What is DPD in CIBIL? Full Form, Meaning & How to Clear It

DPD full form in CIBIL is Days Past Due. It is the number of days you delayed paying your loan EMI or credit card bill past the due date. CIBIL records DPD every month for each of your loan and credit card accounts for the last 36 months. A DPD of 000 means you paid on time. Any number above 000 hurts your credit score.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

DPD stands for Days Past Due — it is the number of days you paid your loan EMI or credit card bill after the due date, recorded every month for the last 36 months on your CIBIL report.

A DPD of 000 means you paid on time. Anything above 000 hurts your CIBIL score — a single 30-day DPD can drop your score by 50 to 80 points.

Genuine DPD entries cannot be deleted from your report. They stay for 36 months and then drop off automatically. Only wrong DPDs (bank reporting errors) can be disputed and removed.

The more serious the DPD — SUB, DBT, or LSS (written-off) — the harder it is to handle alone. These need active resolution, not just waiting.

If multiple accounts have gone into serious DPD, FREED can step in to negotiate with your banks, get the right CIBIL status update done, and help your score recovery begin.

What is DPD in CIBIL? (Meaning in Simple Words)

DPD stands for Days Past Due. It is a banking term used by CIBIL and every other credit bureau in India.

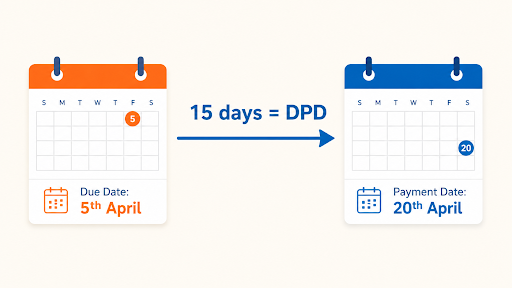

In simple words, DPD is a record of how late you paid your EMI or credit card bill each month. If your due date was 5th April and you paid on 20th April, your DPD for that month is 15.

CIBIL keeps track of your DPD for the last 36 months of your credit history. That means your report shows your last 3 years of monthly payment behaviour for every active loan and credit card.

Here is the part nobody tells you. Having a DPD entry does not mean you are a bad person or that your financial life is over. Many honest, hard-working Indians have DPDs on their report. Job losses happen. Medical bills happen. Sometimes a UPI failure on the due date happens. The number is just data. What you do next is what really decides your future.

How is DPD calculated in CIBIL?

The formula is simple.

DPD = Day you paid the EMI – Day the EMI was due

- Let us walk through it with an example.

- Your credit card bill due date: 5th April

- You actually paid on: 20th April

- DPD for April = 15

A few important things to remember:

- DPD counts every calendar day, including Sundays and public holidays

- Banks and NBFCs report DPD to CIBIL once a month, not daily

- Most loan providers only report a delay if it crosses 30 days, but the rule changes from one bank to another

So if you paid just 2 days late, in many cases it will not show as a DPD in your report. But do not make it a habit. Every bank has its own internal cut-off, and you never know which one is strict.

What Do DPD Values Mean? (Decoding Your CIBIL Report)

DPD Value | What It Means | Impact on CIBIL |

000 | Paid on time | ✅ Healthy |

XXX | Bank did not report data for that month | ⚪ Neutral, no impact |

STD | Standard. Paid within 90 days but a little late | 🟡 Mild negative |

30 | 30 days late | 🟠 Negative |

60 | 60 days late | 🔴 Serious |

90 | 90 days late | 🔴 Major hit |

SMA | Special Mention Account (early warning) | 🚨 Pre-default flag |

SUB | Sub-standard. 90+ days overdue (NPA stage) | ⚠️ Severe |

DBT | Doubtful. Sub-standard for 12+ months | ⚠️ Severe |

LSS | Loss. Bank has written it off | ❌ Worst |

What is SMA in CIBIL?

SMA stands for Special Mention Account. It is an early warning system created by RBI. Think of it as a yellow light before the red one.

SMA-0 = Account overdue by 1 to 30 days

SMA-1 = Account overdue by 31 to 60 days

SMA-2 = Account overdue by 61 to 90 days

After 90 days, the account becomes an NPA (Non-Performing Asset)

If you see SMA on your report, it means your account is on the watchlist. This is the time to act, not the time to panic.

How Much Does DPD Affect Your CIBIL Score?

Payment history is the single biggest factor in your CIBIL score. It carries roughly 30 to 35% weightage, more than anything else on your report.

Here is the rough impact of different D PDs:

- One 30-day DPD entry can drop your score by around 50 to 80 points

- One 90-day DPD entry can drop your score by 100+ points

- Multiple DPDs across different months can push your score below 600

And the damage does not stop at the score itself. Once your score falls:

- New loan applications get rejected

- The few approvals you get come with much higher interest rates

- Banks may reduce your credit card limit

- Some banks may even close your unused cards

This is why one small slip-up gets compounded. The score falls, then your borrowing options shrink, then handling existing EMIs gets harder. That is how a small delay becomes a big problem if it is not addressed.

Where to Find DPD in Your CIBIL Report

Finding your DPD is easier than people think. Just follow these steps.

1. Open your CIBIL report PDF

2. Scroll to the "Account Information" section

3. Find each of your loan and credit card accounts

4. Look at the "Payment History" sub-section under each account

5. You will see a 36-month grid with DPD values for each month

That grid is exactly what you are looking for. Each cell tells you how you paid tha

Why You Got DPD Entries Common Reasons

Before we talk about fixing it, let us talk about how it happens. Because in most cases, DPDs are not caused by bad money habits. They are caused by real life.

1. Salary delay or sudden expense A medical emergency. A delayed salary. A family wedding that cost more than planned. These are not failures. These are life events.

2. Too many EMIs eating your salary When more than half your income goes to EMIs, one bad month is all it takes. The first missed payment becomes the first DPD.

3. You simply forgot the due date Auto-debit failed because of low balance. The reminder SMS got lost in the spam folder. Suddenly the date passed.

4. Minimum due confusion on credit cards You thought paying the minimum due was enough. In most cases it is. But for some banks and certain product types, a part of the unpaid balance still gets flagged.

5. Bank reporting error Yes, this happens more than you would think. Sometimes banks report a payment as late even when you paid on time. Wrong DPDs do show up, and they can be fixed.

Can You Remove DPD from Your CIBIL Report?

Let us be honest here. Genuine DPD entries cannot be removed. Only wrong ones can be disputed and corrected.

There are two paths forward, depending on which one you have.

Path A: If the DPD is wrong (not your fault)

This happens when:

- The bank reported a payment as late, but you actually paid on time

- A loan or card on your report does not even belong to you (identity mix-up)

- The amount shown is wrong

In these cases, you can raise a dispute with CIBIL through their official website. CIBIL will contact the bank to verify. If your case is proven correct, the DPD entry is removed within 30 days.

Path B: If the DPD is correct (you really did pay late)

This is the harder reality. A genuine DPD stays on your report for 36 months. After that, it automatically drops off.

But there are still things you can do to reduce the damage right now:

- Stop the bleeding. Clear all current overdues. Stop new DPDs from getting added every month.

- Settle written-off accounts properly. This is where most people make mistakes and the bad status stays forever.

- Build new positive history. Every clean payment from today onwards will start outweighing the old damage.

When you have multiple DPD entries across several accounts, and especially when some have already gone into SUB, DBT, or LSS, doing this alone gets very tricky. At FREED, we work directly with your banks and NBFCs to settle those accounts the right way, so your CIBIL recovery can actually start.

Settlement amounts are indicative. Final terms are decided by your bank or NBFC. FREED is not a lender and does not guarantee approval. All settlement offers require bank verification.

FREED Expert Tip

DPD entries are like scars on your CIBIL report. The fresh ones hurt the most. The older they get, the less they impact your score. But if you have written-off (LSS) or doubtful (DBT) accounts sitting on your report, those will not fade away on their own. They need active resolution. The longer you wait, the harder it gets.

Talk to us →How to Clear DPD in CIBIL Report Step by Step

Here is the plan we follow with our customers at FREED. Simple steps, real results.

Step 01: Get Your Latest CIBIL Report We help you pull your most recent CIBIL report and read every DPD entry with you.

Step 02: Identify Errors First We mark every DPD that looks wrong, because those are the easiest wins.

Step 03: Raise the Dispute for Wrong DPDs We file the dispute with CIBIL, attach proof, and follow up until the entry is corrected.

Step 04: Clear All Current Overdues We help you stop new DPDs from getting added each month going forward.

Step 05: For Written-Off or Settled Accounts, We Step In This is where most people get stuck on their own. We negotiate directly with your bank, ensure the right status update is done, and chase them until your CIBIL report reflects the resolution.

Step 06: Stay Disciplined for 12 to 18 Months Every clean payment from here on starts repairing your score. Most FREED customers see real CIBIL improvement within 6 to 12 months.

What the Law Says

Under RBI guidelines, every bank and NBFC must report your payment data to CIBIL every single month. They must also correct any wrong entry within 30 days of you raising a dispute. No bank can refuse to update your CIBIL once a settlement is completed and the dues are cleared as per agreed terms. If your bank delays or refuses, you have the legal right to file a complaint with the RBI Ombudsman.

Know your full rights as a borrowerDPD vs CIBIL Score vs Settlement What's the Difference?

DPD | CIBIL Score | Settlement Status | |

What it is | Monthly delay record | A 3-digit score (300–900) | Tag on a closed account |

Where it shows | Payment history grid | Top of CIBIL report | Account status section |

Time on report | 36 months | Always live | 7 years |

Can it be removed? | Only if wrong | Updates automatically | Status can be improved |

So DPD is the history, CIBIL score is the summary, and settlement status is the closure tag. All three matter. All three need attention.

Stuck with Multiple DPDs Across Accounts? Here's What to Do

Let us be real. If you have a DPD on one credit card, you can probably sort it out yourself.

But the moment 3 personal loans, 2 credit cards, and an app loan all start showing DPDs together, and one of them has already gone into SUB or LSS, this is no longer a DIY situation.

Settlement amounts are indicative. Final terms are decided by your bank or NBFC. FREED is not a lender and does not guarantee approval. All settlement offers require bank verification.

1. Banks do not take individual settlement calls seriously" implies the reader is beneath the bank's attention

2. "You do not know the right legal language to use, directly states reader incompetence

3. "Many borrowers get tricked" is fear-based, shaming readers who got a bad outcome

This is exactly where FREED helps.

1. We work with banks every single day, so they know us and take us seriously

2. We know what each bank's internal settlement system looks like

3. We push for the right CIBIL status updates, not just the cheapest payoff

Worried about DPDs and a falling CIBIL score?

At FREED, we have helped 60,000+ Indians clean up their credit reports the right way. One free call. No judgment. Clear plan.

Get My Free CIBIL Recovery PlanFREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions