Personal Loan Settlement Percentage: What Is Typical in India

Personal loan settlement percentage is the share of your total outstanding loan that a bank or NBFC (non-bank loan company) agrees to accept as full and final payment instead of the complete amount you owe. There is no fixed percentage set by law. The final number depends on your specific situation, your loan's history, and how long repayment has been missed.

FREED India

Reviewed by FREED India, SEO Intern

Key Takeaways

Personal loan settlement percentage is not fixed; it varies case by case, based on your financial situation and loan history.

Banks generally consider settlement only after a loan has been overdue for 90 days or more, and often after 6+ months of missed EMIs.

The "Settled" mark on your CIBIL report can stay for up to 7 years and may drop your score by 75-100 points.

Settlement must be considered as a last resort. It’s always better to explore options such as EMI restructuring, tenure extension, or moratorium first.

FREED works with banks and NBFCs to help you find the most manageable path, whether that is settlement or an alternative.

What Is a Personal Loan Settlement Percentage?

Settlement is not something a borrower chooses out of preference. Banks and NBFCs only consider it when you are in genuine financial difficulty and are truly unable to repay the full amount. It is a last resort, not a shortcut.

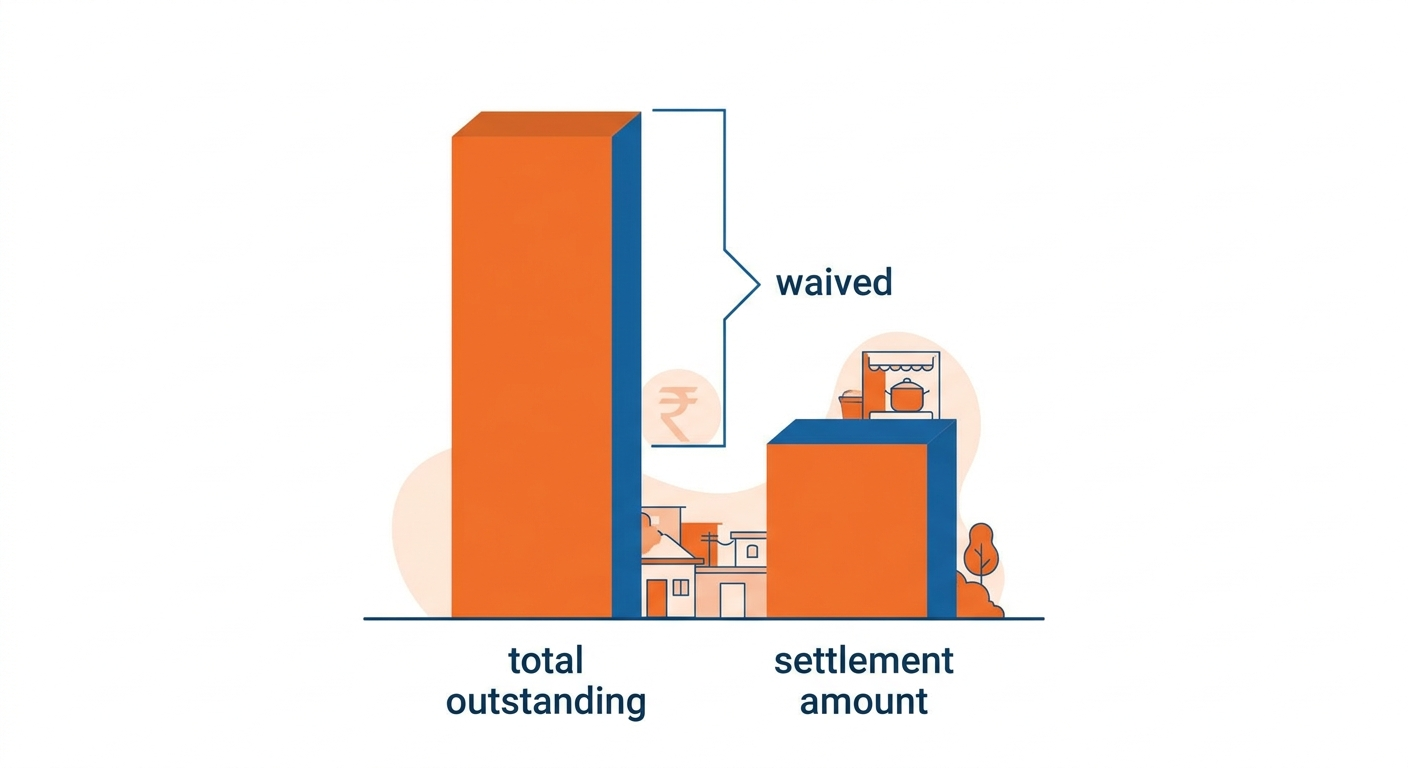

When a bank "settles" a personal loan, it agrees to accept less than what you actually owe. The personal loan settlement percentage is simply how much of the outstanding amount you end up paying.

Here is a plain example. Say you owe ₹1,00,000 on a personal loan. The bank agrees to accept ₹50,000 as full and final payment. That means the settlement happened at 50% of the outstanding amount. The remaining ₹50,000 is waived.

But this number is never guaranteed. There is no law in India that sets a minimum or maximum settlement percentage. Every case is handled individually.

There is also a critical difference between settlement and a normal loan closure. When you repay a loan in full, your CIBIL report shows the status as "Closed." That is clean. When a loan is settled for less than what you owe, the report shows "Settled." That is different from a fully repaid loan, and future lenders may consider that distinction during evaluation.

Per RBI guidelines, a loan is classified as NPA (loan marked as bad by the bank) after 90 days of missed EMI. Most banks do not open settlement discussions until the loan has been in this category for a significant period typically 6 or more months of non-payment.

Why Is There No Fixed Settlement Percentage?

This is the most common frustration. It is natural to want a clear number. But banks assess each situation individually.

No law, no RBI circular, and no industry standard sets a settlement floor or ceiling for personal loans. Each bank makes this call internally. Their decision is based entirely on your specific case, and not a decided formula.

RBI circular DOR.STR.REC.80/21.04.048/2023-24 (issued June 2023) provides guidance to banks on compromise settlement for borrowers in genuine financial difficulty. But it gives banks the discretion to decide it does not fix a percentage. (Writer to fetch and verify the exact language of this circular before publishing.)

What this means for you: If you see articles quoting broad settlement ranges online, treat them as general examples, not guarantees, not a promise. The actual number depends on factors specific to your case.

That is an honest answer. And it is the one FREED stands by.

What Factors Actually Affect the Settlement Amount?

These five factors have the most influence on what a bank is willing to accept:

1. How long the loan has been overdue: Banks are generally more open to discussion when a loan has been overdue for a longer period. A loan that has been NPA for 18 months is treated differently from one that missed its first EMI last month.

2. Proof of genuine hardship: Documents such as a job loss letter, medical bills, or 3 months of bank statements showing income loss can help banks to validate a waiver. However, without solid documentation, banks don’t have enough evidence to provide a relaxation in the overdue amount.

3. The bank or NBFC's internal policy: Public sector banks (government banks) and private banks handle settlement differently. NBFCs may have different processes again. There is no uniform rule.

4. The outstanding amount at the time of negotiation: This includes the original unpaid principal, added interest, and penalty charges. The number you negotiate from may be higher than what you originally borrowed.

5. Whether you can pay the settled amount as a lump sum: Banks strongly prefer a single payment over instalments. If you can arrange the full settled amount at once, that is a stronger position to negotiate from.

FREED Expert Tip

Before asking about settlement, collect 3 documents: your loan statement, proof of hardship (job loss letter or medical bills), and your last 3 months' bank statements. These make your case believable.

See what documents you need for loan settlementWhat Does Settlement Do to Your CIBIL Score?

When a loan is settled, your CIBIL report is updated with the status "Settled." This is different from "Closed," which is what shows up when you repay in full. Lenders who check your report in the future can see this status clearly and many treat it as a red flag.

The score impact is also significant. A settled loan may significantly affect your CIBIL score depending on your broader credit history.

The impact varies from person to person depending on overall repayment history and existing credit behaviour. That makes it harder to get a new loan, a credit card, or sometimes even a rental agreement.

This is not shared to discourage you. It is shared because you need to know the cost before you decide.

If there is any realistic way to repay in full through a payment plan, a moratorium, EMI restructuring, or support from family, exploring that first is the better path. But for some borrowers, when repaying in full becomes genuinely impossible, settlement may be the most realistic option available. Understanding both the benefits and trade-offs helps you make a more informed decision.

What Are Your Options Before Settlement?

Before settlement becomes the conversation, four options are worth exploring seriously. These options are generally considered before settlement because they may have a lower impact on your credit profile..

EMI Restructuring: You ask the bank to change your repayment plan reducing the monthly EMI amount or adjusting when payments are due. This is different from missing EMIs. It is a formal request to change the terms.

Tenure Extension: You ask the bank to stretch your loan period, say, from 36 months remaining to 60 months. Your monthly EMI drops. Total interest paid over time increases, but the immediate pressure reduces.

Moratorium (temporary payment break): A moratorium is a short, approved pause on repayments. You stop paying for a fixed period. Interest usually continues to accrue. This is useful if the difficulty is temporary, there’s a medical event, or a short income gap.

Debt Consolidation: If you have multiple loans, consolidation means merging them into one new loan with a single, lower EMI. This can reduce the total monthly burden and simplify your payments. It does require qualifying for the new loan.

If none of these options work and repaying in full is genuinely not possible, that is when settlement becomes a conversation worth having.

How Does the Personal Loan Settlement Process Work?

Settlement is not something a borrower chooses out of preference. Banks and NBFCs only consider it when you are in genuine financial difficulty and truly unable to repay the full amount. It is a last resort, not a shortcut.

Here is how the process works, step by step.

- 1

Step 1 Understand What You Owe:

Review your loan statement carefully total outstanding, added interest, and any penalty charges.

- 2

Step 2 Document Your Hardship

Gather proof of financial difficulty, job loss papers, medical bills, or bank statements showing income loss.

- 3

Step 3 Contact the Right Team

Reach the loan recovery or collections department, not general customer service to discuss your situation.

- 4

Step 4 Make a Written Proposal

Submit your proposal in writing with your hardship documents and the amount you can realistically pay as a lump sum.

- 5

Step 5 Negotiate Patiently

The bank may respond with a different proposed amount based on your case. Stay calm, stick to what you can genuinely pay, and do not commit to an amount you cannot arrange.

- 6

Step 6 Get Everything in Writing

Once an amount is agreed, ask for an official settlement letter on the bank's letterhead before making any payment. If you want help with any of these steps, FREED's counsellors can help guide and support you through the process.

What Happens After Settlement and How to Recover

The process does not end when the bank accepts your payment. There are two things to do immediately after.

Get the NOC (clearance letter) from the bank. A No Objection Certificate or NOC (clearance letter) is your proof that the bank has no remaining claim on the loan. Ask for this on the bank's official letterhead, and keep it permanently.

Verify your CIBIL report is updated correctly. Check that the status shows "Settled" not "Written Off" or a worse classification. If the update is incorrect, raise a dispute through the CIBIL portal. Banks are expected to update credit bureau records accurately based on RBI and bureau reporting norms..

After that, recovery is a slower process. There is no fixed timeline. It depends on how many active accounts you have, how consistently you repay, and how much of your credit limit you use.

What helps over time: paying all other EMIs on time, keeping your credit card balance below 30% of the limit, and avoiding applying for new credit repeatedly in a short window.

FREED also offers guidance to help borrowers rebuild healthy credit behaviour after settlement for borrowers who want structured guidance on rebuilding their score.

What the Law Says:

Under RBI guidelines, banks must provide a written settlement letter before you pay. Never pay on a verbal promise or a WhatsApp message alone.

Know your rights under RBI recovery rulesSettlement vs Other Options What Suits Your Situation

About FREED

FREED is India's first debt relief company. Founded in 2020, FREED helps people with unsecured loans credit cards, personal loans, BNPL, and loan apps negotiate settlements with banks and NBFCs. FREED charges fees only when a settlement is successfully reached. FREED does not handle secured loans such as home loans, car loans, or gold loans.

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions