Budgeting: The Basics and a Little More

Most people think budgeting means cutting down on everything fun. It doesn't. It just means telling your money where to go - before it disappears on its own.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

A budget is simply a plan for your money - nothing more, nothing less.

Most people fail at budgeting because they don't track what they actually spend.

The goal is not to spend zero - it's to spend with intention.

If EMIs take up more than 40–50% of your income, you need debt help, not just a budget.

Small, consistent money habits beat big, complicated financial plans every time.

What Is a Budget, Really?

Let's keep this simple.

A budget is a list. Income on one side. Expenses on the other.

That's it.

You're not giving up chai. You're not counting every single rupee forever. You're just making sure you know where your money is going before it goes there.

Most people don't have a budget. They have a rough feeling about money. That feeling is usually wrong and by the 20th of the month, it becomes panic.

A budget replaces the feeling with facts.

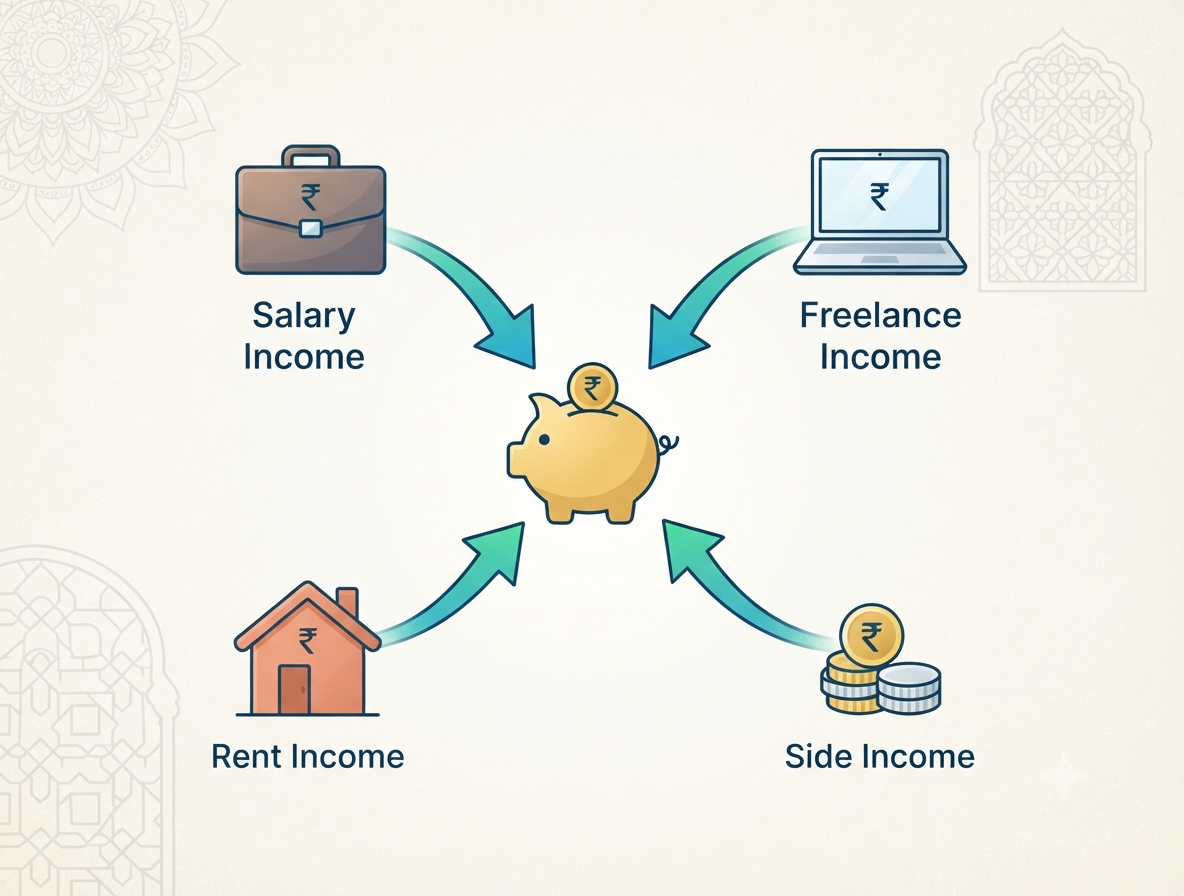

Step 1: Know What Comes In

Before you plan anything, you need one number: your monthly take-home income.

Not your CTC. Not your gross salary. What actually lands in your account every month, after tax and PF deductions.

If your income is irregular freelance, business, daily wages use the average of your last 3 months. Or use the lowest month as your base. Better to be safe.

Write this number down. This is your starting point.

Step 2: Know What Goes Out

Now list everything you spend money on in a month.

Divide it into two types:

Fixed expenses are the same every month. Rent, EMIs, school fees, insurance premiums, subscriptions.

Variable expenses change month to month. Groceries, transport, dining out, clothes, medicines, entertainment.

Don't guess. Look at your last month's bank statement and UPI history. This is where most people get a shock.

Write every number down. Even the small ones Swiggy, auto, recharge. They add up faster than you think.

FREED Expert Tip: Most people underestimate variable expenses by 20–30%. When in doubt, round up - not down. An honest budget always beats an optimistic one.

Step 3: Find the Gap

Now subtract your total expenses from your income.

Income – Expenses = Your Gap

Three things can happen here:

Positive gap - you have money left over. Good. This goes into savings or debt repayment.

Zero gap - every rupee is accounted for. Okay. But there's no room for surprises. You need to find cuts.

Negative gap - you're spending more than you earn. This is a serious problem and it's more common than people admit.

If your gap is negative, don't panic. But don't ignore it either. Something has to change either income goes up, or expenses come down.

Step 4: Make a Plan That Actually Works

Here's a simple structure that works for most Indian households:

Category | Ideal % of Income |

Needs (rent, groceries, bills, EMIs) | 50% |

Wants (dining, shopping, entertainment) | 20–30% |

Savings & investments | 20% |

This is the 50-30-20 framework. It's a guide, not a law.

If your EMIs alone are 40–50% of income, the "needs" category is already over budget before food and rent. That's a debt problem not a budgeting problem. We'll come to that.

For everyone else: start with this split. Adjust based on your real expenses. The goal is direction, not perfection.

What the Law Says:

Under RBI guidelines, banks must clearly disclose the total interest cost of any loan before you sign. You have the legal right to a loan amortisation schedule - a month-by-month breakdown of exactly what you'll pay. Always ask for this before taking any EMI. If a lender refuses, you can escalate to the RBI Banking Ombudsman.

Know your rights as a borrower

The Little More - Beyond Basic Budgeting

Once you have the basics down, here's what separates people who just budget from people who actually build wealth.

1. Build your emergency fund first. Before investments, before anything - save 3 months of total expenses in a separate account. Don't touch it unless there's a real emergency. This is the fund that stops debt from happening.

2. Review your budget every month. Life changes. A budget that worked in January may not work in March. Spend 15 minutes at the end of each month comparing what you planned vs. what actually happened. Adjust accordingly.

3. Watch out for lifestyle creep. When income goes up, expenses tend to go up too - silently. A new phone. A bigger flat. More eating out. This is lifestyle creep. It's not wrong to spend more as you earn more - but do it intentionally, not automatically.

4. Automate what you can. Set up auto-transfers for savings. Auto-pay for EMIs. The less willpower budgeting requires, the more sustainable it becomes.

5. Have one "guilt-free" spending category. If your budget is 100% discipline with zero joy, you'll quit. Allow yourself one category dining, movies, travel where you spend without guilt, within a fixed limit. This keeps budgeting human.

When Debt Makes Budgeting Impossible

There's a version of this problem that a budget can't fix alone.

If your EMIs, credit cards, personal loans, BNPL are eating 50% or more of your monthly income, there's no budget framework in the world that will give you breathing room.

In these situations, the problem isn't how you're spending. The problem is how much you owe.

FREED helps people in exactly this situation. We look at your full debt picture and find a way to reduce your monthly EMI burden - through consolidation or resolution. Once your debt load drops to a manageable level, budgeting becomes possible. Even easy.

Over 10,000 Indians have used FREED to get to that point. The first step is a free conversation.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions