Axis Bank Debt Consolidation Loan: Eligibility, Process, and What to Do If You Don't Qualify

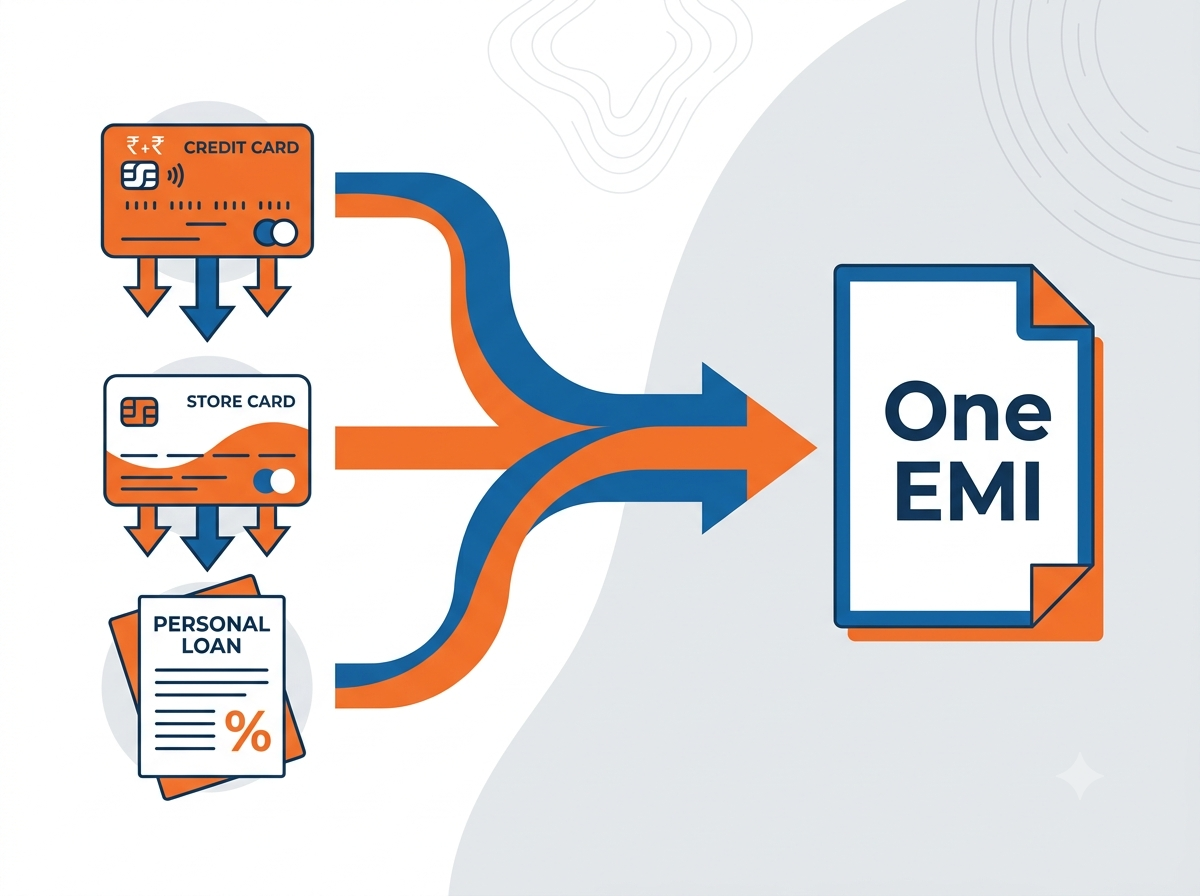

An Axis Bank debt consolidation loan is a personal loan from Axis Bank that you use to pay off multiple existing debts, including credit card dues, personal loans, or loan app balances, and replace them with one single EMI at a lower interest rate. Axis Bank doesn't actually offer a product called "debt consolidation loan." Their personal loan is what's used for this purpose, if you qualify.

FREED India

Reviewed by FREED India, SEO Intern

Key summury

There are two real ways to consolidate: apply to Axis Bank yourself, or let FREED's Loan Consolidation Program match you to a lending partner and handle the process for you. This guide covers both.

An Axis Bank debt consolidation loan works through their personal loan product which is the vehicle.

Axis Bank personal loan rates currently start around 9.99% to 10.5% per annum, compared to credit card interest of up to 36% per annum. The savings can be significant.

A CIBIL score of 750 gives you the best approval odds. If your score has already dropped from missed EMIs, your odds drop sharply too.

Loan amounts run ₹50,000 to ₹40 lakh, tenure 12 to 84 months, with a processing fee typically around 1.5% to 2% of the loan amount plus GST.

If you don't qualify for consolidation, then settlement may be the structured way through, but these are very different paths with very different outcomes.

What Is an Axis Bank Debt Consolidation Loan, and How Does It Work?

Axis Bank doesn't have a product literally called a "debt consolidation loan." What people use for this purpose is their standard personal loan, and for the right borrower, it genuinely works.

Here's the mechanic: you take a personal loan from Axis Bank, use the funds to immediately clear your existing high-interest debts (credit cards charging up to 36% a year, loan apps often at 22% or more, or other personal loans), and you're left with one EMI, to Axis Bank, at a meaningfully lower rate.

Axis Finance, Axis Bank's NBFC (non-bank financial company) arm, is worth knowing about separately. It specifically advertises taking over multiple loans, including loan app balances, as a balance transfer, consolidated under one umbrella. Its eligibility bar runs a bit lower than the main bank's.

None of this is automatic, and none of it is free money. The interest savings are real for someone with a stable income and a clean repayment history. But it only works if you still qualify, meaning a reasonably healthy CIBIL score and steady income. If either of those has slipped, the next section matters more than this one.

Who Is This For, and Who Should Not Apply?

This is the part most articles on this topic skip, and it matters more than the eligibility checklist that follows.

If your CIBIL score is 750 or above, your total EMIs are over 50% of your take-home salary, and you're paying everything on time but just tired of juggling multiple due dates, a consolidation loan is genuinely a good fit. You're the borrower this product was built for.

If you've already missed EMIs, your CIBIL score has dropped, your FOIR (Fixed Obligation to Income Ratio, how much of your salary already goes toward EMIs) is above 50%, or your income has become irregular or stopped, this is harder to hear: a consolidation loan is unlikely to work for you right now.

Here's why this matters beyond disappointment. Every loan application creates a hard inquiry (a formal credit check), and that alone drops your CIBIL score by roughly 5 to 10 points. Apply and get rejected, and you've made your score worse for no benefit. If your score has already fallen below 680 from late payments, an unsecured consolidation loan from most banks is genuinely unlikely. That's not a judgment on you. It just means the section further down, on what to do instead, is where you should actually be looking.

One more path worth knowing before you apply anywhere: if you fit the "good fit" description above but would rather not handle the bank-by-bank legwork yourself, FREED's Debt Consolidation Program does this matching for you. FREED looks at your full profile, all your loans, your income, your EMIs, and matches you to a lending partner from its own huge network of lenders that disburses one consolidated loan to pay off your existing unsecured debts. It's built specifically for borrowers who are still current on payments but stretched across too many EMIs, and it doesn't hurt your CIBIL score; it typically starts improving once you're down to one regular payment. There's no upfront fee, FREED is paid only if the consolidation actually goes through.

FREED Expert Tip

Before applying to Axis Bank, calculate your FOIR: add up all your monthly EMIs and divide by your take-home salary.

FREED's Debt Consolidation ProgramWhat Are the Eligibility Criteria for Axis Bank Debt Consolidation?

Here's the checklist, salaried and self-employed both covered.

For salaried applicants: age 21 to 60 years, a minimum monthly income of ₹15,000 if you're an existing Axis Bank customer or ₹25,000 if you're new to the bank, at least 6 months in your current job and 2 to 3 years of total work experience, and a CIBIL score of 750 for the best approval odds. Axis Bank also tends to favour salaried employees at established private companies, MNCs, or government organisations, though this isn't an absolute rule.

For self-employed applicants, the age ceiling extends closer to 65, but approval is genuinely harder. Income needs to be consistent and properly documented through ITR (Income Tax Return) filings, not just bank statement averages.

If you're specifically looking at Axis Finance, the bank's NBFC arm, the minimum CIBIL score drops to 650, and it's built to handle exactly this kind of multi-loan consolidation, including loan app balances. A straight balance transfer of an existing personal loan into Axis Bank itself, separately, typically needs a CIBIL score of 720 or above with a clean repayment track record.

One more number worth knowing: a processing fee of roughly 1.5% to 2% of your sanctioned loan amount, plus GST, applies either way, and it's non-refundable even if you later decide not to go ahead. Always confirm the exact current figure on axisbank.com before applying.

Axis Bank Debt Consolidation Loan: Key Terms at a Glance

Parameter | Axis Bank Personal Loan | Axis Finance Personal Loan |

Interest Rate | Starting around 9.99% to 10.5% p.a. (varies by profile) | 13% to 18% p.a. |

Loan Amount | ₹50,000 to ₹40 lakh | Varies; covers app loan consolidation |

Tenure | 12 to 84 months | 12 to 60 months |

Minimum CIBIL Score | 750 for standard approval; lower scores may still be considered at a higher rate or smaller amount | 650 |

Processing Fee | Around 1.5% to 2% + GST | As per Axis Finance's schedule |

Foreclosure Charges | Typically 2% to 3% of outstanding principal; may be waived for loans above ₹10 lakh paid from your own funds | Applicable, varies by tenure |

Disbursal Time | Instant for pre-approved customers; 2 to 3 working days standard | 30 minutes to 2 days |

How to Apply for an Axis Bank Debt Consolidation Loan, Step by Step

Apply in the wrong order and you risk a rejection you didn't need, with a CIBIL hit that came along with it. Here's the sequence that actually protects your score.

Step 1: Check Your CIBIL Score First

Before anything else, get your CIBIL score. You can check it for free once a year at cibil.com. You'll want at least 750 for standard Axis Bank approval. Below 700, Axis Finance, with its 650 minimum, is the more realistic option.

Step 2: Calculate Your FOIR

Add up your current monthly EMIs and divide by your take-home salary. Above 50%, a consolidation loan will likely be rejected. Paying off one small loan first, or lowering your credit card utilisation, can bring this number down before you apply.

Step 3: Use Axis Bank's Eligibility Calculator

Visit axisbank.com and run their personal loan eligibility calculator. This is a soft check, it doesn't touch your CIBIL score, and it gives you a realistic loan estimate before you commit to a full application.

Step 4: Gather Your Documents

PAN card, Aadhaar card, your last 3 months' salary slips, 3 to 6 months' bank statements, and statements for every loan or credit card you plan to consolidate. Complete documents up front cut processing time meaningfully.

Step 5: Submit the Application Online or at a Branch

Apply through axisbank.com's personal loan section, or visit your nearest branch. Pre-approved customers can see instant decisions. Standard applications typically take 2 to 3 working days.

Step 6: Use the Disbursed Amount to Close Every Old Debt

The moment the loan lands in your account, pay off everything you planned to consolidate, immediately, not gradually. Collect a NOC (No Objection Certificate, the clearance letter) or No Dues Certificate from each closed account, then set up NACH (auto-payment authorisation) for your new consolidated EMI so you never miss one by accident. If you're unsure which debts to prioritise, or whether this is even the right move for your situation, FREED's counsellors can look at your full picture for free.

Not Sure If You'll Qualify? Check Before You Apply

Free assessment. Understand your CIBIL, FOIR, and real options in one call.

[Get My Free Assessment →]Why Some Borrowers Use FREED Instead of Applying to Axis Bank Directly

Everything above is the real, accurate process for going straight to Axis Bank. For a lot of borrowers, that's the right move, especially if you already bank with Axis or have a clear sense of your own CIBIL and FOIR. But it isn't the only way to get to the same outcome: one loan, one EMI, lower than what you're paying across multiple debts now.

The biggest cost of doing this yourself is often hidden in the process itself. Every bank or NBFC application is its own hard inquiry, the kind of credit check that can drop your CIBIL by 5 to 10 points on its own. Apply to Axis Bank, get turned down, try Axis Finance, then an NBFC, and you can stack up several hard inquiries before you land a yes, each one chipping away at the exact score you're trying to protect.

FREED's Debt Consolidation Program is built around that specific problem. You share your loan and income details once, FREED assesses your full profile, and matches you to a suitable lending partner from its own network, rather than you guessing which bank to try first. FREED handles the paperwork and the coordination with that lending partner from there. You end up in the same place, one consolidated loan, one lower EMI, without taking a separate credit hit for every door you knocked on.

FREED has done this at real scale: 20,000+ accounts settled, 20,00,000+ customers counselled, and ₹3,200 Cr+ in debt managed, with a 4.7-star rating across 3,000+ Google reviews. Like the Axis Bank route, there's no upfront fee, FREED is paid only if the consolidation actually goes through.

Applying to Axis Bank Yourself vs Using FREED

Applying to Axis Bank Yourself | FREED's Debt Consolidation Program | |

Who you deal with | Axis Bank directly | FREED, which matches you to a lending partner |

If you're turned down | You apply elsewhere yourself, another hard inquiry each time | FREED assesses your profile before matching, instead of you applying blind |

Paperwork | You manage forms, follow-ups, and bank coordination yourself | FREED handles the paperwork and coordination |

Eligibility | Fixed to Axis Bank's own published criteria | Matched across a network of lending partners |

Fees | Axis Bank's standard processing fee applies regardless of outcome | Success-based only, nothing if it doesn't go through |

See What FREED Can Do for You First

Free assessment, no commitment. Find out if FREED can match you to a better path than applying yourself.

[Get My Free Assessment →]What Documents Does Axis Bank Require for a Debt Consolidation Loan?

Keep this list tight and complete, since incomplete documents are the single biggest cause of delays.

Standard documents: a completed application form, a passport-sized photo, your PAN card, Aadhaar card, your last 3 months' salary slips, and 3 to 6 months of bank statements showing your salary credits. Self-employed applicants need ITR filings in place of salary slips.

Specific to consolidation: statements for every existing debt you plan to fold in, so the bank can see your total debt burden clearly, not just what you're asking to borrow.

One small cost to know about: if you ask Axis Bank to pull your CIBIL report directly, there's typically a charge of around ₹50 per report plus service tax.

Practical tip: keep every outstanding loan account number on hand. You'll need each one to formally close that account once your consolidated loan is disbursed.

This entire document-gathering and follow-up process, salary slips, statements, ITR filings, chasing down account numbers, is exactly what FREED's counsellors handle on your behalf if you go the FREED route instead.

What the Law Says

Under the RBI Fair Practices Code, banks must clearly disclose all loan terms, interest rate, processing fee, prepayment charges, before you sign the loan agreement. Ask for the Key Facts Statement before accepting any loan offer.

What Is Debt Settlement and How Does It Work?

Does Consolidation Actually Save Money, When Does It Work and When Doesn't It?

Here's the honest math, not the brochure version.

Consolidation saves money when the new rate is meaningfully lower than the weighted average of what you're currently paying, and the tenure isn't stretched so far that total interest eats the savings back up. On a ₹3 lakh credit card balance at 36% a year, moving to a 12% personal loan can save you roughly ₹72,000 a year in interest. That's real money.

But stretch that same ₹3 lakh loan to 84 months at 12% to get a smaller EMI, and total interest paid can climb to somewhere around ₹1.28 lakh, compared to roughly ₹18,000 if you'd repaid it over 12 months instead. A lower monthly number can quietly cost you more overall. Run the actual numbers before choosing a tenure, don't just pick whatever makes the EMI feel comfortable.

There's a second trap, separate from the math: closing the loan but keeping your old credit cards open and active. It's a well-documented pattern, borrowers consolidate, breathe easier, and then slowly run the same cards back up, ending up with both the new consolidation loan and fresh card debt. That's strictly worse than where you started. Closing those old accounts can also cause a small, temporary CIBIL dip, often 5 to 10 points, since your total available credit drops. It typically recovers within 3 to 6 months of clean repayment, a short-term cost worth accepting. Closing or cutting up the cleared cards isn't optional, it's the part that makes consolidation actually work.

See What Consolidation Could Save You

Run your own numbers before deciding on a tenure. The math above is illustrative, your actual debts, rates, and timeline will look different.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

What If You Don't Qualify for a Consolidation Loan, What Are Your Options?

If you searched for this because you've already missed a few EMIs, there's a real chance you won't qualify for a standard consolidation loan right now. That's worth saying plainly, and it isn't a verdict on you as a borrower, it's just where the numbers currently stand.

It matters which of these two situations you're actually in, because the right next step is different for each.

If you're still current on payments, just stretched thin across too many of them: this is exactly the gap between "doesn't fit Axis Bank's specific bar" and "is in real trouble." FREED's Debt Consolidation Program exists for precisely this situation. Instead of applying bank by bank and racking up hard inquiries, FREED assesses your full profile and matches you to a lending partner from its own network that can disburse one consolidated loan. It doesn't damage your CIBIL, your score typically starts improving once you're on one regular payment instead of several. It's free to find out if you qualify, and FREED is only paid if the consolidation goes through.

If you've already missed EMIs and your income genuinely can't support what you currently owe: a consolidation loan, from Axis Bank, Axis Finance, FREED's network, or anyone else, isn't the right tool anymore. Debt settlement is the structured last resort here. Settlement is not something a borrower chooses out of preference. Banks only consider it when there's a genuine inability to pay. FREED works with banks to bring down what you owe by up to 50%*, with fees charged only on a successful settlement. Be clear-eyed about the cost: the "Settled" mark stays on your CIBIL for up to 7 years. But staying in default does ongoing damage too, every month it continues. At some point, resolving the debt matters more than protecting a score that's already taken the hit.

A third, narrower option also exists either way: a bank or NBFC with a lower CIBIL bar than Axis Bank's, Axis Finance accepts down to 650, and other NBFCs may go lower still, usually at a higher rate, often 18% to 24%. Or simply asking your existing banks for EMI relief directly: a lower EMI, a longer tenure, or a short payment pause. Banks are required under the RBI Fair Practices Code to consider genuine hardship requests, even if they don't advertise this loudly.

*Settlement reduction of "up to 50%" is indicative only. Final terms are decided by the bank. FREED is not a Loan Provider. No outcome is guaranteed. Please verify directly with your bank.

Multiple EMIs Eating Your Salary?

Find out if consolidation or settlement is right for you, free.

[Book My Free Call →]What Helps When You're Trying to Consolidate Debt, Practical Checks Before Applying

A few habits make the difference between this going smoothly and it backfiring.

Check your CIBIL score before applying, not after. A free check is available once a year at cibil.com.

Calculate your FOIR honestly: total monthly EMIs divided by take-home salary. Above 50%, fix that first.

Use Axis Bank's online eligibility calculator before you submit a full application. It's a soft inquiry only, so it costs you nothing to check.

Don't apply to multiple banks at the same time. Each application is a hard inquiry on its own, and three rejections in a row can drop a healthy 750 score below 720, even if you never missed a single payment.

Once you've consolidated, close the old accounts properly, and physically cut up the cards. An open, unused credit line is still a temptation.

And set up NACH (auto-payment authorisation) on your new consolidated EMI immediately. A missed payment on the new loan is the single most common way people lose everything consolidation was supposed to fix.

If working through this checklist yourself feels like more than you want to manage on top of everything else, this is the exact groundwork FREED does for you before matching you to a lending partner.

Ready to See Your Real Options?

By now you have the full picture: how Axis Bank's product actually works, who it's realistically built for, what it costs, and what the math does and doesn't save you. You also have a second path, FREED's Debt Consolidation Program, that gets you to the same outcome without the bank-by-bank legwork or the stacked hard inquiries.

Either way, the first move is the same: find out where you actually stand before you apply anywhere. A free assessment with a FREED counsellor takes one call and tells you your real CIBIL and FOIR picture, whether Axis Bank's criteria are realistic for you right now, and whether FREED's network can do better. No commitment, and no cost either way.

Talk to a FREED Counsellor Before You Apply Anywhere

One free call. Real numbers on your CIBIL, FOIR, and options, Axis Bank, Axis Finance, FREED, or settlement.

[Get My Free Assessment →]FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions