What Does SUB Mean in Your CIBIL Report?

SUB in your CIBIL report means Sub-Standard,the RBI's label for a loan you haven't paid in 90 days to 12 months. It is the first stage of NPA (Non-Performing Asset, a loan the bank now treats as bad debt). Your score has likely dropped 100–250 points. Recovery calls have probably already started. You can still fix this.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

SUB in CIBIL means sub-standard; your loan is overdue between 90 days and 12 months.

It is the first stage of NPA (non-performing asset, a loan the bank marks as bad debt).

Your score has likely dropped 100–250 points from where it was.

You can recover, but the window to act before things get worse is 12 months from the SUB date.

Most people in SUB status need a one-time settlement (OTS) to resolve it cleanly and stop the score from dropping further.

What Does SUB Mean in Your CIBIL Report?

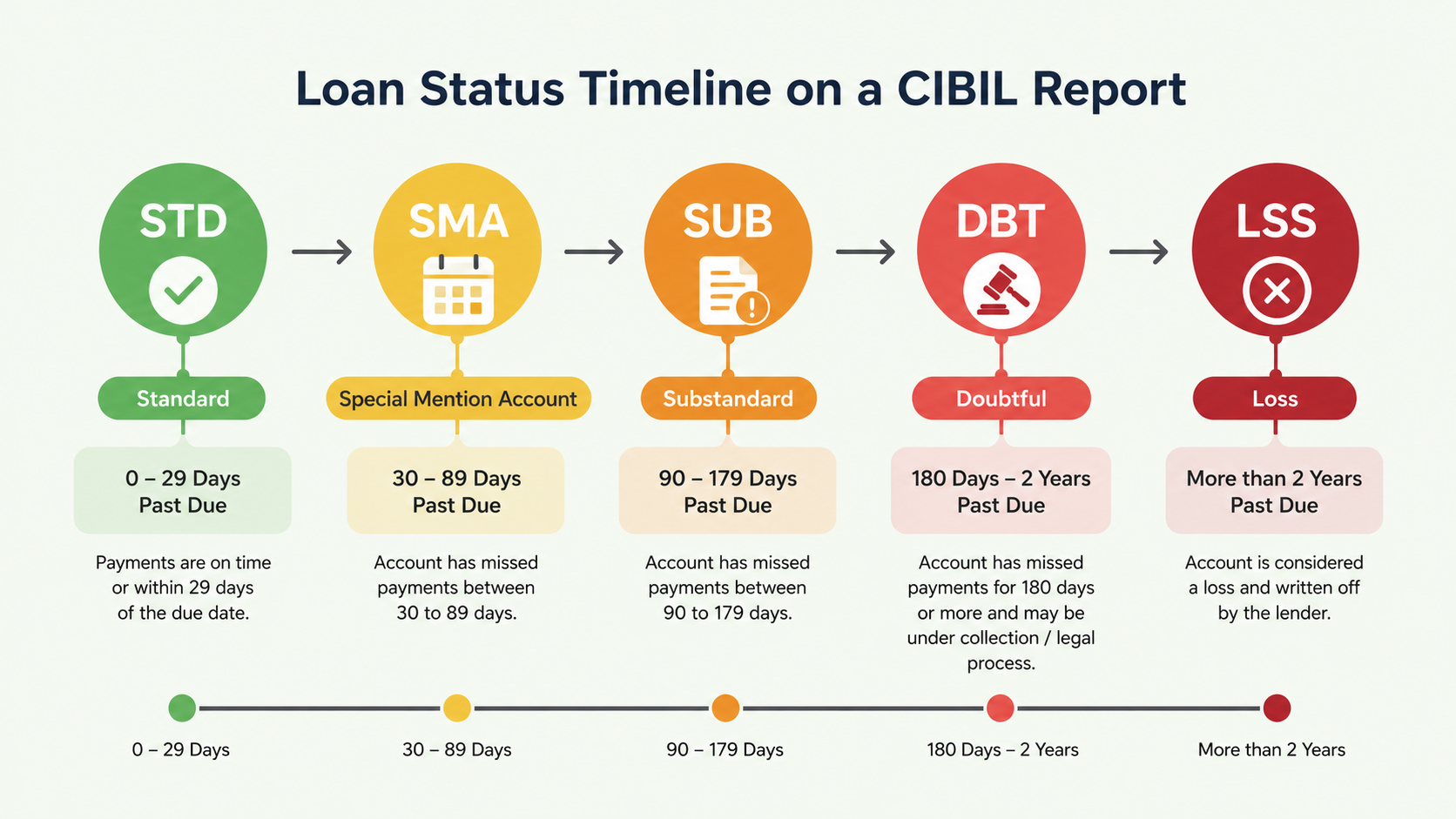

SUB means Sub-Standard, a classification the RBI assigns to any loan that has been overdue for 90 days to 12 months. Sub-Standard (a loan the bank now treats as bad debt, stage 1 of NPA) is the first formal step in the bank moving your account from healthy to problem.

Before SUB, your loan was listed as STD (Standard, being repaid on time). Once you crossed 90 days without paying, the bank reclassified it internally. They stopped expecting full repayment on the original schedule.

SUB is not the end of the road. But it is a serious marker. The stages after it are harder to come back from:

- STD → SMA (Special Mention Account, early warning)

- SUB (Sub-Standard, 90 days to 12 months overdue)

- DBT (Doubtful, 12 months or more overdue)

- LSS (Loss,fully written off, the worst classification)

As per RBI's IRAC norms (Income Recognition and Asset Classification norms, last updated July 2015), any loan overdue 90+ days is automatically reclassified. The bank does not need to inform you first. It happens in their system.

Your loan is already SUB. Stop the bleed

Talk to a FREED counsellor. Free. Confidential. No bank involved.

Get My Free Assessment.How Did Your Loan Get Marked SUB? (The 90-Day Timeline)

The slide from STD to SUB does not happen overnight. Here is how it typically moves:

- Day 0–30: You missed one EMI. Status: SMA-0 (early warning flag in the bank's system).

- Day 31–60: Status: SMA-1. Bank calls start. SMS reminders increase.

- Day 61–89: Status: SMA-2. Field collection visits may begin. Legal warning letters go out.

- Day 90+: Status flips to SUB. Your loan is now officially NPA (non-performing asset,a loan the bank has stopped treating as healthy).

- After 12 months unpaid: Slides to DBT (Doubtful,harder to negotiate, lower waiver offers).

- After 3 years unpaid: Slides to LSS (Loss,the bank writes it off. Score hits rock bottom).

If you are reading this, you are somewhere between Day 90 and Day 365. The window to fix this without permanent damage is still open. It will not stay open.

FREED Expert Tip

The bank has 90 days from your last payment to classify you as SUB,but they have up to 12 months before sliding you to DBT. That 12-month window is your best chance to negotiate a one-time settlement. After DBT, waiver offers get smaller and the process gets longer.

How does loan settlement work in India?What Does SUB Status Actually Do to Your CIBIL Score?

The number drop is the first thing people want to know. Here is what actually happens:

- SUB classification typically causes a score drop of 100–250 points. A score of 720 can land in the 520–620 range.

- The SUB tag shows in the DPD (Days Past Due, howDue,how many days late you have been) section of your report. It stays visible there for 36 months from the last reporting date.

- It also stays in your account history section for 7 years from the date the account is finally closed or settled.

- Every additional month unpaid causes a further score drop, until the account slides to DBT.

- Loan apps and banks use auto-decisioning systems. They spot SUB status instantly and reject the application. You will not get a reason. The system simply says no.

Most people focus on the score number. That is not the real damage. The real damage is time,every month you wait, the deal you can negotiate gets worse and the score takes another hit.

Can You Remove SUB From Your CIBIL Report Yourself?

The short answer is no,you cannot remove the SUB tag. But you can change the status, stop the bleeding, and begin the score recovery. Here are your 4 options, honestly explained.

- Option 1: Pay the Full Overdue Amount

This is the cleanest path. Pay the full outstanding amount, what you originally borrowed, plus the interest that has built up, plus any late fees. The bank then updates your status to Closed over the next 1–2 reporting cycles.

The problem: most people in SUB status cannot pay the full amount. That is exactly why they hit 90 days in the first place.

- Option 2: Change the Repayment Plan with the Bank

RBI allows banks to restructure NPA accounts (change the repayment plan, spread out what you owe over a longer time). The bank needs proof that your income has recovered enough to support the revised plan. You will need salary slips, bank statements, and a letter explaining your situation.

Banks reject most of these requests. You do not control the decision; the bank does.

- Option 3: One-Time Settlement (OTS)

OTS (one-time settlement, paying a reduced amount once, and the matter ends) means you pay 30–60% of the outstanding as a full and final payment. The status on your CIBIL report changes to "Settled" rather than "SUB."

"Settled" is still a negative tag and it stays for 7 years. But it stops the score from dropping further. It stops recovery calls. It removes the risk of legal action. For most people in SUB, this is the most realistic path forward.

- Option 4: Dispute (Only If It Is a Reporting Error)

If you actually paid your EMIs on time and the bank still shows you as SUB, that is a reporting error. File a dispute directly on the CIBIL portal. The process takes around 30 days. This option only applies to genuine errors; it cannot be used to erase a real default.

What the Law Says

Under RBI's Master Circular on IRAC norms, once an account is classified as SUB, the bank cannot remove the tag retroactively,even if you pay the full outstanding amount in one go. The status changes to "Closed" or "Settled." It does not go back to STD (Standard). The history stays.

Can you remove NPA from CIBIL report?Why Settling SUB-Status Loans Yourself Is Harder Than It Looks

Going to the bank directly is not wrong. But there are 3 ways it tends to go wrong,and each one costs money.

- You will likely over-pay. Banks open OTS discussions at 70–80% of the outstanding amount. Most borrowers settle there because they do not know how much lower a final agreement can go. People who are familiar with the process and know what to ask for at which stage tend to get significantly better outcomes. On a ₹5 lakh outstanding, even a 10–15% difference in the final number is ₹50,000 to ₹75,000 in real money.

- You may sign the wrong papers. Banks issue two separate documents: a Settlement Letter and a No Dues Certificate (clearance letter confirming nothing is owed). Most borrowers accept only the Settlement Letter. Six months later, recovery calls start again because a different department in the same bank was never updated. You need both documents,by name, in writing, before any payment is made.

- You may miss a better tag. The status "Settled" is what the bank reports once an OTS is completed. This stays on your CIBIL report for up to 7 years and does affect future loan applications. Understanding what this means for your credit timeline, and how to manage the rebuild after settlement, is something a FREED counsellor walks you through before you sign anything

Loan settlement is not a casual phone call. It is a structured process with specific documentation, specific asks at specific departments, and specific timelines. People who handle these cases regularly get better outcomes,not because they are tougher,but because they know exactly what to ask, from whom, and when.

Settle smarter. Pay less. Sleep tonight.

FREED has settled SUB-status accounts with every major bank in India. Average waiver: up to 50%

Talk to a Counsellor,FreeHow Does FREED Help You Recover From SUB Status?

FREED works on 3 steps. No pressure, no jargon, no running around banks alone.

- Step 1: Free Assessment. A counsellor pulls your CIBIL report, maps every SUB account, and estimates a realistic waiver for each one.

- Step 2: Negotiate. The team handles the negotiation and all paperwork on your behalf. FREED communicates directly with the bank, pushes for the best possible reduction, and makes sure you get both the Settlement Letter and the No Dues Certificate. If calls from the bank or recovery agents turn threatening or abusive, FREED helps you understand your rights and what steps you can take.

- Step 3: Closure and Score Rebuild. Once settled, the correct status gets reported to CIBIL. Your counsellor gives you a 24-month plan to bring your score back to 750+.

FREED charges only on successful settlement. If your dues are not reduced, you pay nothing.

One thing to know: FREED handles unsecured loans only, credit cards, personal loans, BNPL, and loan apps. Home loans and car loans involve property (secured loans like home/car loans have a different legal process). If your SUB account is a personal loan or credit card, FREED can take it on.

What Happens If You Ignore SUB and Let It Slide to DBT or LSS?

Ignoring SUB is not a strategy. Here is what actually happens at each stage:

DBT - Doubtful (12+ months of no payment): Your score typically floors around 450. Almost no mainstream bank or NBFC will approve any credit. Recovery agents are often replaced by lawyers at this point.

LSS - Loss (3+ years, written off): The bank has fully written off the account. Status on CIBIL reads "Written-off",the worst tag on the report. It stays 7 years from the date of closure. Some banks blacklist the borrower internally, which can affect all future dealings with that bank.

Legal action: For unsecured loans, banks usually file under Order 37 of the Civil Procedure Code. Court summons typically begin arriving 8–14 months after default in most cases. For larger loan amounts, Section 138 of the Negotiable Instruments Act (cheque bounce law,can become criminal) may also apply if post-dated cheques were part of the original loan agreement.

Every month you wait in SUB, the settlement amount you can negotiate gets higher and the waiver you can get gets smaller.

How Long Does SUB Stay on Your CIBIL Report After Recovery?

Here is the direct answer by section of your CIBIL report:

- DPD (Days Past Due) section: Visible for 36 months from the last date of reporting. This is what new loan approvers look at first.

- Account history section: Visible for 7 years from the date the account is finally closed or settled.

- If you pay in full: Status updates to "Closed." Score recovery typically takes 6–18 months, depending on how clean the rest of your credit behaviour is during that time.

- If you settle via OTS: Status updates to "Settled." Score recovery takes 18–30 months. New loan approvals will be harder during that window,but not impossible, especially if you keep all other accounts clean.

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions