look for "NH" (No History) or "-1" in the score field. This tells you whether you are a new-to-credit borrower or a low-score borrower. The loan path differs between the two. Do not skip this step.

- 2

Choose the loan type that matches your actual situation

If you have gold at home, the gold loan is the fastest, cheapest, and safest option. If you have an FD, use it as collateral. Only if neither applies should you approach NBFCs for an unsecured personal loan.

- 3

Pick 1 or 2 NBFCs that specifically work with no-score borrowers

Research before applying. Not all NBFCs accept no-CIBIL applications. Applying to 5 places hoping one says yes creates multiple hard enquiries on your credit file. Even before a score has fully formed, multiple enquiries in a short period can make future approvals harder. Identify the right 1 or 2 institutions first.

- 4

Prepare your income and banking documents properly

For no-score borrowers, the bank statement is effectively the credit score. Provide the last 6 months of statements. Maintain a consistent balance rather than zeroing out the account after every salary credit. If self-employed, include ITR filings or GST returns to show income is real and regular.

- 5

Read the Key Fact Statement before signing anything

Every regulated bank and NBFC must give you a KFS (Key Fact Statement, a summary of all loan costs) before signing. Check the APR, processing fee, bounce charges, and prepayment penalty. If anything is unclear, ask.

What Happens to Your CIBIL Score When You Take a Loan Without One?

Most articles explain how to get the loan. Almost none explain what the loan does to your credit profile. This matters.

Taking a loan starts building your CIBIL score. Once a bank or NBFC reports even one loan to the credit bureau, a score begins to form. It does not appear overnight. But timely repayments from the very first EMI are the raw material the score is built from.

Within 6 to 12 months of consistent on-time repayments, a borrower can move from no score to a CIBIL score in the 650 to 700 range. That is a meaningful score. It opens up most NBFC products and puts prime bank products within reach.

But the reverse is also true, and more sharply so. Missing a payment on this first loan is particularly damaging. There is no positive history to offset the negative mark. A single default on a first loan sits alone in the record with nothing good beside it.

One thing that changed recently: since January 2025, banks report repayment data to Experian every 15 days instead of once a month. That means a payment you make mid-month can reflect in your credit profile faster than before. If you are actively building a score, this works in your favour.

Confirm before taking any loan that the bank or NBFC reports to a credit bureau. Not all MFIs and small NBFCs do. If the loan does not get reported, it cannot build your score, which defeats one of the key benefits of taking it.

What Are Your Options If a Loan Isn't the Right Move Right Now?

This section is for borrowers in a different situation: your score is very low because of debt you are struggling to manage, and taking a new loan is not the answer.

Work through these options in order.

Talk to your bank about changing the existing loan plan. Ask whether the EMI can be reduced by extending the repayment time. This keeps the account current without any default.

Merge all loans into one lower EMI. Debt consolidation (merging all your loans into a single loan with one lower monthly payment) can significantly reduce what you pay each month. FREED's Loan Consolidation Plan handles this for unsecured loans.

Explore a balance transfer if your CIBIL is 670 or above. Moving your loan to a bank with a lower interest rate reduces the EMI without requiring settlement, subject to lender approval.

If all the above have failed and repayment is genuinely impossible, loan settlement may apply. This applies to unsecured loans only: personal loans, credit cards, BNPL (buy now pay later) products, and loan apps. It does not apply to home loans or car loans.

How Loan Settlement Helps When Repayment Has Become Genuinely Impossible

Settlement is not something a borrower chooses out of preference. Banks and financial companies only consider it when you are in a genuine financial difficulty and are truly unable to repay the full amount. It is a last resort, not a shortcut.

When you settle an unsecured loan, the bank agrees to accept a reduced lump sum as the final payment. The outstanding balance is cleared. The account is then marked "Settled" on your CIBIL report.

That mark stays for up to 7 years. It is a negative mark. Any future bank or NBFC that checks your report will see it and treat it as a partial default. The account is reported as 'Settled,' which may be considered by future lenders.

But for someone who genuinely cannot repay and has exhausted every other option, settlement provides a defined end. No more accruing interest. No more recovery calls on a debt that will never be fully repaid. A fixed date from which CIBIL recovery can begin.

FREED helps borrowers settle their unpaid/overdue loans at up to 50% less*. The exact figure depends on the outstanding amount and the bank's own assessment.

FREED handles the back-and-forth with the bank or NBFC, prepares the required documents, and guides the full settlement process from start to finish. This is done for the borrower.

*Settlement waiver up to 50% is indicative, not a guarantee. Rates and ranges shown are indicative. Final terms decided by the bank. FREED is not a Loan Provider. No outcome is guaranteed. Please verify directly with your bank.

Things That Actually Help You Build a CIBIL Score from Scratch

Pay every EMI on time from the very first one. This is more important here than for any borrower with an established history. When there is no prior record to fall back on, a single missed payment is all there is. There is nothing positive beside it to soften the impact.

If you also get a secured credit card (a card issued against a fixed deposit you hold with the bank), maintain responsible credit utilisation. High utilisation on a forming score can suppress the number before it has a chance to grow.

Do not apply for multiple credit products at the same time. Once a score starts forming, multiple applications in a short window create hard enquiries and signal financial stress to future banks.

Check your CIBIL report 45 days after your first repayment. Confirm the bank has reported it correctly. Errors do happen. If the repayment is not showing, raise a dispute directly with CIBIL.

Since January 2025, RBI rules require lenders to report credit data to all four bureaus, including Experian, every 15 days instead of monthly. This means positive behaviour reflects faster than before.

Building from no score to above 700 takes sustained, disciplined repayment over time. There is no shortcut, and the exact timeline varies based on your individual credit activity. But the path is straightforward.

Source: RBI Master Direction (Credit Information Reporting) Directions, 2025, effective January 1, 2025 — https://www.business-standard.com/finance/news/rbi-mandates-fortnightly-credit-information-reporting-to-boost-transparency-124080801505_1.html

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions