Loan Settlement Process in Hindi: Bank Se Settlement Kaise Karein

Loan settlement process in Hindi mein samjhein bank se kaise baat karein, kya documents chahiye, CIBIL par kya asar hoga, aur FREED kaise madad karta hai.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

Loan settlement process mein bank ek kam raqam mein poora loan band kar deta hai lekin yeh sirf tab hota hai jab repayment genuinely impossible ho.

Settlement ke baad CIBIL report par "Settled" status up to 7 saal tak rehta hai aur score 75–100 points tak gir sakta hai.

Settlement karne se pehle EMI restructuring, tenure extension, ya moratorium jaisi options zaroor try karein yeh aapki CIBIL bachaa sakti hain.

Bina likha hua settlement letter ke koi bhi payment mat karein verbal ya WhatsApp se koi confirmation nahi chalta.

Settlement ke baad NOC (clearance letter NOC kehte hain isko) lena zaroori hai bina iske loan technically band nahi maana jaata.

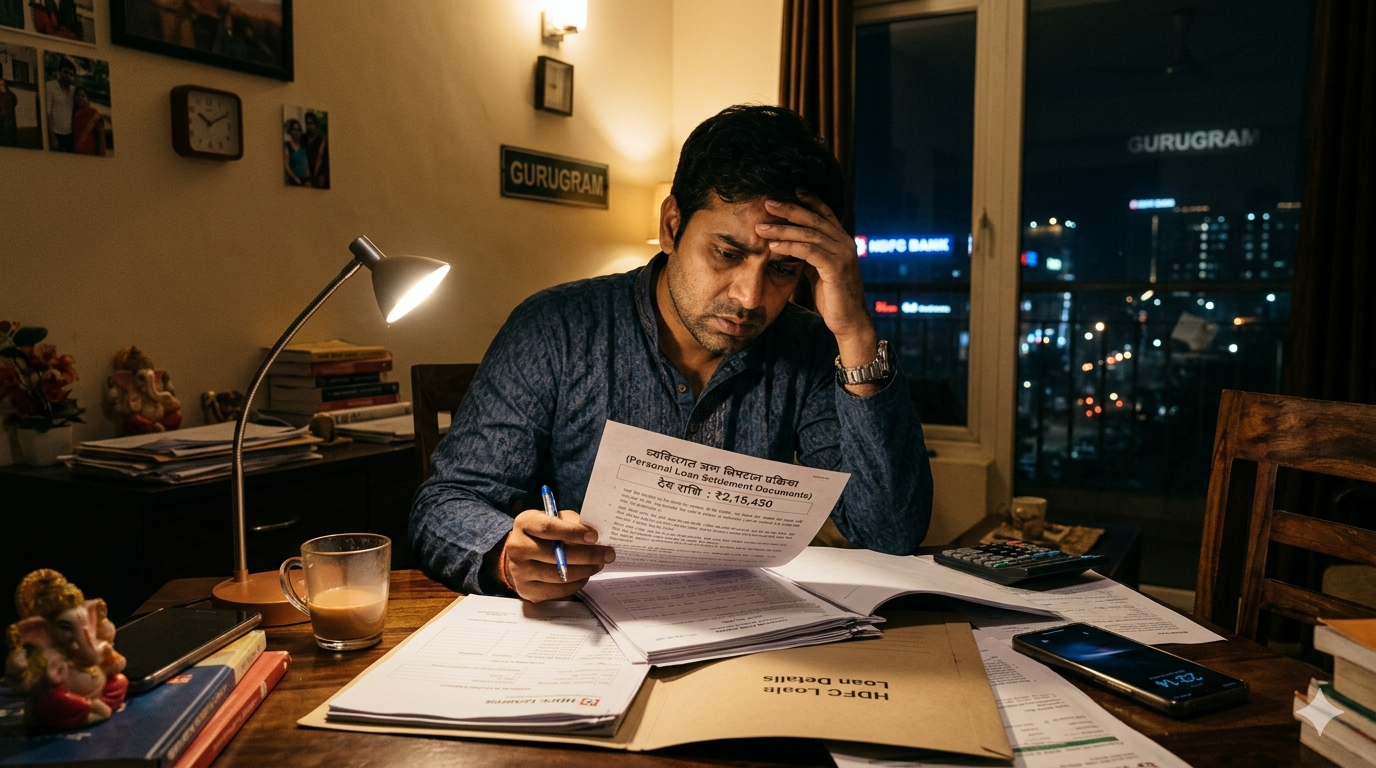

Loan Settlement Kya Hota Hai?

Content direction: Expand the Definition Box naturally. Explain what loan settlement means in plain Hinglish — that the bank agrees to accept a lower amount as full and final payment, writes off the rest, and closes the account. Immediately and clearly distinguish "settled" from "closed" — if a loan is fully repaid, it shows "Closed" on CIBIL; if settled for less, it shows "Settled," which future banks see as a red flag. Use a simple ₹ example to make this tangible — e.g., if someone owes ₹1,00,000 and the bank agrees to accept ₹60,000, the remaining ₹40,000 is waived. But the CIBIL record will show this. Open this section with the mandatory line: "Settlement is not something a borrower chooses out of preference" — adapted naturally into Hinglish. Banks only consider it when the borrower has genuine inability to pay. Establish this clearly in the first paragraph.

Bank Loan Settlement Kab Consider Karna Chahiye?

Content direction: This section addresses the core question: when is settlement actually appropriate? The answer must be clear only when repayment in full is genuinely not possible due to a real financial difficulty: job loss, medical crisis, income gone down drastically, family emergency. Writer must NOT list "too many loans" or "feeling stressed" as triggers these are not valid. Settlement trigger genuine inability to pay. List real situations that qualify, without shame or blame. Acknowledge that reaching this point is hard the reader didn't choose this. Also briefly introduce the alternatives that should be explored first this section serves as a bridge into H2 3. Tone: empathetic, calm, blame-free.

Settlement Se Pehle Yeh Options Zaroor Try Karein

Content direction: FREED's most important brand rule — alternatives before settlement. Cover 4 options in plain Hinglish with a one-to-two line explanation each:

Option 1: EMI Restructuring — bank se baat karke EMI ki raqam kam karwana ya repayment plan badalna. Option 2: Tenure Extension — loan ki time period badhwana taaki monthly EMI chhoti ho jaye. Option 3: Moratorium (temporary pause) — kuch mahine ke liye EMI band karne ki request, jab aai wapas normal ho jaaye. Option 4: Loan Consolidation — agar kai saare loans hain, unhe ek loan mein merge karna taaki ek hi EMI deni pade.

For each option: one sentence of what it is, one sentence of when it makes sense. Keep this motivating — these options preserve the CIBIL score. End with: "Agar inn mein se koi bhi option kaam nahi kar raha aur poora repayment genuinely impossible lag raha hai, tab loan settlement ki baat karna sahi ho sakta hai." Do NOT frame settlement as a natural next step — frame it as the last option when all others are genuinely exhausted.

EXPERT TIP

Tip: Bank se settlement ki baat karne se pehle apni last 3 month ki bank statements, loan statement, aur hardship ka proof (job loss letter ya medical bills) ready kar lein. Isse aapki baat zyada seriously li jaayegi. Settlement Se Pehle Yeh Options Zaroor Try Karein.

freed.care/resources/documents-needed-for-loan-settlementLoan Settlement Process Step by Step — Bank Se Kaise Karein?

Content direction: This is the primary content section matching the primary keyword. General method framed clearly — the reader can follow this themselves. FREED mentioned only at the end of the last step as available help. Steps must follow the STEP SECTION rule: 1 bold heading line + 1 short sub-line MAX per step. No paragraphs, no examples, no extra context inside the step body. See Steps Section below.

- 1

Step 1

Apna Poora Loan Samjhein Apni loan statement lein — total outstanding, interest, aur penalty charges clearly likhein.

- 2

Step 2

Hardship Ka Proof Ikatha Karein Job loss letter, medical bills, ya income drop ka koi bhi written proof collect karein.

- 3

Step 3

Bank Ki Recovery Team Se Milein Customer care nahi — directly bank ki recovery ya collections team se sampark karein aur apni situation explain karein.

- 4

Step 4

Written Mein Settlement Request Dein Apni request aur hardship documents ke saath likha hua proposal dein — kitna amount aap de sakte hain, yeh clearly bataayein.

- 5

Step 5

Negotiate Karein, Jaldi Commit Mat Karein Bank pehli baar mein zyada maang sakta hai. Shant rehein. Sirf wahi amount commit karein jo aap actually de sakte hain.

- 6

Step 6

Settlement Letter Milne Ke Baad Hi Payment Karein Koi bhi payment karne se pehle bank se official settlement letter lein — letterhead par, likhit mein. Iske baad hi payment karein. Agar aapko is poore process mein madad chahiye, FREED ke counsellors aapki taraf se bank se baat kar sakte hain.

Nahi Pata Kahan Se Shuru Karein?

Hum Batayein. Subtext: Free call. Koi pressure nahi. Aapki situation ke liye seedha raasta.

Apna Free Assessment LeinLoan Settlement Mein Kaun Se Documents Chahiye?

Plain, practical checklist section. List the documents a borrower needs to initiate settlement discussions with a bank. Explain each in one short line. Documents to cover: (1) Loan account statement — total outstanding ka full breakup; (2) Hardship proof — job loss letter, medical bills, ya bank statements showing income loss; (3) Income proof — salary slip ya aur koi income document jo current financial situation dikhaye; (4) ID proof — Aadhaar ya PAN; (5) Any written communication from the bank — recovery notices or NPA letters if received. End with a strong reminder: settlement letter ke bina koi payment mat karein, aur payment ke baad NOC (clearance letter) zaroor maangein. Tone: practical, calm, step-by-step. No jargon without explanation.

Loan Settlement Ka CIBIL Score Par Kya Asar Hota Hai?

Content direction: Honest, clear, empathetic. This is one of the most searched secondary questions and most competitors underplay it. Cover: (a) What "Settled" status looks like on a CIBIL report and how it differs from "Closed"; (b) How long it stays — up to 7 years; (c) The score drop. Do NOT sugarcoat this — Ramesh needs to understand the cost before deciding. Then acknowledge: agar poori repayment genuinely impossible hai, toh bhi yeh option exist karta hai — but the cost is real and worth understanding. Briefly mention CIBIL recovery path after settlement — consistent payments on other accounts, low credit card usage over time. One mention of FREED's CIBIL repair guidance as available post-settlement support.

Loan Settlement Ka CIBIL Score Par Kya Asar Hota Hai?

WHAT THE LAW SAYS

Law: RBI ke guidelines ke mutabiq koi bhi bank ya NBFC aapko threaten ya harass nahi kar sakta — settlement ke dauran bhi. Recovery agents ka aapke family members ya employer se baat karna bina aapki permission ke allowed nahi hai. Placement: After H2 6 — Loan Settlement Ka CIBIL Score Par Kya Asar Hota Hai?

freed.care/resources/recovery-agent-harassment-rightsAre You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

Loan Settlement Ke Baad Kya Karein?

Content direction: Post-settlement action steps — practical and forward-looking. Cover: (1) Settlement letter safe rakhein — yeh aapka proof hai ki loan officially settle ho gaya; (2) NOC (clearance letter) lein — bank se likhit mein confirm karein ki koi outstanding nahi hai; (3) CIBIL report check karein — verify karein ki status "Settled" dikha raha hai, koi worse status nahi (jaise "Write-off" ya "Suit Filed"); (4) Agar CIBIL report mein kuch galat dikh raha hai, toh CIBIL dispute raise karein; (5) Dheere dheere CIBIL repair shuru karein — doosre loans ya EMIs samay par bharein, credit card ka balance zyada mat badhne dein. Tone: hopeful, forward-looking, practical. Do NOT promise any specific CIBIL recovery timeline — it varies per individual.

IN-BODY CTA 2

FREED Se Baat Karein — Bilkul Free Subtext: Ek call. Koi judgment nahi. Seedha aur sach mein helpful.

Apni Free Call Book KareinLoan Settlement vs Doosre Options Aapke Liye Kya Sahi Hai?

Option | Kab Kaam Aata Hai | CIBIL Par Asar | Naya Loan Lena Padega? |

EMI Restructuring | Aap abhi bhi kuch pay kar sakte hain par poori EMI heavy lag rahi hai | Minimal agar sahi time par kiya | Nahi |

Tenure Extension | Monthly EMI chhoti karni hai | Minimal | Nahi |

Moratorium (Temporary Pause) | Short time ke liye income band ho gayi | Minimal | Nahi |

Loan Consolidation | Kai saare loans hain, ek mein merge karna chahte hain | Minimal | Haan, ek naya loan |

Loan Settlement | Poori repayment genuinely impossible hai | Significant "Settled" status up to 7 saal | Nahi |

Note: Yeh table sirf samjhaane ke liye hai. Aapke case mein kya sahi hai yeh aapki exact situation par depend karta hai. FREED koi lender nahi hai aur koi specific outcome guarantee nahi karta. Apni situation ke liye ek free counselling call zaroor karein.

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions