Budgeting Mantras for Millennials

Earning decent money but still broke by the 25th? You're not alone. These simple budgeting mantras can help millennials take back control of their money - one payday at a time.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

Saving before spending is the single biggest habit shift millennials need.

EMIs and BNPL feel easy but they quietly eat your future salary.

Tracking your expenses for even 7 days changes how you see money.

If your EMIs cross 50% of income, budgeting alone won't fix it the debt needs to go first.

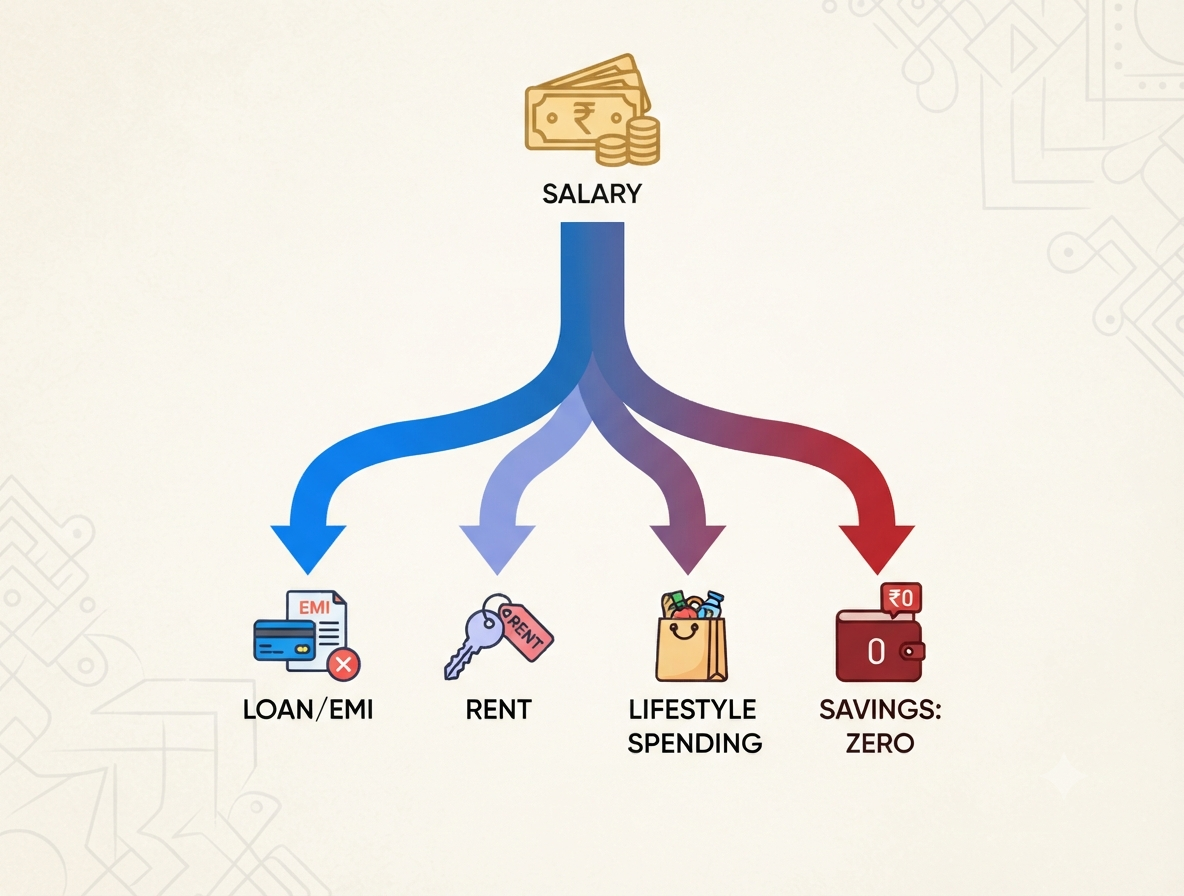

Why Do Millennials Struggle with Money?

You earn. You spend. Month ends. Repeat.

Sound familiar? Most millennials in India face this. It's not because they're careless. It's because nobody taught them how to handle money.

Add EMIs, credit cards, BNPL apps, and lifestyle pressure and suddenly your salary feels half its size before the month even starts.

The fix is not a fancy spreadsheet. It's a few simple money rules mantras you stick to, no matter what.

Mantra 1: Pay Yourself First

Most people save whatever is left after spending. That's backwards.

The rule: The moment your salary hits, move a fixed amount to savings. Before rent. Before groceries. Before anything.

Even ₹500 or ₹1,000 counts. The habit matters more than the amount right now.

This is called the "Pay Yourself First" rule. It works because your brain treats savings like a fixed expense - something that has to happen, not something you'll "try to do."

Start small. Automate it if you can (SIP, recurring deposit - anything). Don't touch it.

FREED Expert Tip

Set up an auto-transfer of even 5% of your salary on the day you get paid. You won't miss it - but in a year, you'll be glad it's there.

Talk to FREEDMantra 2: Never Spend What You Haven't Earned Yet

Credit cards. BNPL. "Pay in 3 instalments." "No cost EMI."

These are all versions of the same thing: spending tomorrow's money today.

It feels harmless. One purchase. Then another. Then the bill comes and you don't have it.

The mantra: If the money isn't in your account right now, don't spend it.

This doesn't mean never use a credit card. It means: only swipe if you can pay the full bill this month. Not the minimum. The full amount.

If you can't it's debt. Call it what it is.

Mantra 3: Track Before You Splurge

You don't need a complicated budget. You need 7 days of honesty.

For one week, write down every single rupee you spend. Chai. Auto. Zomato. Recharge. Everything.

By day 7, you'll see where your money is going - and it will surprise you.

Most millennials discover they're spending ₹3,000–₹5,000 a month on things they don't even remember buying.

The mantra: Track first. Cut second. Budget third.

You can't fix what you can't see.

What the Law Says

Did you know? Banks and NBFCs are legally required to give you a full breakdown of your loan charges if you ask. You have the right to know exactly what you're paying in interest, fees, and penalties. If they refuse, escalate to the RBI Banking Ombudsman.

Read more about your rights as a borrowerMantra 4: EMIs Are Not Free Money

"Sir, koi interest nahi. Easy EMI hai."

We've all heard this. And most of us have fallen for it.

Here's the truth: EMIs lock your future salary. Every EMI you take on is a promise your future self has to keep - even if they're broke, sick, or between jobs.

The mantra: Before taking any EMI, ask yourself - "Can I pay this if my income drops by 30%?"

If the answer is no, don't take it.

And if your current EMIs are already more than 40–50% of your monthly income - that's a red flag. Your budget will always fail until that number comes down.

Mantra 5: Save for Tomorrow, Not Just for Today

Emergency fund. Retirement. Health. These feel far away when you're 25 or 30.

They're not.

The mantra: Build 3 months of expenses as an emergency fund before you invest or buy anything big.

That's it. Three months. Not a year. Not a lakh. Just enough to survive 90 days without a salary.

This one fund will save you from going into debt when life throws a curveball - medical emergency, job loss, car breakdown. It happens to everyone.

Once that fund exists, you can start thinking about investments, goals, and growth.

FREED Expert Tip

If you have no emergency fund, don't invest in stocks yet. Build the safety net first. Investments can wait. Emergencies don't.

Talk to a FREED CounsellorAre You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

What to Do When Debt Is the Real Problem

Sometimes budgeting doesn't work not because you're bad at it, but because the debt load is too heavy.

If you're spending more than half your income on EMIs, budgeting feels like mopping a flooded floor without turning off the tap.

In that case, the first step is reducing the debt, not just managing it.

FREED's Debt Consolidation Program combines multiple high-interest debts into one lower monthly payment. This gives you breathing room to actually budget and save.

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions