Hero Fincorp Loan Settlement: Process, Timeline and What to Expect

Hero Fincorp loan settlement is a formal agreement between you and Hero Fincorp, an NBFC (non-banking financial company), where they accept a reduced lump-sum payment to resolve a loan you are genuinely unable to repay in full. It is a last resort for borrowers in real financial distress. It is not a shortcut or a trick.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

Hero Fincorp loan settlement, also called OTS (one-time settlement, meaning you pay once and the matter ends), lets eligible borrowers resolve outstanding debt for less than the full amount owed.

Settlement discussions are generally considered after prolonged non-payment, depending on the lender's assessment.

The "Settled" status stays on your CIBIL report for up to 7 years from the date of settlement.

Settlement is only possible if you can prove genuine financial hardship: job loss, medical crisis, business failure, or similar.

REED has helped 60,000+ customers navigate debt resolution across banks and NBFCs, including Hero Fincorp.

What Is Hero Fincorp Loan Settlement?

Settlement is not something a borrower chooses out of preference. Hero Fincorp and other financial companies only consider it when you are in genuine financial difficulty and are truly unable to repay the full amount. It is a last resort, not a shortcut.

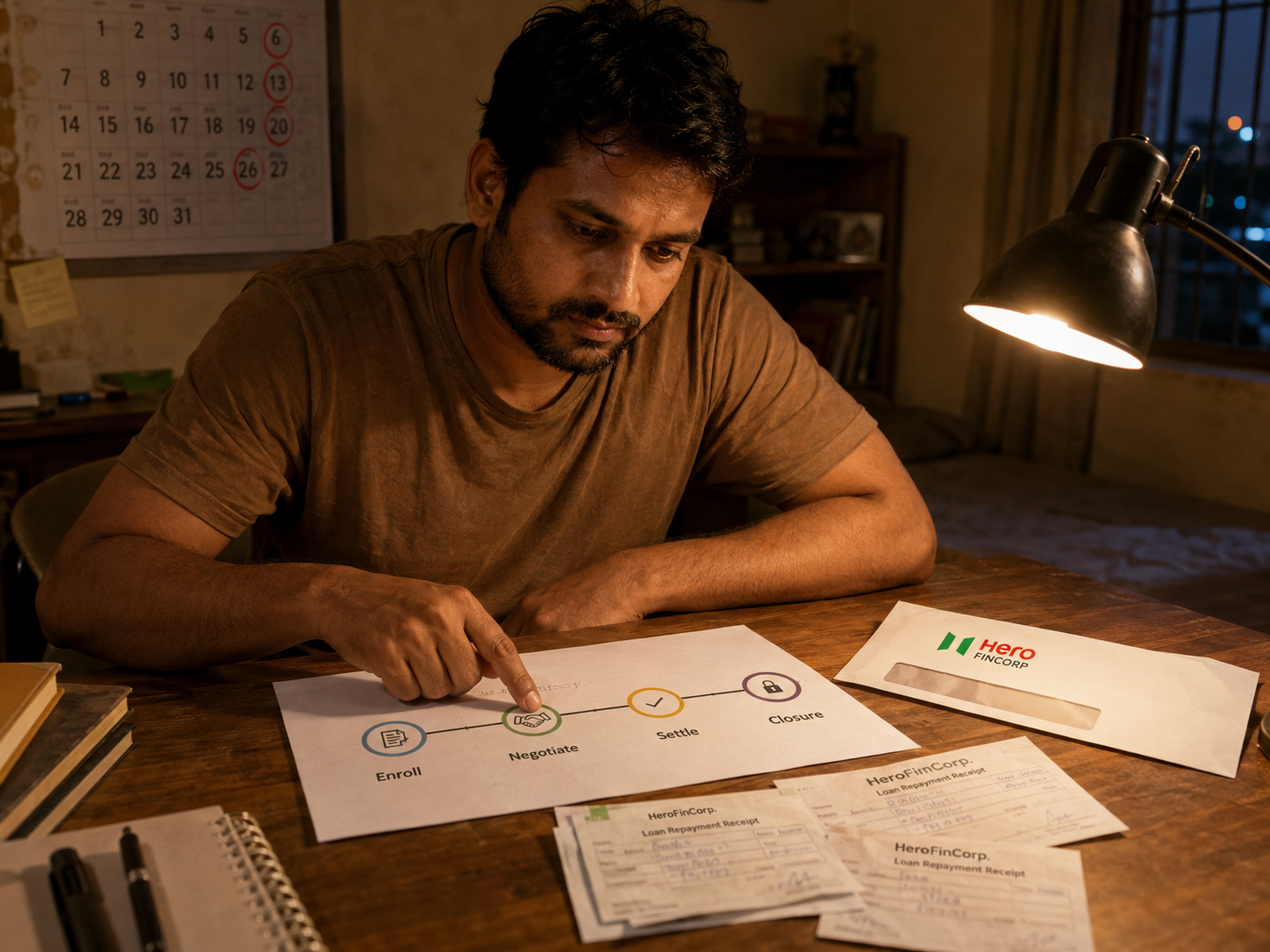

Hero Fincorp is an NBFC, not a bank. This distinction matters because NBFCs operate under slightly different RBI regulations than scheduled commercial banks, though the core settlement mechanism is similar. The formal process Hero Fincorp uses is called OTS (one-time settlement): you propose a reduced lump-sum amount, Hero Fincorp evaluates it, and if agreed, the payment resolves the loan permanently.

What does "resolved" mean here? The final settlement amount depends on Hero Fincorp's assessment of your individual circumstances. Once you pay the agreed amount and collect your NDC (No Dues Certificate, which is the clearance letter from Hero Fincorp confirming the matter is fully resolved), Hero Fincorp's claim on that loan ends.

This is different from full loan closure. Full closure means you paid everything owed: principal, interest, and all charges. Your CIBIL shows "Closed." Settlement means Hero Fincorp accepted less. Your CIBIL shows "Settled." The financial outcome and the credit record impact are different, and you need to understand both before deciding.

Settlement applies to unsecured personal loans from Hero Fincorp. For two-wheeler loans, additional considerations apply because those are secured loans where the vehicle can be repossessed. Hero Fincorp only considers settlement when the account has turned NPA after 90 days of non-payment and the borrower has genuine documented hardship.FREED helps borrowers settle their unpaid/overdue loans at up to 50% less.* , depending on your case. The "Settled" CIBIL mark stays for up to 7 years.

Why Does Hero Fincorp Settlement Happen?

Nobody wakes up wanting to settle a loan. The situations that push borrowers here are real: a sudden job loss with no severance, a medical emergency that drained savings, a business that shut down during a bad patch, or an irregular income that finally ran out after months of trying to keep up.

Hero Fincorp's borrower base is wide. They offer personal loans up to ₹5,00,000 with repayment times of 12 to 36 months at interest rates starting from 1.75% per month. These are high-cost products. When income disrupts, even a short gap hits fast. A borrower who was managing the EMI on a regular salary can fall behind quickly after one missed month.

The pattern is usually the same. A few missed EMIs. Recovery calls starting. Legal notices following. Income still not restored. By the time many borrowers look at settlement, they have already tried paying whatever they could for months. Settlement is not a choice they took lightly.

What matters here is documentation. Hero Fincorp, like all financial companies, distinguishes between borrowers who cannot pay and those who will not pay. The first group gets considered for settlement. The second group faces continued recovery action and legal proceedings. Your ability to prove your hardship in writing is what determines which group you fall into.

FREED Expert Tip

If a large share of your take-home salary is already going toward loan repayments of your take-home salary, speak to a counsellor before the first missed payment. Options shrink significantly after you have defaulted.

Talk to a FREED ExpertWhat Are the Signs You May Need to Consider Settlement?

These are not automatic triggers. They are situations that suggest you should get proper guidance before things get worse.

- Recovery calls from Hero Fincorp are becoming frequent, persistent, or threatening. When calls cross into abusive or harassing behaviour, that is a separate issue covered by RBI fair practice guidelines.

- You have received a formal arbitration notice from Hero Fincorp. Hero Fincorp commonly includes arbitration clauses in their loan agreements, with the arbitration seat typically in New Delhi.

- You have received a Section 138 notice under the Negotiable Instruments Act Section 138 makes a bounced cheque or NACH mandate dishonour a criminal matter, not just a civil one. [(NI Act Section 138: https://indiankanoon.org/doc/1823824/)]

- You have missed 3 or more consecutive EMIs and your income has not recovered.

- You have no assets to liquidate and no family support available.

- You have already tried talking to Hero Fincorp's customer care and received no resolution.

If several of these situations apply, it may be worth speaking with an expert to understand your options. It does not mean you must settle. It means you need a clear picture of your options.

How Does Hero Fincorp Loan Settlement Work?

- 1

Check if You Are Eligible

Assess your situation honestly. Hero Fincorp only considers settlement for genuine hardship: job loss, medical emergency, business failure, or similar documented difficulty. If you have income or assets and are choosing not to pay, Hero Fincorp will not settle. Being clear-eyed about this before approaching them saves time.

- 2

Gather Your Documents

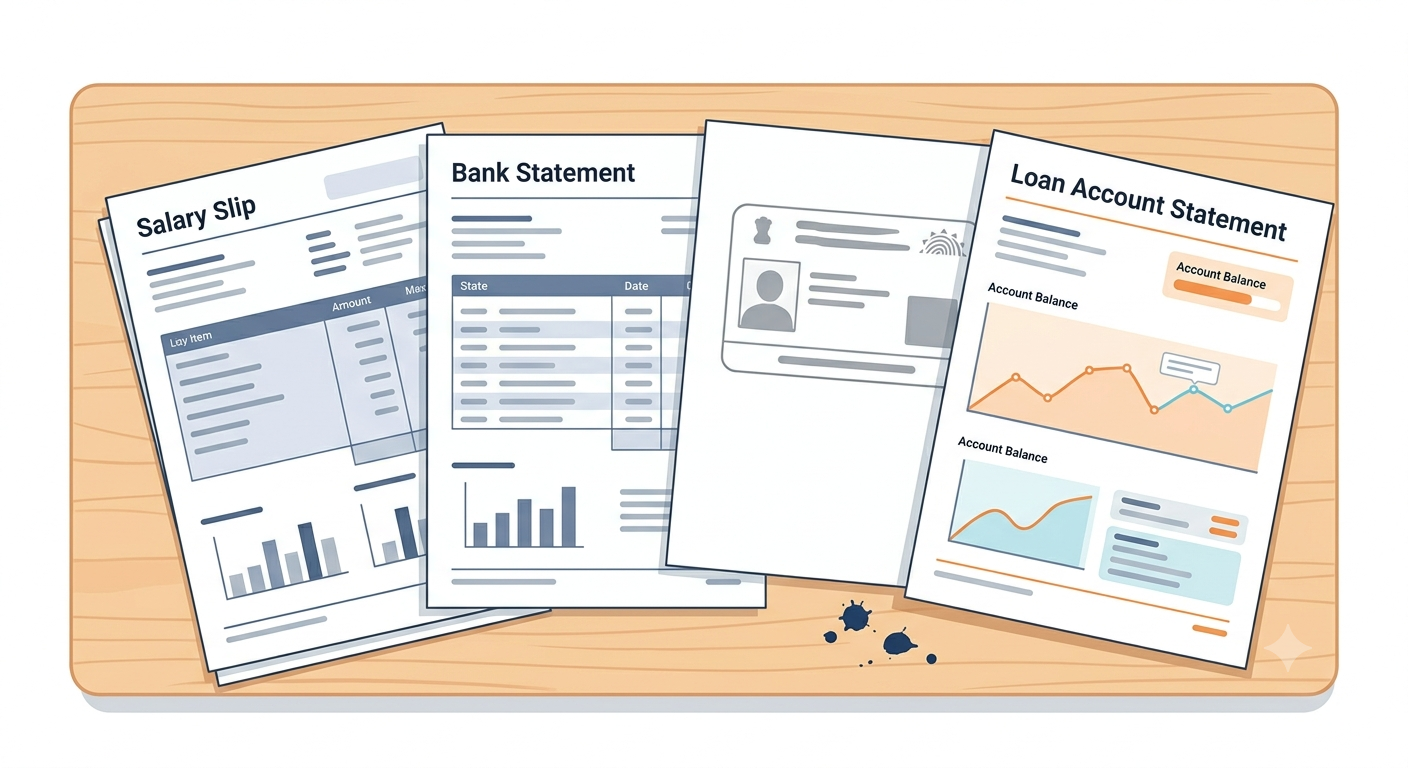

You will need KYC documents (PAN and Aadhaar), your loan account statement showing the current outstanding amount, proof of financial hardship (a termination letter, medical bills, bank statements showing income has stopped, or business loss statements), and copies of any legal notices already received. For two-wheeler loans, also keep the vehicle RC ready.

- 3

Contact Hero Fincorp's Collections Team in Writing

Reach out to their collections or recovery department directly, not your nearest branch. Put everything on email. WhatsApp promises or verbal assurances from field agents carry no legal weight. State your loan account number, your situation, and that you want to discuss an OTS (one-time settlement). Keep every reply and acknowledgement.

- 4

Submit a Formal OTS Proposal

Write a short, clear proposal: your hardship, the amount you can pay, and the timeline within which you can pay it. Attach all supporting documents. This is a formal document, not a casual request. The clearer and more specific your case, the more seriously it will be reviewed.

- 5

Negotiate the Terms

Hero Fincorp may respond with a revised proposal depending on your circumstances. This back-and-forth is normal and expected. The final settlement amount depends on your outstanding balance, how long the account has been in default, and your documented ability to pay. Be patient and respond in writing each time.

- 6

Get the Settlement Letter Before Paying Anything

Once terms are agreed, Hero Fincorp issues a formal settlement letter on their official letterhead. Read every clause, especially the payment deadline and what happens if you miss it. Only pay after this letter is in your hand. Never pay before.

- 7

Pay and Collect Your NDC

Pay the agreed amount directly to the loan account via NEFT, RTGS, or demand draft. Keep the payment receipt permanently. Then follow up specifically for your NDC (No Dues Certificate, the clearance letter confirming full resolution). This is your legal proof. Track the CIBIL update at 45 to 60 days after payment. If this process feels difficult to navigate or

How Long Does Hero Fincorp Settlement Take?

Expect the process to take longer than you hope. Here is a realistic picture.

The starting point is NPA classification, which typically happens after 90 days of non-payment. Before that threshold, Hero Fincorp is more likely to offer restructuring than settlement. Once the account is NPA, the collections focus shifts from EMI recovery to partial recovery, and settlement becomes a real possibility.

After you initiate contact, Hero Fincorp's internal review takes time. The negotiation phase, from first contact to agreed terms, typically runs 2 to 4 weeks (indicative; actual timelines vary). This can stretch longer if documentation is incomplete, if there are multiple rounds of counter-offers, or if Hero Fincorp's recovery team is handling a high volume of cases.

After agreement, the payment window is stated in the settlement letter itself, commonly 15 to 30 days, though this varies by lender and can be negotiated. Miss this window and the offer typically lapses.

From the first missed payment to receiving the NDC, the full process realistically takes 1 to 3 months, sometimes more. The "Settled" CIBIL mark then stays for up to 7 years from the date of settlement.

The single biggest delay factor is the borrower: incomplete documents, delayed responses, or missing the payment window after agreement. Keep your paperwork ready from the start and respond to every communication promptly.

What Happens to Your CIBIL Score After Settlement?

Do not skip this section. The CIBIL impact of settlement is the most important thing to understand before you proceed.

After Hero Fincorp settlement, your loan account is marked "Settled" on your CIBIL report. Not "Closed." "Settled." The distinction matters. "Closed" means you paid everything in full. "Settled" means the financial company accepted less than what you owed. Any bank or NBFC checking your report will see it clearly.

This mark stays for up to 7 years. During this period, new unsecured loan applications will be harder. Some banks decline outright. Others may approve with a co-applicant or at higher interest rates.

How does "Settled" compare to the alternatives? "Written Off" means Hero Fincorp gave up on recovering the amount and removed it from their books as a loss. Both are negative marks. But "Written Off" signals complete recovery failure. "Settled" shows partial resolution. If your account has already been in default for months, your score has already dropped significantly. Settlement stops further damage; it does not add a new one on top of a clean record.

The exact drop depends on your starting score and the rest of your credit profile. Paying any remaining active loans on time, keeping credit card usage below 30% of the limit, and avoiding fresh defaults. A secured credit card backed by a fixed deposit can help establish a positive payment track during this period.

You cannot remove the "Settled" mark early unless there is a factual error in the reporting. Do not let anyone tell you otherwise.

What the Law Says

Under RBI fair practice guidelines, a financial company must not engage in recovery practices that are harassing, abusive, or conducted at odd hours. If Hero Fincorp's agents cross this line, you have the right to file a formal complaint.

Read MoreWhat Are Your Options Before You Settle?

Restructuring | Loan Settlement (OTS) | |

What it does | Changes the loan plan: lower EMI or longer repayment time | Resolves the loan by paying a reduced one-time amount |

Total amount paid | Full principal and interest, often more overall | Significantly reduced |

CIBIL impact | Moderate, shows as "Restructured" | High, shows as "Settled" for up to 7 years |

Best for | Borrowers who can still pay but need breathing room | Borrowers who genuinely cannot repay |

Availability | Available earlier in the default cycle | Typically after NPA classification, 90+ days |

Actual terms depend on Hero Fincorp's assessment of your case. FREED is not a loan provider. No outcome is guaranteed. Please verify directly with Hero Fincorp.

How FREED Helps With Hero Fincorp Loan Settlement

Negotiating with Hero Fincorp's collections team is not simple. There are multiple rounds of back-and-forth, documents to prepare, offer letters to read carefully, and follow-ups that can go unanswered for weeks. FREED's counsellors have worked through this process with 60,000+ customers across banks and NBFCs, managing over ₹3,200 crore in debt.

What FREED does: reviews your complete debt picture and helps you understand whether settlement is the right route or whether another option suits your situation first. If settlement is the right call, FREED helps you prepare the OTS proposal and the hardship documentation. FREED handles the communication with Hero Fincorp's recovery team, checks every offer letter clause before you sign, and follows up for the NDC after payment. The CIBIL update is tracked at the 45-day mark.

If Hero Fincorp's agents have been harassing or abusive, FREED can help you understand your rights under RBI fair practice guidelines and help you draft a formal complaint through the right channels. FREED does not directly stop recovery calls, but it gives you the tools to respond correctly.

FREED charges fees only when settlement is successfully completed. There is no upfront charge.

FREED covers unsecured loans only: personal loans, credit cards, BNPL, and loan apps. Two-wheeler loans from Hero Fincorp are secured, and the approach there differs.

Disclaimer: Settlement waiver up to 50%* is indicative, not a guarantee. Final terms decided by Hero Fincorp. FREED is not a Loan Provider. No outcome guaranteed. Verify directly with Hero Fincorp.

Already Getting Recovery Calls From Hero Fincorp?

Find out your options with a quick free call.

Book a Free CallWhat Helps During the Hero Fincorp Settlement Process?

A few practical things that make the process go more smoothly.

Keep written records of everything. Every email, every WhatsApp message, every letter received. Date and time it. Always ask for important settlement terms in writing. If it is not in writing, it does not count.

Never pay before the formal settlement letter arrives. The letter must be on Hero Fincorp's official letterhead. It must state the agreed amount, the payment deadline, and the "full and final" clause confirming no further claims will be made. If any of that is missing, go back and ask for it before paying anything.

Do not take a new loan to pay off the settlement amount. This replaces one debt with another and often worsens the situation. Pay from savings or family support if possible.

Respond to legal notices. Do not ignore them. Ignoring an arbitration notice or a Section 138 notice does not make it go away. Responding, even to say you are working on a resolution, is always better than silence.

Prepare your documents before approaching Hero Fincorp. Going in with a complete file means the process moves faster. A missing document is the most common reason negotiations stall.

About FREED

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions