Personal Loan Settlement Calculator: How to Estimate Your Settlement Amount

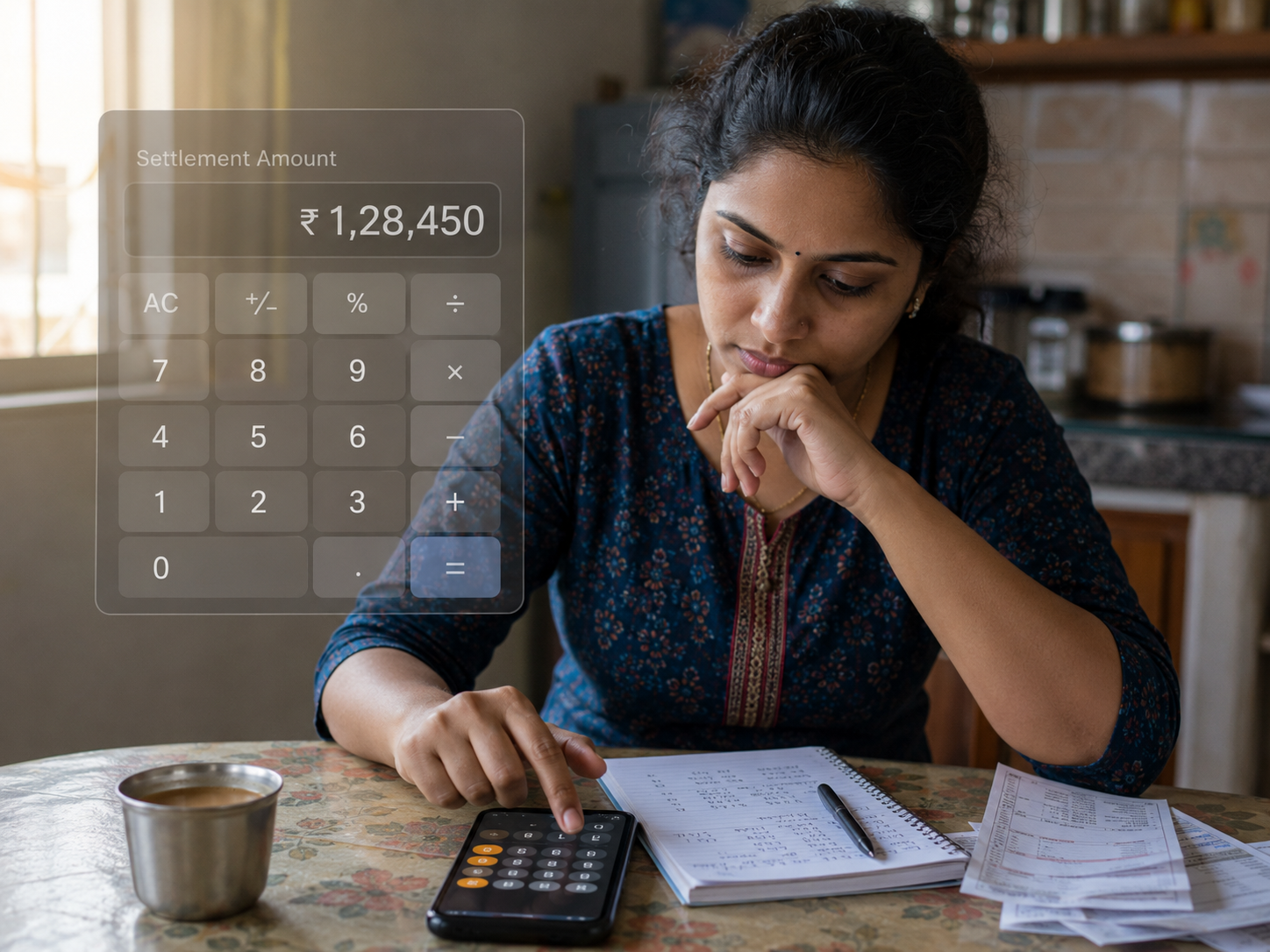

A personal loan settlement calculator estimates how much you might pay to resolve a defaulted loan through a one-time settlement (OTS, paying it once and the matter ends). It uses your outstanding principal, accrued interest, late fees, and a likely waiver percentage to give you a ballpark figure before you walk into any negotiation. It doesn't give a guaranteed number. But it gives you a starting point.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

A personal loan settlement calculator estimates your OTS amount using outstanding balance, interest, fees, and a discount range

FREED helps borrowers settle their unpaid/overdue loans at up to 50%* less. But only after genuine inability to pay, not preference. The 'Settled' status may remain on your credit report for an extended period and can affect future borrowing eligibility. The "Settled" remark stays on your CIBIL (India's primary credit bureau) report for up to 7 years and drops your score by 70–100 points

RBI data shows banks recovered nearly ₹33,000 crore through OTS in FY 2023–24, proving settlement is a legitimate, structured process

FREED has helped thousands of enrolled customers settle personal loans at up to 50%* less than what they owed

What Goes Into the Settlement Amount Calculation?

Most people think of their personal loan in terms of what they originally borrowed. That number, the principal is just one part of what the bank counts as your total outstanding. By the time you've missed 3 to 6 EMIs, the real figure can be much larger.

Banks use 4 components to calculate total outstanding:

- Outstanding Principal: The portion of the original loan you haven't repaid yet

- Accrued Interest: Interest that kept building during the period you didn't pay

- Penal Interest: Interest-on-interest charged specifically for missed payments

Late Fees and Legal Charges: Recovery costs the bank has incurred, including field agent visits, legal notices, and processing fees

Borrowers are often shocked when they see this number. They expected ₹3 lakh outstanding, and the bank presents ₹5.3 lakh. The difference is everything listed above stacking up over months.

When a bank considers an OTS (one-time settlement, paying it once and the matter ends), they don't waive everything equally. Penal interest and late fees go first. A portion of accrued interest may follow. The principal itself is the last thing a bank touches, and they protect it hard. For loans that have been in default for 2 or more years, the bank has had longer to provision against the loss, so they may accept a deeper discount than they would for a loan only 6 months overdue.

Understanding this breakdown is what separates a borrower who negotiates well from one who walks in underprepared.

What Is the Formula Banks Use to Estimate a Settlement Amount?

Component | Amount |

Outstanding Principal | ₹3,50,000 |

Accrued Interest + Penalties | ₹1,80,000 |

Total Outstanding | ₹5,30,000 |

Waiver Scenario | Waiver Amount | Settlement Amount |

30% waiver | ₹1,59,000 | ₹3,71,000 |

40% waiver | ₹2,12,000 | ₹3,18,000 |

50% waiver | ₹2,65,000 | ₹2,65,000 |

These are estimates. The bank decides the actual number based on your case, your documentation, and their current recovery targets. No calculator can tell you exactly what your bank will accept. What it can do is show you the range, so you know what ₹2.5 lakh versus ₹3.7 lakh looks like and plan your lump sum accordingly.

What Factors Actually Decide Your Settlement Percentage?

Banks don't flip open a manual and look up a fixed percentage. They evaluate your case across 5 factors:

1. Age of the Default - The longer a loan has sat unpaid, the more the bank has spent on recovery, legal notices, field agents, and write-off provisioning. A loan that's been an NPA (loan marked as bad by the bank, usually after 90 days of missed EMIs) for 18 months is more expensive for the bank to hold than one that crossed 90 days last month. That translates into more room to negotiate for the borrower.

2. Type of Bank - Public sector banks like SBI, PNB, and Bank of Baroda follow rigid, committee-approved OTS schemes. Private banks like HDFC, ICICI, and Axis Bank negotiate case by case faster but more aggressively in early stages. NBFCs (non-banking financial companies) are often the most flexible because their priority is principal recovery, not full-amount maximisation.

3. Principal vs. Interest Mix - If your total outstanding is heavily weighted toward accrued interest and penalties, the bank has more room to waive, because these were never "real money" they lent you. A loan where the bulk is still outstanding principal is harder to settle at a deep discount.

4. Demonstrable Financial Hardship -. Written proof of why you cannot pay, a termination letter, hospital bills, and GST returns showing a revenue drop are not just helpful. It's the single biggest lever you control. Banks are more willing to accept a lower offer when the hardship is real and documented.

5. Lump Sum Availability Banks strongly prefer one payment over 2 or 3 installments. If you can offer a lump sum, say so. If you can't, some banks will accept a short payment plan, typically 30–60 days, but expect a smaller waiver in return.

Find Out Exactly How Much You Could Settle For

Free Evaluation. Real settlement range. No commitment needed.

Get My Free EvaluationWhat Are Your Options Before You Decide to Settle?

Settlement is not something a borrower chooses out of preference. Banks and financial companies only consider it when you are in genuine financial difficulty and truly unable to repay the full amount. Before you go this route, exhaust these 3 options first.

1. EMI Restructuring Contact the bank's collections department, not the customer helpline, and ask if your loan can be restructured. This means changing the loan plan: extending your repayment time reduces the monthly EMI. You pay more in total, but the monthly burden becomes manageable. Some banks do this without requiring you to be in default yet.

2. Temporary Moratorium (Pause) If you're salaried and can prove a temporary income disruption, some banks offer a 2–3 month payment pause (moratorium). This doesn't reduce your outstanding, but it buys time. It needs documented proof, a pay cut letter, a medical certificate.

3. Debt Management Programme A structured plan where you pay 1 consolidated monthly amount through a third party, covering multiple loans at revised rates. FREED offers this for enrolled customers as an alternative to settlement. If your income can support a lower EMI but not your current one, this is worth exploring before taking the settlement route.

Settlement has long-term implications that should be carefully considered before proceeding. Once the "Settled" mark is on your CIBIL report, it stays for up to 7 years. That affects future loan applications, rental agreements, and some employment background checks. If any of the 3 options above can work for you, try them first.

FREED Expert Tip

If a large share of your take-home salary is already going toward loan repayments. , that's the point to act, not wait. Waiting doesn't reduce the outstanding; it adds to it

Know your optionsHow Does Personal Loan Settlement Actually Work Step by Step?

- 1

Get your loan statement

Request a current statement from your bank showing outstanding principal, accrued interest, and all fees. Don't rely on the app balance; it may not include all accumulated charges. This number is your negotiating baseline.

- 2

Run the calculator

Use the formula or the tool above to estimate your range. Decide a realistic lump sum you can actually pay, not a number you're hoping to have someday.

- 3

Contact the right department

Call the number on your recovery notice or visit the branch. Ask specifically for the collections or OTS (one-time settlement) team. Don't start with customer service; they can't process this.

- 4

Submit a written hardship letter

Draft a letter addressed to the Collections Department. Explain your income, expenses, and the reason you cannot repay in full. Attach supporting documents: salary slip or termination letter, medical bills, and bank statements for 3–6 months.

- 5

Make your opening offer

Start below what you can actually afford to pay. Expect the bank to counter. The final amount depends on how long your loan has been in default, your documented financial situation, and whether the bank has an active OTS scheme at that time. There is no fixed percentage every case is different. Don't show your maximum capacity upfront.

- 6

Get the agreement in writing

Never pay without a signed settlement letter. It must state the exact amount, due date, account number, and the phrase "Full and Final Settlement." No written letter means no transfer.

- 7

Collect your NOC (clearance letter)

After payment, collect your No Objection Certificate and Settlement Certificate. Confirm the bank will report "Settled" to CIBIL within 30–45 days. Follow up yourself at the 45-day mark.

What the Law Says

Under RBI guidelines, banks must follow a board-approved, non-discretionary OTS policy. A bank cannot arbitrarily reject a genuine, documented settlement proposal.

Know your rightsHow Does FREED Help With Personal Loan Settlement?

Settlement is not something a borrower chooses out of preference. It's a structured process for people who genuinely cannot repay, and it produces better outcomes when handled by someone who knows the entire process and is an expert on this.

FREED handles what most borrowers find the hardest parts: the paperwork, the back-and-forth with the bank's collections team, getting the hardship documentation in the format that carries weight, and following up until the NOC (clearance letter) actually arrives. The advantage isn't insider knowledge. It's experience hundreds of settled accounts across different banks, different outstanding amounts, and different case ages. FREED's counsellors know what a credible hardship case looks like and how to present it so the bank takes it seriously.

FREED also doesn't hide the CIBIL impact. The "Settled" mark will appear on your report for up to 7 years. FREED doesn't promise credit recovery; it negotiates settlement. Once the loan is resolved, FREED helps borrowers understand the next steps after settlement. But that's separate from the settlement itself.

FREED has helped thousands of borrwers settle personal loans at up to 50%* less than the total outstanding.

Fees are charged only on successful settlement. There's no upfront cost.

What Should You Know Before Using a Settlement Calculator?

A few things that make the calculation more accurate, and a few that can throw it off.

- Always use Total Outstanding, not just principal. The principal is what you borrowed. The bank's number includes interest, penalties, and fees. If you plug in only the principal, your estimate will be significantly lower than reality.

- Treat the output as a negotiating range. The calculator gives you a floor and a ceiling. It doesn't tell you where your bank will land. Use it to decide what lump sum you can realistically arrange, then work backward.

- Build a buffer. If you plan to offer ₹2.5 lakh, make sure you actually have ₹2.7 lakh available. Settlements fall apart when payment is delayed or arrives short. A lapsed offer means starting the conversation over, sometimes at a worse number.

- Don't show your full capacity. If you tell the bank you can pay ₹3 lakh, Start lower. Let the counteroffer come to you.

- Get every commitment in writing before you transfer money. A verbal agreement means nothing. A signed settlement letter means everything.

Banks prefer a single lump-sum payment but may accept 2–3 instalments over 30–60 days in some cases. A missed instalment typically voids the settlement agreement entirely.

Your next step: run the calculator above, or call your bank's collections department. If you'd rather have someone else handle it, speak to a FREED counsellor, free, no commitment.

Talk to a Counsellor Before You Negotiate.

One call. No pressure. We'll tell you what's realistic.

Book Your Free CallHow Do Different Banks Approach Personal Loan Settlement?

Lender Type | Flexibility | Who Decides | Typical Waiver Range | Speed |

Public Sector Banks (SBI, PNB, Bank of Baroda) | Lower follows the rigid OTS scheme | Circle/Zonal Office | 20–40% | Slower Committee approval required |

Private Banks (HDFC, ICICI, Axis) | Higher case-by-case | Collections Manager | 30–50% | Faster, but aggressive in early stages |

NBFCs (Bajaj, Tata Capital, Muthoot) | Highest principal recovery priority | Branch Head | 35–55% | Fastest |

Fintech / Loan Apps | Varies widely | Automated + manual review | 20–50% | Very fast, but documentation requirements vary |

Waiver percentages are indicative and based on industry patterns. Actual settlement terms depend on your specific account, default history, and documentation. FREED negotiates across all these lender types on behalf of enrolled customers.

About FREED

FREED is India's first debt relief company, founded in 2020 and headquartered in Gurugram. FREED works with people who are unable to repay their unsecured loans, personal loans, credit cards, BNPL, and loan apps and negotiates settlements with the bank on their behalf. FREED covers unsecured debt only; secured loans like home loans and car loans are outside FREED's scope. Fees are charged only on successful settlement.

What Is a Personal Loan Settlement Calculator and Who Is It For?

A personal loan settlement calculator is an estimator, not a binding quote, not a guarantee. It's a tool built for people who've already missed multiple EMIs (Equated Monthly Instalments) and are in genuine financial difficulty. Think job loss, a medical emergency, or a business that stopped generating income. This is not a tool for someone who can pay but would prefer not to.

Here's how it differs from the EMI calculator you may have used before. An EMI calculator looks forward; it tells you what your monthly payments will be on a new loan. A settlement calculator looks backward. It takes stock of what's already owed: the principal you haven't repaid, the interest that has piled up, and the penalties the bank added. Then it estimates what portion you might realistically pay to close the account.

If you're receiving recovery calls right now and you want to know the number before your next conversation with the bank, this tool is for you. It won't give you a final answer. But it will give you a range, so you stop guessing and start preparing.

India's personal loan market grew 19% year-on-year in 2024. Default rates among urban households have climbed alongside that growth. Millions of borrowers are in exactly this position. The calculator exists to help them walk into a conversation with the bank knowing roughly what's on the table.

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions