Bank Loan Settlement Process in India: A Complete Guide

Struggling to repay a bank loan and wondering if settlement is an option? It is but the process has specific steps, and skipping any one of them can leave you unprotected. Here is exactly how it works.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

Bank loan settlement is a legal, formal agreement where you pay less than the full outstanding amount and the bank agrees to close the account and waive the remaining balance.

Banks agree to settle only when you can genuinely prove financial hardship and they believe settlement is better than prolonged recovery that may yield nothing.

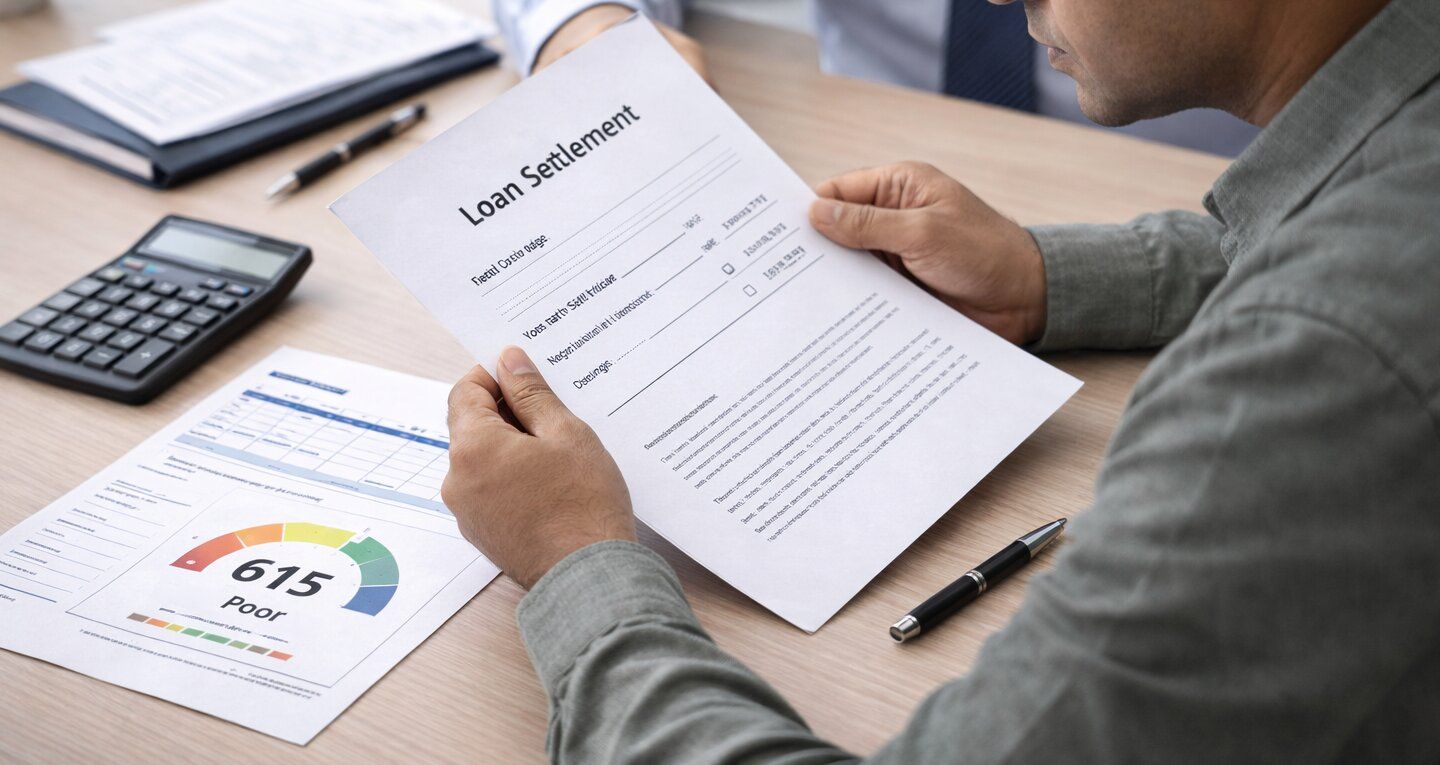

Never pay any settlement amount without a written settlement letter from the bank first. A verbal agreement has no legal standing.

After paying, always collect a No Dues Certificate from the bank. This is your permanent legal proof that the debt is resolved.

Settlement does affect your CIBIL score your report shows Settled instead of Closed. But it stops the continuous damage from an ongoing default and gives you a clear starting point for recovery.

What is Bank Loan Settlement?

Bank loan settlement is a formal agreement between you and your lender.

You owe a certain outstanding amount on a loan. You genuinely cannot repay the full amount. You approach the bank, explain your situation with documentation, and negotiate. The bank reviews your case and if it believes you truly cannot repay in full agrees to accept a reduced lump sum to close the account. The remaining balance is waived off.

This is called a One-Time Settlement or OTS.

For example: You owe Rs 3,00,000 on a personal loan. You have missed payments for 4 months due to job loss. The bank, after reviewing your situation and documentation, agrees to settle for Rs 1,60,000. You pay Rs 1,60,000. The loan is officially closed. The remaining Rs 1,40,000 is waived.

Bank loan settlement is completely legal in India. It is a mutually agreed arrangement under Indian contract law. Both parties you and the bank must follow through on every term of the agreement.

It is not a shortcut. It is not a way to avoid debt you can afford to repay. It is a formal resolution mechanism for genuine hardship situations and it carries consequences that must be understood before proceeding.

Who is Eligible for Loan Settlement in India?

Banks do not offer settlement to everyone. They have clear internal criteria.

You are more likely to be considered for settlement if:

You have missed loan payments for 90 days or more at which point your account is classified as an NPA or Non-Performing Asset.

You have a documented, genuine reason for the financial hardship of job loss with a termination letter, a medical emergency with hospital bills, a significant income reduction shown through salary slips, or a business failure reflected in bank statements.

You can demonstrate that you cannot repay the full outstanding amount even over an extended period.

You have a realistic lump sum available to offer either from savings, from family support, or from a structured savings plan.

Banks are significantly more open to settlement when they believe the alternative is getting nothing through a prolonged legal recovery process. Your documented hardship is what convinces them that settlement is the better outcome for both parties.

If you have recently started missing payments and can genuinely afford to repay with some restructuring EMI reduction or tenure extension that is a better path than settlement, both for your CIBIL score and for your long-term financial health.

How Settlement is Different From Loan Closure

This distinction matters both practically and for your credit report.

A normal loan closure happens when you repay every rupee as per the original agreement. Your credit report shows Closed. Future lenders see a fully honoured commitment. No negative impact.

A settlement happens when you pay less than the full outstanding and the bank agrees to close the account. Your credit report shows Settled. Future lenders see that the full commitment was not met. This carries a negative impact on your CIBIL score.

Status | What It Means | Credit Report Impact |

Closed | Full amount repaid as agreed | Positive — no negative impact |

Settled | Reduced amount accepted by bank | Negative score drops, stays 7 years |

Written Off | Bank gave up recovering debt still exists | Severe much worse than Settled |

Default or NPA | Ongoing non-payment unresolved | Continuous damage score keeps falling |

Settled is significantly better than Written Off or an ongoing default. But it is not as clean as Closed. Understanding this difference helps you make an informed decision about whether settlement is the right path for your situation.

The Bank Loan Settlement Process: Step by Step

The process has six clear stages. Each one matters.

- 1

Stage 1: Assess Your Situation Honestly

Before approaching any bank, be completely clear about your own financial picture. Write down: total outstanding on the loan including accumulated interest and penalties, your current monthly income from all sources, your monthly essential expenses, any savings or assets you have, and what realistic lump sum you could offer as a settlement. This assessment tells you two things. First, whether

- 2

Stage 2: Contact the Bank's Settlement or Collections Department

Call your bank's customer care and ask to speak specifically to the settlements department or the collections team not general customer service. When you speak to them, be honest and direct. Tell them you are experiencing financial hardship and cannot repay the full outstanding. Tell them you want to discuss a one-time settlement. Ask what documentation they need and what

- 3

Stage 3: Gather and Submit Documentation

This stage directly determines the quality of your settlement outcome. A well-documented hardship case gets a better response and a lower settlement amount than a poorly documented one. Gather whatever is relevant to your specific hardship situation. The documents section below provides a complete list. Submit everything the bank asks for and submit it completely the first time. Incomplete submissions

- 4

Stage 4: Negotiate the Settlement Amount

The bank will make an initial offer. This is almost never their best offer. There is room to negotiate. Banks typically settle for 40 to 70% of the total outstanding in genuine hardship cases. Where exactly within that range you land depends on the quality of your documentation, how long the account has been in NPA, whether you can offer

- 5

Stage 5: Get the Settlement Agreement in Writing

This is the most critical stage and the one where the most borrowers make costly mistakes. Do not pay a single rupee without a formal, written settlement letter from the bank on official letterhead. This letter must clearly state specific terms as listed in the section below. Read every line. If anything is ambiguous or absent, ask the bank to

- 6

Stage 6: Make the Payment and Collect Your Documents

Pay the agreed amount exactly as specified in the settlement letter on time, through the agreed channel, in the correct amount. Do not pay early through an unauthorised channel. Do not pay in parts unless the letter explicitly allows this. Follow the terms exactly. A missed deadline can allow the bank to revoke the offer. After payment, collect two documents:

What Documents You Need

Have these ready before you approach the bank. Missing any one of them can delay the process by weeks.

Proof of financial hardship job termination letter, hospital bills and medical reports, salary slips showing income reduction, ITR showing reduced income for self-employed borrowers.

Bank statements for the last 6 months showing actual account balances and transaction patterns.

The original loan agreement and account statement showing total outstanding.

PAN card and Aadhaar card for identity verification.

Any previous correspondence with the bank letters, emails, notices related to the loan.

If you are going through FREED, we help you compile and organise all of this documentation in the most persuasive format which directly affects the settlement outcome.

After Settlement | What Happens Next

Once you have paid and received your No Dues Certificate, three things happen.

The loan account is officially closed. No more EMIs. No more interest. No more collection calls on this account. The debt is legally resolved.

Your credit report is updated. Within 30 to 60 days, the account status changes from NPA or Overdue to Settled. This is better but it is not the same as Closed. The Settled status stays on your credit report for up to 7 years.

Your CIBIL score is affected. Settlement causes a score drop typically 75 to 100 points or more depending on your starting score. But if your account was already in default, your score was already falling every month. Settlement stops that continuous decline. It fixes the damage at one point. Recovery can begin.

With consistent, responsible financial behaviour after settlement paying all current obligations on time, keeping credit utilisation low most people see meaningful score improvement within 12 to 24 months.

The Settlement Letter: What It Must Contain

Before paying, verify that the settlement letter from the bank includes every one of these elements:

Your full name as it appears on the loan agreement.

The loan account number.

The original outstanding amount at the time of settlement initiation.

The agreed settlement amount.

The payment deadline and the specific payment method.

A clear, unambiguous statement that once the settlement amount is paid, you have no further financial liability on this account.

A statement that the account will be closed and marked as Settled in the bank's records and with credit bureaus.

If any of these elements are absent, ask the bank to add them before you pay. A settlement letter missing any of these points does not give you the full legal protection you need.

How Settlement Affects Your CIBIL Score

This deserves its own clear section because it is the most common concern and the most misunderstood.

Settlement does damage your CIBIL score. The word Settled on your credit report tells future lenders that you did not repay the full amount you committed to. This is a negative mark.

However, there are two important points of context.

First, if your loan is already in NPA or default, your score is already being damaged every single month. Every 30 days of unresolved default adds more negative marks. Settlement stops this ongoing damage. It draws a line.

Second, the Settled status is not permanent. Its impact weakens every year as you build a fresh record of responsible financial behaviour. By year 2 to 3 after settlement, most lenders focus primarily on your recent behaviour rather than the old mark. By year 7, the entry is removed from your report entirely.

The comparison that matters: an unresolved default that continues for years versus a settled account followed by 24 months of clean behaviour. The settled account recovers. The unresolved default does not.

Common Mistakes to Avoid

Paying any amount without a written settlement letter is the most dangerous mistake. Verbal promises are not enforceable.

Missing the payment deadline after the settlement is agreed the bank can revoke the offer.

Not collecting the No Dues Certificate after payment without it, you have no proof the debt is resolved.

Negotiating alone without understanding what the bank is likely to accept results in settling for more than necessary.

Not reading every line of the settlement letter ambiguous clauses can create problems later.

Assuming settlement means the debt disappears from your credit report it does not. It shows as Settled for up to 7 years.

How FREED Manages the Entire Loan Settlement Process for You

Negotiating a bank loan settlement alone is stressful, time-consuming, and usually less effective than working with a professional.

Banks have experienced recovery teams. Most borrowers are doing this for the first time. That is a significant disadvantage when it comes to negotiating the settlement amount and reviewing the legal terms.

FREED levels this completely.

We assess your full debt situation and confirm whether settlement is the right path or whether consolidation or restructuring would serve you better.

We compile and present your hardship documentation in the most effective format which directly improves the settlement outcome.

We negotiate with your lenders on your behalf. Our counsellors deal with banks every day and know what each lender will realistically accept. We push for the maximum possible reduction. On average, FREED clients settle at 56% less than the original outstanding.

We review every settlement letter before you pay a single rupee checking every clause to ensure your legal interests are fully protected.

We handle all creditor communication through your relationship manager throughout the process.

We protect you from harassment through FREED Shield the moment any recovery agent crosses a legal line, we escalate formally.

You do not have to face the bank alone. FREED has done this for over 10,000 Indians and we will do it for you.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions