Budgeting Tips for Better Financial Goals

Want to buy a house? Clear your debt? Build savings? None of it happens without a plan. These practical budgeting tips will help you set real financial goals - and actually reach them.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

A goal without a number and a deadline is just a wish.

Separating money into goal-based buckets makes saving automatic, not willpower-dependent.

Invisible expenses - subscriptions, auto-renewals, forgotten EMIs, quietly drain 10–15% of income.

You can't save your way to wealth if high-interest debt is eating your income first.

FREED helps reduce EMI burden so your budget can finally support your goals.

Why Most Financial Goals Fail

"I want to save more." "I want to buy a house someday." "I want to clear my credit card debt."

Most people have goals like these. Very few reach them.

The reason is almost never income. It's the missing link between the goal and the daily money decision.

A goal without a number is vague. A vague goal has no place in a budget. And a budget with no goal is just a list of expenses, it doesn't tell you where you're going.

The tips below fix exactly this. They connect your daily spending to the future you actually want.

- 1

Tip 1: Set Goals Before You Set a Budget

Most people build a budget and then wonder what to do with the leftover money. Flip it. Start with your goals. Then build the budget around them. Ask yourself three questions: What do I want to achieve in the next 12 months? What do I want in the next 3–5 years? What does my life need to look like in

- 2

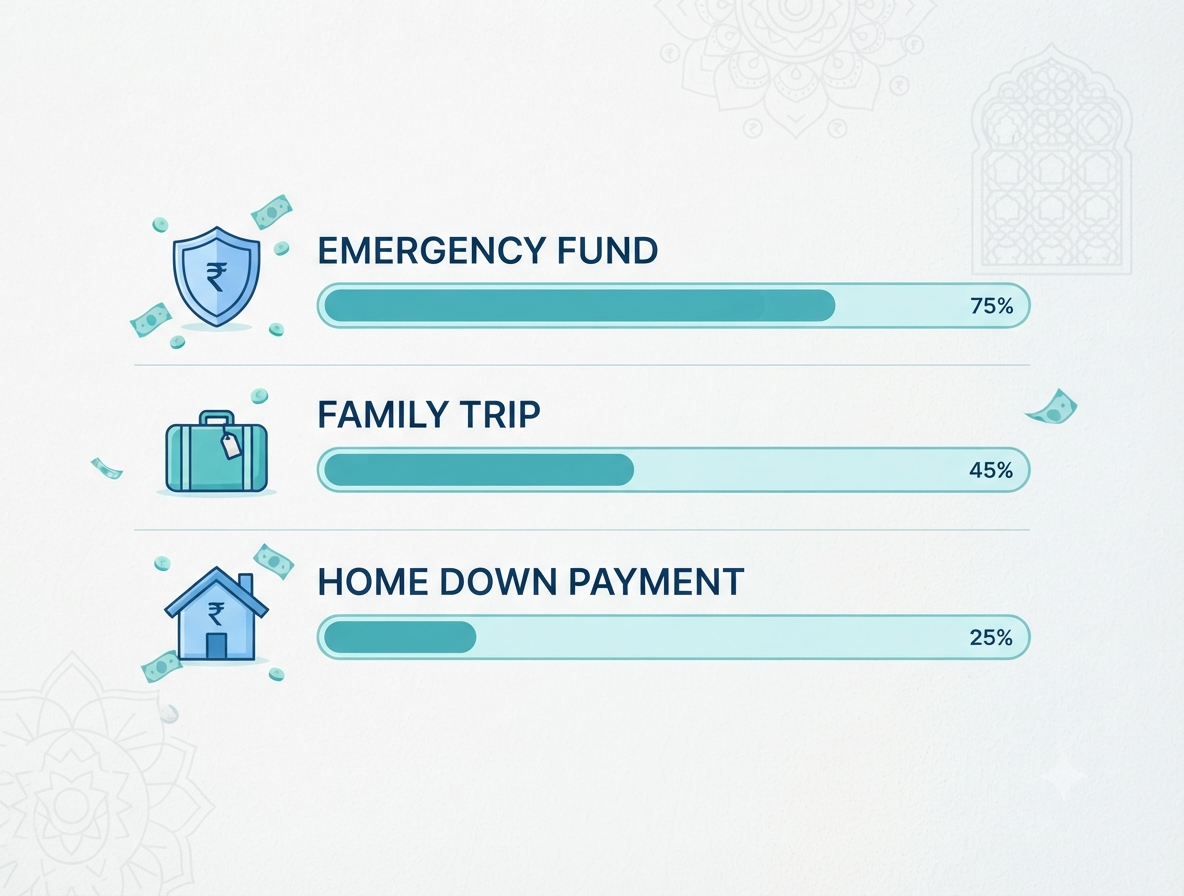

Tip 2: Separate Your Goals Into Buckets

One savings account for everything doesn't work. You can't tell which money is for emergencies, which is for the trip, and which is for the future. The moment you dip into "savings" for any reason, all goals take a hit. Instead, create separate buckets - mentally or physically: Bucket 1 - Emergency Fund. 3 months of expenses. Never touched unless

- 3

Tip 3: Treat Savings Like a Bill

If savings is what's left after spending, you'll save almost nothing. The moment salary arrives before rent, before groceries, before anything transfer your savings amount out. This is non-negotiable. Think of it like your electricity bill or your EMI. It has to be paid. The only difference is: you're paying yourself. Set up a standing instruction or SIP to make

- 4

Tip 4: Cut Invisible Expenses First

Before you cut dining out or entertainment, look for expenses you're not even aware of. These are called invisible expenses. They don't feel like decisions but they add up to thousands every year. Common invisible expenses in India: OTT subscriptions you forgot to cancel (Netflix, Hotstar, Spotify, Amazon Prime often 3–4 running together) Auto-renewal of apps and cloud storage Bank

- 5

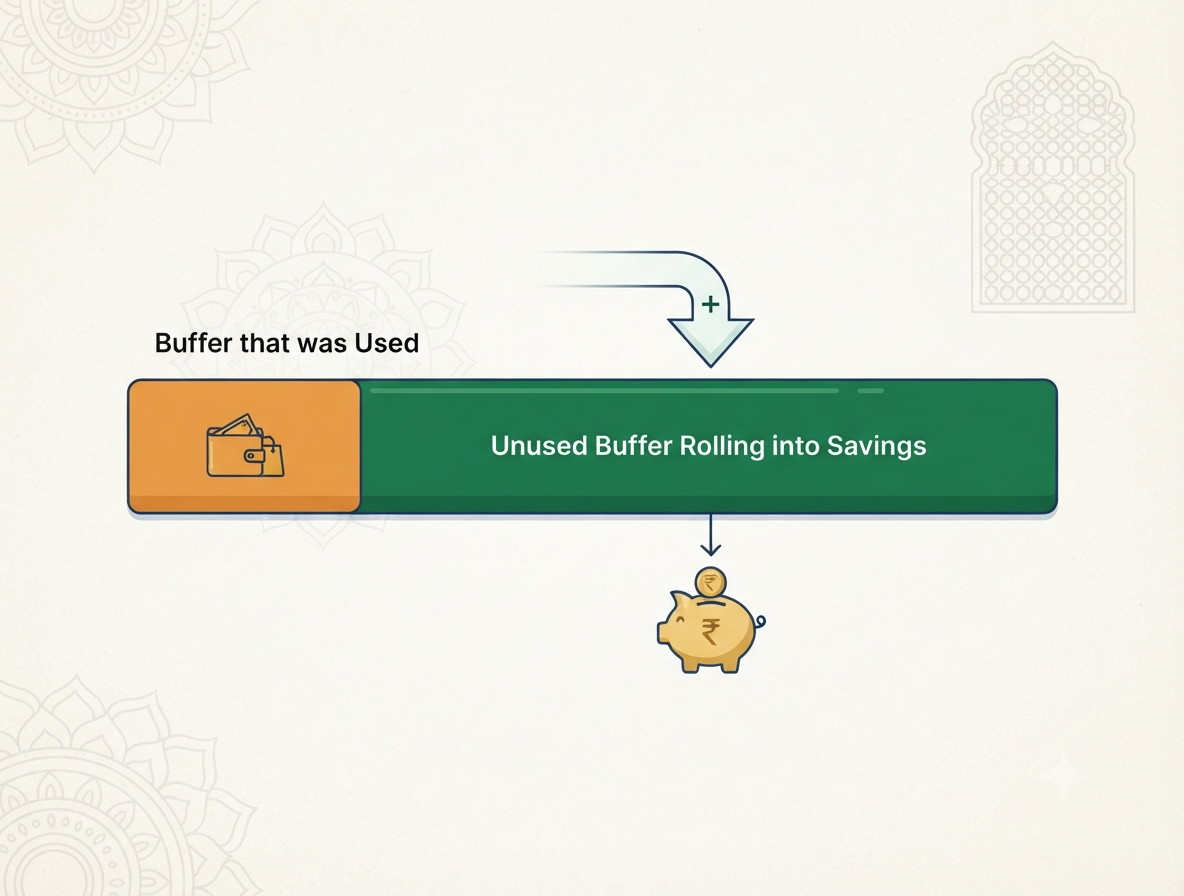

Tip 5: Build a Buffer - Not Just a Budget

A budget tells you the plan. A buffer saves the plan when life doesn't follow the script. Every month has surprises, a medical expense, a vehicle repair, a family emergency, a higher electricity bill in summer. Without a buffer, these surprises become debt. Build a small monthly buffer into your budget, ₹1,000 to ₹3,000, depending on income as a "surprise

- 6

Tip 6: Review Monthly, Adjust Quarterly

A budget is not a one-time exercise. It's a living document. At the end of every month, spend 10–15 minutes asking: What did I plan to spend? What did I actually spend? Where was the gap? Did I hit my savings target? Don't judge yourself. Just observe. Patterns become obvious within 2–3 months. Every 3 months, do a bigger review:

- 7

Tip 7: Clear Debt Before Chasing Big Goals

Here's an uncomfortable truth: if you're carrying high-interest debt credit card dues, personal loans at 18–24% interest, BNPL balances, no investment or savings goal can outrun that interest rate. Every ₹100 you put in a mutual fund while carrying credit card debt at 36% annual interest is a losing trade. The priority order for most Indians with debt: 1) Build

What the Law Says

Auto-renewal subscriptions and recurring mandates on your bank account must be notified to you 24 hours in advance - as per RBI e-mandate guidelines. If a company charges you without this notification, you can raise a dispute with your bank and claim a reversal. You are also entitled to cancel any e-mandate at any time through your bank's net banking or mobile app.

Know your banking rights

When Debt Is Blocking Every Goal

Sometimes the math simply doesn't work.

You want to save. You want to invest. You have goals. But every rupee is going into EMIs and there's nothing left.

This isn't a budgeting problem anymore. It's a debt load problem.

FREED helps people in exactly this situation. We look at all your existing loans, credit card dues, and EMIs and find a way to reduce the total monthly outgo. Through consolidation (one lower EMI replacing many) or resolution (settling for less than you owe), we create the breathing room your budget needs.

Once your EMI burden drops, your goals become reachable. Your budget starts working. And money stops feeling like a source of anxiety.

Over 10,000 Indians have made that shift with FREED's help. The first conversation is free.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions