How to Clear DPD in CIBIL Report: A Step-by-Step Guide

DPD (Days Past Due) in your CIBIL report shows how many days you were late paying an EMI or credit card bill. A genuine DPD entry cannot be removed, it stays for 36 months from the month of delay. But you can reduce its impact by paying on time going forward. And you can dispute any wrong DPD with CIBIL within 30 days.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

DPD (Days Past Due) shows how many days late you paid an EMI or credit card bill. CIBIL keeps your last 36 months of payment history, reported every month by your bank or NBFC.

A genuine DPD entry cannot be removed. It stays on your CIBIL report for 36 months from the month of delay. Only wrong or inaccurate entries can be disputed and corrected through CIBIL's official process.

Clear all overdue amounts right away and set up NACH mandate (auto-payment permission) on every loan and card. This stops new DPD entries from being added each month.

Consistent on-time payments over 6 to 12 months reduce the weight of old DPD entries on your score. A DPD from 30 months ago hurts your score far less than one from last month.

If DPD is piling up across multiple loans and your total EMIs have crossed 50% of your take-home salary, standard advice of "pay on time and wait" does not match your situation. Talk to a FREED counsellor before missing another EMI. The first call is free with no commitment needed.

You Are Not Stuck With a Bad CIBIL Forever

You just pulled up your CIBIL report. You see "DPD 60" next to a personal loan from two years ago. It can feel stressful and discouraging.

First breathe. This does not mean you are a bad borrower. Millions of Indians have DPD entries on their report. A medical emergency. A job loss. An EMI that slipped through during a rough patch. It happens.

A late EMI doesn't make you irresponsible. It makes you human.

The important thing is what you do next. This blog will show you exactly what DPD is, where to find it, and what you can actually do about it step by step. Let's first understand what DPD actually is, then exactly what you can do about it.

What Is DPD in a CIBIL Report?

DPD stands for Days Past Due. It is simply the number of days you paid your EMI or credit card bill after the due date.

The calculation is straightforward. Payment Date minus Due Date equals your DPD value. For example: your EMI was due on the 5th of the month. You paid it on the 20th. That is a DPD of 15.

Here is what the codes mean when you look at your report:

- 000 Paid on time. No negative impact.

- 030 / 060 / 090 / 120+ Number of days late that month. Higher is worse.

- XXX The Bank or NBFC (non-bank loan company) did not report that month. No negative impact.

- STD Standard account. Paid on time, in good shape.

- SUB Sub-standard. Account has started slipping.

- DBT Doubtful. Serious default stage.

- LSS Loss. The bank has classified the loan as unrecoverable.

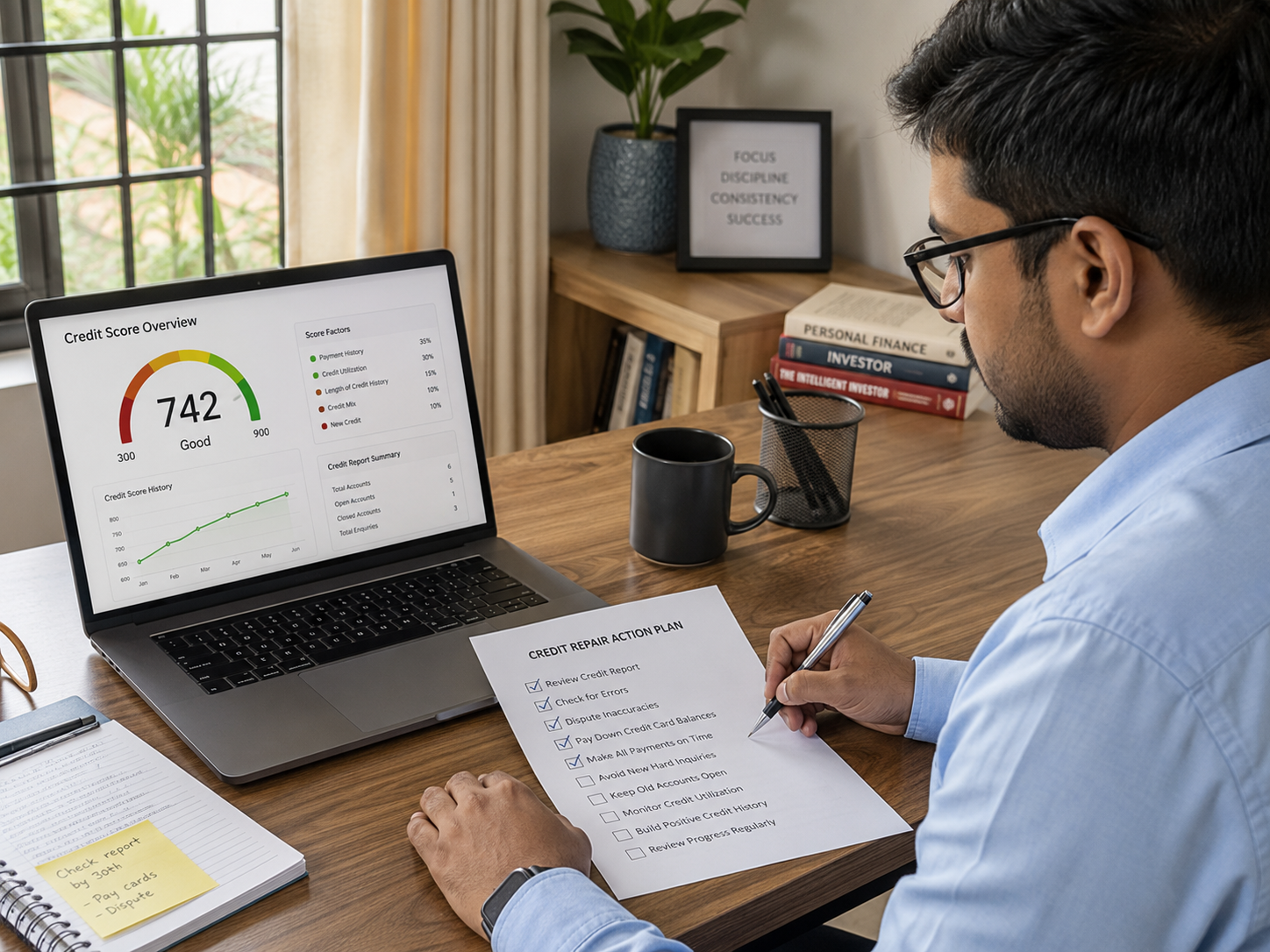

DPD is reported every month. CIBIL keeps the last 36 months of your record that is 3 full years of payment history.

How to Get Your Detailed CIBIL Report

As per RBI rules, you are entitled to one free detailed CIBIL report every calendar year. Here is how to get it:

- Go to the official CIBIL website: cibil.com

- Click "Get Your Free CIBIL Score and Report."

- Fill in your PAN, full name, date of birth, and registered mobile number.

- Verify with the OTP sent to your mobile.

- Answer 3–4 security questions about your past loans or credit cards.

- Your full report opens on screen. Download the PDF.

Note on the PDF password: It is usually your name (in caps) followed by your birth year. Check the email CIBIL sends you.

For more frequent checks, most banks now show your CIBIL score free inside their app. You can also buy a paid subscription on cibil.com if you want monthly access.

FREED Expert Tip

If you see XXX on your report, don't panic. It only means the Bank skipped a month of reporting. It does not hurt your score.

Talk to a FREED ExpertWhere to Find Your DPD Entries in the Report

DPD entries live inside the "Account Information" section of your CIBIL report. Every loan and every credit card has its own block.

Inside each block, there is a small grid. It shows the last 36 months, one cell per month. The number inside each cell tells you how many days late you were that month. Green cells mean on-time. Orange or red mean late.

Read across the grid from left to right. That is your full 3-year payment story for that account.

How to Clear DPD in CIBIL Report Step by Step

Here is the truth first: a genuine DPD entry where you actually paid late cannot be removed. It stays on your CIBIL report for 36 months from the month of delay. That is a hard rule set by credit bureaus, not something any company can override.

But its impact on your score generally reduces over time. Its weight on your score reduces over time. And there are real steps you can take right now.

Step 1: Pay All Overdue Amounts Right Away Clear every pending EMI and credit card bill. This stops new DPD entries from being added each month.

Step 2: Set Up Auto-Debit (NACH Mandate) for Every EMI NACH mandate (auto-payment permission) tells your bank to deduct the EMI automatically every month. Set it for every loan and card. One less thing to forget.

Step 3: Keep All Payments on Time for the Next 6–12 Months Consistent on-time payments reduce the weight of old DPD entries on your score.Consistent repayment behaviour gradually improves your credit profile over time. Each month of clean payment chips away at the damage.

Step 4: Keep Credit Card Usage Below 30% of the Limit Credit utilization (percentage of card limit used) is the second-biggest factor in your CIBIL score after payment history. Indicative only actual scoring methodology varies. Using more than 30% regularly hurts the score even if you pay on time.

Step 5: Do Not Apply for Many New Loans or Cards at Once Every application triggers a hard inquiry (a formal check on your CIBIL by the bank). Multiple hard inquiries within a short period may affect your credit profile further.

Step 6: Check Your CIBIL Report Every 3 Months for Errors Wrong DPD entries do happen a bank reported incorrectly, or your payment was credited a day late. Catching them early lets you dispute fast.

Step 7: Talk to Your Bank if You Are Still Struggling Banks and NBFCs may offer a new repayment schedule (restructuring changing how you repay), a short pause (moratorium), or other options. Ask before you miss the next EMI.

If you have several loans and on-time payment has become genuinely difficult, FREED's counsellors can look at your full picture and help find an option that fits at no cost, before any commitment.

How to Dispute a Wrong DPD Entry on Your CIBIL Report

Sometimes a DPD entry shows up that shouldn't be there. The Bank reported wrong data. Or your payment was on time but got credited a day late. Or it's not even your account.

You can dispute it. Here is how:

- Download your latest CIBIL report from cibil.com.

- Mark every entry that looks wrong, check account numbers, dates, amounts, and DPD values carefully.

- Go to cibil.com → "Raise a Dispute" and fill the online form.

- Attach proof: bank statements, payment receipts, NOC (clearance letter) if the account is already closed.

- Note your control number; it is printed at the top of every CIBIL report. You will need it to track the dispute.

- The dispute process generally involves review and response within 30 days.

- If the dispute is upheld, the Bank corrects the wrong DPD and CIBIL updates your report.

If the Bank does not respond within 30 days, escalate to the RBI Ombudsman.

What the Law Says

Under RBI's Credit Information Companies (Regulation) Act, 2005, you have the right to one free detailed credit report every calendar year. Credit bureaus generally process disputes within 30 days under RBI-regulated timelines.

Know Your Rights as a BorrowerHow Long Does DPD Stay on Your CIBIL Report?

A DPD entry stays for 36 months (3 years) from the month the delay was first reported. Even after you clear the overdue amount, the entry stays visible for that full period.

After 36 months, the entry drops off automatically. No action needed on your end.

The good news: as a DPD entry gets older, its impact on your score reduces. A 90-day DPD from 30 months ago hurts your score much less than a 90-day DPD from last month. Recovery is gradual, but it is real.

Many borrowers see gradual improvement over time with disciplined repayment behaviour. Indicative only. Actual recovery depends on individual profile, credit mix, and Bank/NBFC reporting.

How DPD Affects Your CIBIL Score and Loan Approval

DPD Value | What It Means | Typical Score Impact* | Loan Approval Outlook |

000 / STD | Paid on time | No impact | High chance of approval at best rates |

1–29 days | Slightly late | Mild drop | Mostly approved, may face higher interest |

30 days | Late by a month | Moderate drop | Approval depends on overall profile |

60 days | Late by 2 months | Noticeable drop | Higher scrutiny, tighter terms |

90+ days | Loan marked as bad (NPA loan marked as bad by the bank after 90 days) | Sharp drop | Very tough to get new credit |

Settled / Written-off | Closed for less than owed / Bank gave up recovering | Heaviest impact | Most Banks reject for 4–7 years |

All figures indicative only. Actual score impact varies by individual profile, credit mix, and CIBIL's internal scoring methodology.

When DPD Has Become a Bigger Problem Than You Can Solve Alone

For some borrowers, DPD is a one-time mistake. A forgotten EMI. An auto-debit that bounced. One rough patch, then back on track.

For others, DPD has been piling up across two or three loans not because of carelessness, but because there is simply not enough salary left at the end of the month to pay everything.

If your DPD entries are growing every month, recovery calls have started, and your total EMIs have already crossed 50% of your take-home salary then the standard advice of "pay on time and wait 36 months" does not match your situation.

That is when it helps to look at the full picture, not just one loan at a time.

FREED works with thousands of Indians who have reached this same point. The counsellors look at every loan and card you carry, talk to your Banks and NBFCs on your behalf, and help find an option that genuinely fits. That could mean changing how you repay (restructuring), combining all loans into one (consolidation), or only when repaying in full is truly not possible settlement (closing a loan for less than owed).

Settlement is not something a borrower chooses out of preference. Banks only consider it when you are in a genuine financial difficulty and are truly unable to repay the full amount. It is a last resort, not a shortcut.

FREED's counsellors handle the back-and-forth with the Bank, help put your documents together, and get the settlement letter worded correctly so the documentation and reporting process is handled carefully afterward.

The first conversation with FREED is free. No commitment needed.

5 Common Mistakes Borrowers Make While Trying to Clear DPD

- 1

Taking a new loan to pay the old one.

The DPD remains, and repayment pressure may increase further.

- 2

Ignoring small credit card balances.

Even ₹500 overdue can trigger a new DPD entry every month.

- 3

Applying for many cards or loans at the same time.

Every application triggers a hard inquiry. Multiple inquiries in a short window drop the score further.

- 4

Not setting up auto-debit after a missed EMI.

One bounce becomes two. Set up NACH mandate (auto-payment permission) immediately after clearing dues.

- 5

Believing ads that promise "DPD removal in 24 hours."

These are scams. A genuine DPD cannot be removed. Only wrong or inaccurate entries can be disputed and corrected through CIBIL's official process.

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions