Bank Loan Settlement: How to Approach Your Bank and What to Expect

Bank loan settlement is when a bank agrees to resolve your unpaid loan by accepting a lump sum payment that is less than the full amount you owe. The remaining balance is written off. This is also called an OTS — one-time settlement. It only becomes an option after you have missed payments and the loan has turned into an NPA (loan gone bad). It is a last resort, not a first step.

FREED India

Reviewed by FREED India, SEO Intern

Key summury

Bank loan settlement means resolving a loan for less than the full amount owed — it is a last resort when repayment is genuinely impossible.

Your account is marked "Settled" on your CIBIL report — not "Closed" — and this status can stay for up to 7 years.

Under RBI guidelines, every bank must have a board-approved policy for OTS (one-time settlement) — so the process is regulated, not arbitrary.

Recovery agents calling between 8 AM and 7 PM only; threatening or abusive calls are a violation of RBI guidelines and can be reported.

Alternatives — EMI restructuring, moratorium (temporary pause), tenure extension — must be explored before considering settlement.

Section 138 of the Negotiable Instruments Act (cheque bounce law, can go criminal) may apply if post-dated cheques were issued.

What Is Bank Loan Settlement and When Does It Apply?

Content direction: Open with empathy — acknowledge that anyone reading this is already in a difficult place. Define bank loan settlement in plain language. Clarify the difference between settlement and normal loan closure. Explain what OTS (one-time settlement) means. Be explicit: this is a LAST RESORT. Acknowledge that the bank does not offer settlement voluntarily — it happens after missed payments, NPA classification, and genuine hardship. Do NOT frame this as a clever way to pay less. Audience: Ramesh persona — defaulted or near-default, fear of recovery calls, shame.

Stats/data to include:

- A loan is classified as an NPA (loan gone bad) after 90 days of missed payments — writer to verify against current RBI norms

- Under RBI's compromise settlement framework, every bank must have a board-approved OTS policy — this is verified RBI regulation

- "Settled" tag on CIBIL stays for up to 7 years (source: CIBIL official FAQs — writer to verify current duration)

What Are the Bank Loan Settlement Rules in India?

Content direction: This section directly targets the secondary keyword "bank loan settlement rules." Cover the key RBI-regulated rules a borrower must know — not as a legal textbook, but as practical rights. Include: banks must have a board-approved OTS policy; settlement is the bank's discretion, not the borrower's right; recovery agents have contact-hour restrictions (8 AM–7 PM); no physical force, no abusive language; female borrowers may only be contacted by female recovery agents; banks must give written notice before appointing recovery agents; the borrower has the right to written documentation of any settlement offer. Be clear that RBI sets the framework but each bank decides its own OTS terms — so outcomes vary.

Stats/data to include:

- Recovery agent contact hours: 8 AM–7 PM only (source: RBI Fair Practices Code — writer to verify)

- 30-day written notice before appointing a recovery agent (reported in 2025 RBI guidelines — writer to verify directly from RBI circular)

- RBI Integrated Ombudsman complaint process exists for grievances — link to RBI Ombudsman page

What Is Bank Loan Settlement and When Does It Apply?

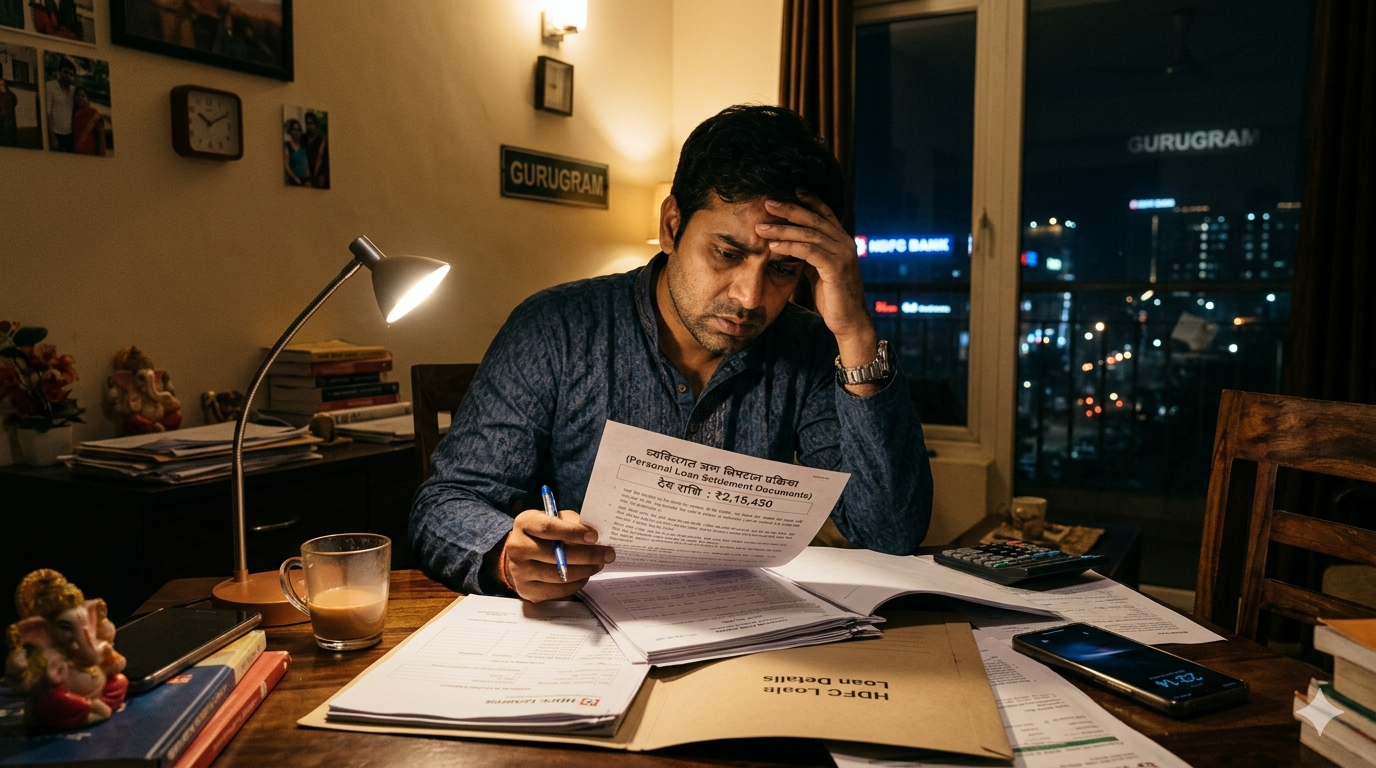

Settlement is not something a borrower chooses out of preference. Banks only consider it when you are in genuine financial difficulty and are truly unable to repay the full amount. It is a last resort, not a shortcut.

If you are reading this, you are probably dealing with missed payments, recovery calls, or both. That is a hard place to be. This section explains what bank loan settlement actually means in plain words.

Bank loan settlement happens when your bank agrees to accept a lump sum that is less than what you still owe. The remaining balance is waived off. Your loan account is then marked "Settled" and the matter is considered resolved.

This is different from a normal loan closure. When you repay a loan in full, your account is marked "Closed." That is a clean record. Settlement is not the same thing. The "Settled" mark tells future banks that the lender did not get full repayment.

Settlement is generally considered when the bank believes full repayment may no longer be feasible. It only becomes an option after your loan has been marked as an NPA (loan gone bad, usually after 90 days of missed EMIs writer to verify against current RBI norms). At that point, the bank may assess that alternative resolution options need to be considered. Settlement is a way for both sides to resolve the matter.

Under RBI's compromise settlement guidelines, every bank must have a board-approved OTS policy. This means the process is not random. It is regulated. But whether your specific case is approved depends on the bank.

One important note: the "Settled" tag on your CIBIL report can stay for up to 7 years (writer to verify current duration against CIBIL's official FAQs). This is not a small thing. The CIBIL impact is real and long-lasting. That is why settlement must always be the last option after alternatives like EMI restructuring, moratorium, and tenure extension have been tried.

What Documents Do You Need for Bank Loan Settlement?

Content direction: Short, practical section. List the documents typically required. Explain why each matters in plain language. Cover: identity proof, address proof, income documents (or proof of income loss), 3–6 months bank statements, all existing loan account statements, hardship proof (termination letter, medical bills), any legal notices received. Mention that documents vary by bank — this is a general list. Honest note: being organised with paperwork improves the outcome of negotiations.

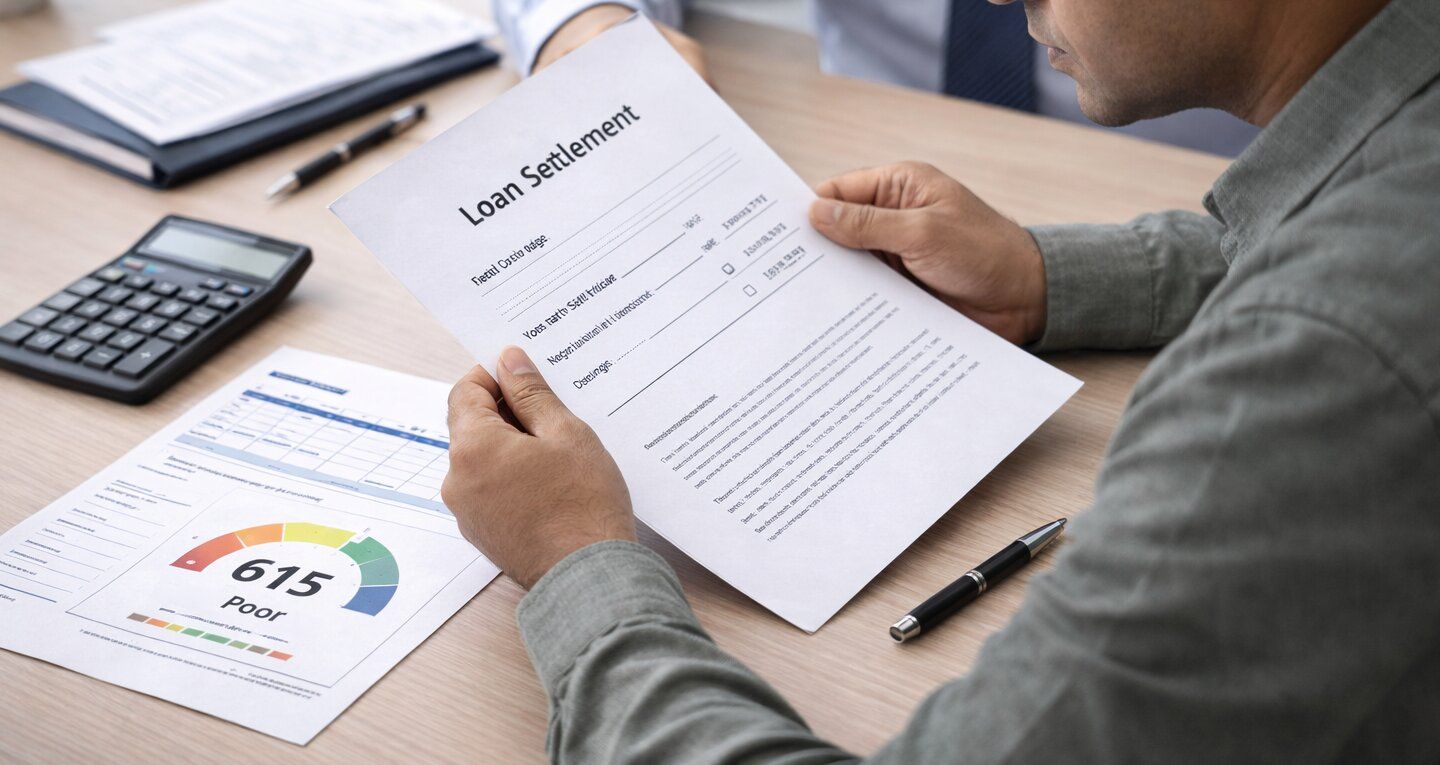

How Does Bank Loan Settlement Affect Your CIBIL Score?

Content direction: This is the most important consequence section — must be thorough and honest. Cover: "Settled" vs "Closed" status difference; "Settled" means the bank did not get full repayment, which is negative for future loan eligibility; the status stays on the CIBIL report for up to 7 years; future loan applications will likely be rejected or get poor rates during this period; the CIBIL score drop is significant (directional language only — do NOT quote specific point drops without a verified source); CIBIL score recovery is possible but takes 2–3 years of consistent positive credit behaviour after settlement. Frame this as information the reader needs to make an informed decision — not as a reason to feel ashamed.

Stats/data to include:

"Settled" tag stays up to 7 years — verified against CIBIL's official FAQs (writer to confirm)

12-month cooling-off period post-settlement before most regulated lenders consider new applications (reported in 2025 sources — writer to verify directly)

CIBIL updates typically happen 45–60 days after final payment (source: credsettle.com research — writer to cross-check)

What the Law Says box

Under the Negotiable Instruments Act Section 138, if you issued a post-datedcheque that bounced, the bank can file a criminal complaint. This is separate from the civil loan recovery process and can apply even during settlement negotiations.Placement:

How Does Bank Loan Settlement Affect Your CIBIL Score?What If the Bank Rejects Your Settlement Request?

Content direction: Address a real fear. Banks can and do reject OTS requests — settlement is their discretion, not the borrower's right. If rejected: the borrower can reapply after a period; can escalate to the bank's internal grievance cell; can approach the RBI Integrated Ombudsman if fair practices are violated. Also note: a rejection does not mean you have no options. Alternatives — restructuring, moratorium, tenure extension — remain on the table. FREED can negotiate on behalf of the borrower directly with the bank, which may improve the outcome. Keep tone calm and solution-focused.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

Want FREED to Negotiate Your Settlement Directly?

Free assessment. No pressure. We handle the paperwork and the bank.

Get My Free AssessmentShould You Approach the Bank Alone or Get Help?

Content direction: Honest assessment. A borrower can approach the bank directly — there is no legal requirement to use a third party. But banks negotiate with individuals less aggressively than with trained negotiators who know the OTS framework. FREED handles the entire settlement process FOR the reader — drafts the hardship letter, negotiates the amount, ensures written documentation, and confirms the NOC. Frame as: you have the right to do this yourself; FREED is available if you want help. Do NOT frame DIY as risky or dangerous — FREED blog rules prohibit DIY-bad framing.

What to Do After a Bank Loan Settlement Is Complete

Content direction: Positive, forward-looking section. Cover: collect NOC (clearance letter) from the bank and store it safely; check CIBIL within 60 days of payment to confirm "Settled" status appears; if it does not appear, raise a bureau dispute using the NOC as proof; begin rebuilding credit slowly — secured credit cards, small loans with timely repayment; do not take on new credit immediately; a 12-month disciplined track record can begin to lift the score. Frame this as the start of recovery, not the end of the story.

What Are the Bank Loan Settlement Rules in India?

Before you approach your bank, you need to know what the rules say not as legal theory, but as your actual rights.

1. Every bank must have a board-approved OTS policy. Under RBI's compromise settlement guidelines, banks cannot make up the rules as they go. Every bank has a formal, approved policy for handling settlement requests. The process is governed by a formal policy rather than individual discretion.

2. Settlement is the bank's discretion, not your right. You can request an OTS. The bank can say no. A rejection does not mean you have no options, but the bank has the final say.

3. Recovery agent contact hours: 8 AM to 7 PM only. Under the RBI Fair Practices Code (writer to verify exact circular), recovery agents are not allowed to contact you outside these hours. Calls before 8 AM or after 7 PM are a violation and can be reported.

4. No physical force, no threats, no abusive language. If calls turn threatening or abusive, that is a violation of RBI guidelines not just bad behaviour. You can report it.

5. Female borrowers may only be contacted by female recovery agents. This is a specific RBI protection that many borrowers are not aware of.

6. Banks must give written notice before appointing a recovery agent. Under RBI guidelines, borrowers are entitled to advance written notice before an agent is formally assigned to their account. The exact notice period depends on the applicable RBI circular. Check the RBI's website for the current requirement.

7. Any settlement offer must be given in writing. Never accept or pay based on a verbal promise. You have the right to a written offer letter from an authorised bank officer before any payment is made.

Each bank sets its own OTS terms within the RBI framework. The rules above apply to everyone. The settlement amount and process will vary by bank.

If you face a violation of any of these rights, you can approach the RBI Integrated Ombudsman at https://rbi.org.in/Scripts/Complaints.aspx.

What Actually Happens in the Bank Loan Settlement Process, Step by Step?

- Explore Every Alternative First Try EMI restructuring (changing your loan plan), moratorium (temporary pause on EMIs), or tenure extension before approaching for settlement. Settlement is only for when these options have genuinely failed.

- Collect job loss proof, medical bills, income documents, and all existing loan account statements. Being organised with your paperwork improves the outcome of any negotiation.

- Write a Formal Letter to Your Bank Send a written OTS request to your branch manager. Address it formally, explain your hardship, and ask for an OTS meeting. Do not rely on a phone call or WhatsApp message.

- Receive the Bank's OTS Offer in Writing The bank will come back with a written proposal the amount they are willing to accept. Never accept or pay anything based on a verbal promise from any bank official.

- Negotiate the Settlement Amount Settlement discussions may involve multiple rounds of communication. The final amount depends on your situation, your loan history, and the bank's internal policy. There is room to respond in writing.

- Get the Settlement Agreement Signed Before you transfer any money, a written settlement agreement must be signed by an authorised bank officer. Keep a copy of this.

- Make Payment and Collect Your NOC (Clearance Letter) After payment is made, request your No Dues Certificate (called NOC) from the bank in writing. Keep the payment proof and NOC together safely filed.

- Monitor Your CIBIL Report Credit bureau updates may take several weeks after settlement. If it does not update, raise a bureau dispute using your NOC as proof.

If you want help with any part of this, drafting the letter, handling the back-and-forth with the bank, or getting the settlement agreement worded correctly FREED can support you through this process.

FREED Expert Tip

Never make any payment to a bank for settlement without a signed written offer letter from an authorised bank officer. Verbal promises are not binding.

Enroll NowWhat Documents Do You Need for Bank Loan Settlement?

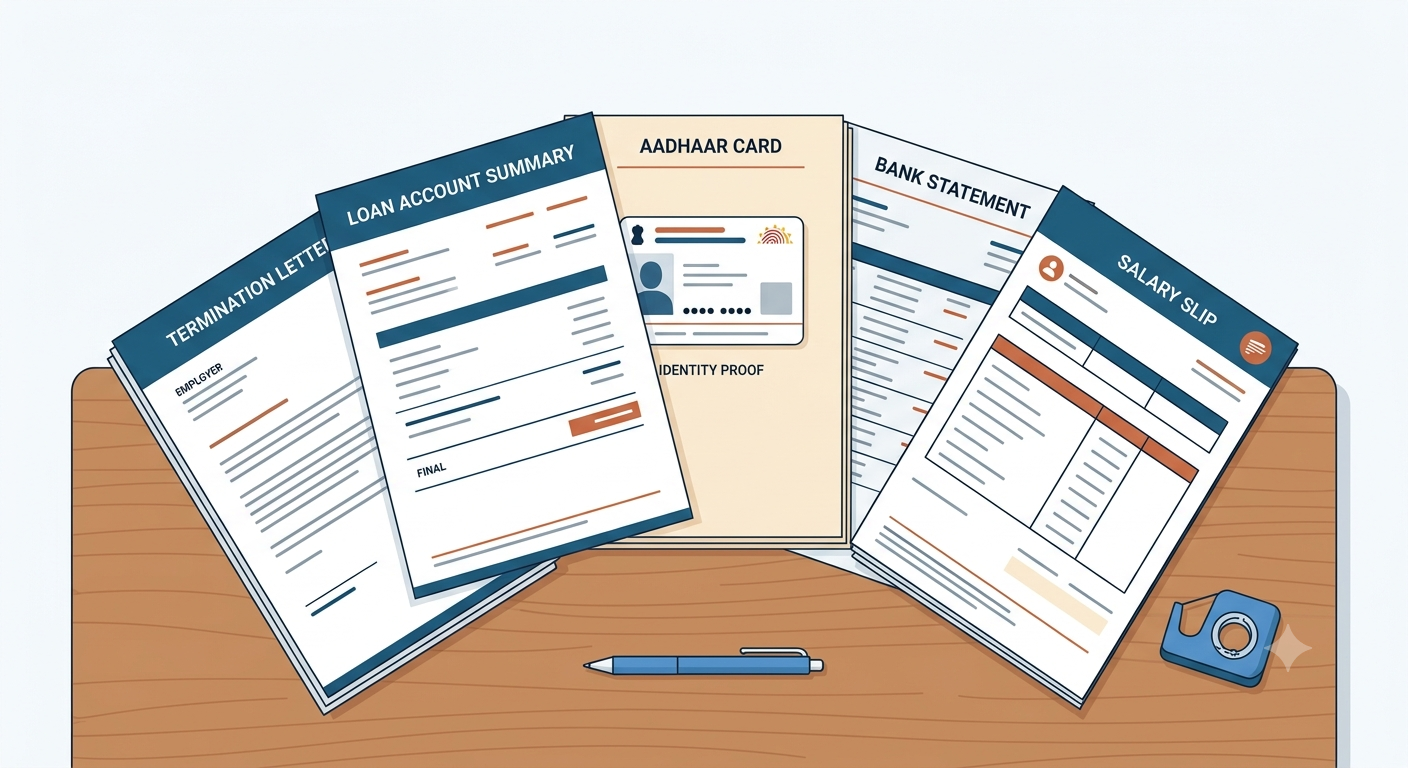

Having your documents ready before you approach the bank makes a real difference. Banks deal with many cases. A borrower who comes prepared is taken more seriously.

Here is the general list:

- Identity proof Aadhaar card, PAN card

- Address proof Aadhaar, passport, or utility bill

- Income documents salary slips, Form 16, or ITR for the last 1 to 2 years

- Proof of income loss or hardship termination letter, medical bills, or doctor's certificate

- 3 to 6 months of bank statements showing your current income and expenses

- All existing loan account statements principal outstanding, interest charged, penalties

- Any legal notices received from the bank or its representatives

This list will vary by bank. Some banks may ask for additional documents depending on the loan amount or type. Treat this as a starting checklist, not an exhaustive one.

One honest note: banks do not decide settlement amounts on the spot. Being organised with clean copies of all documents helps the process move forward without unnecessary back-and-forth.

India's leading debt resolution platform

FREED is India's leading platform for debt settlement and financial wellness. We have helped over 60,000 Indians reduce, manage, and get completely out of debt the right and legal way.

Media Mentions