Myth VS Reality: Understanding Debt Consolidation

Heard that debt consolidation is risky? Or that it ruins your credit score? Most of what people believe about it is simply not true. Let's bust the myths - one by one - in plain simple language.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

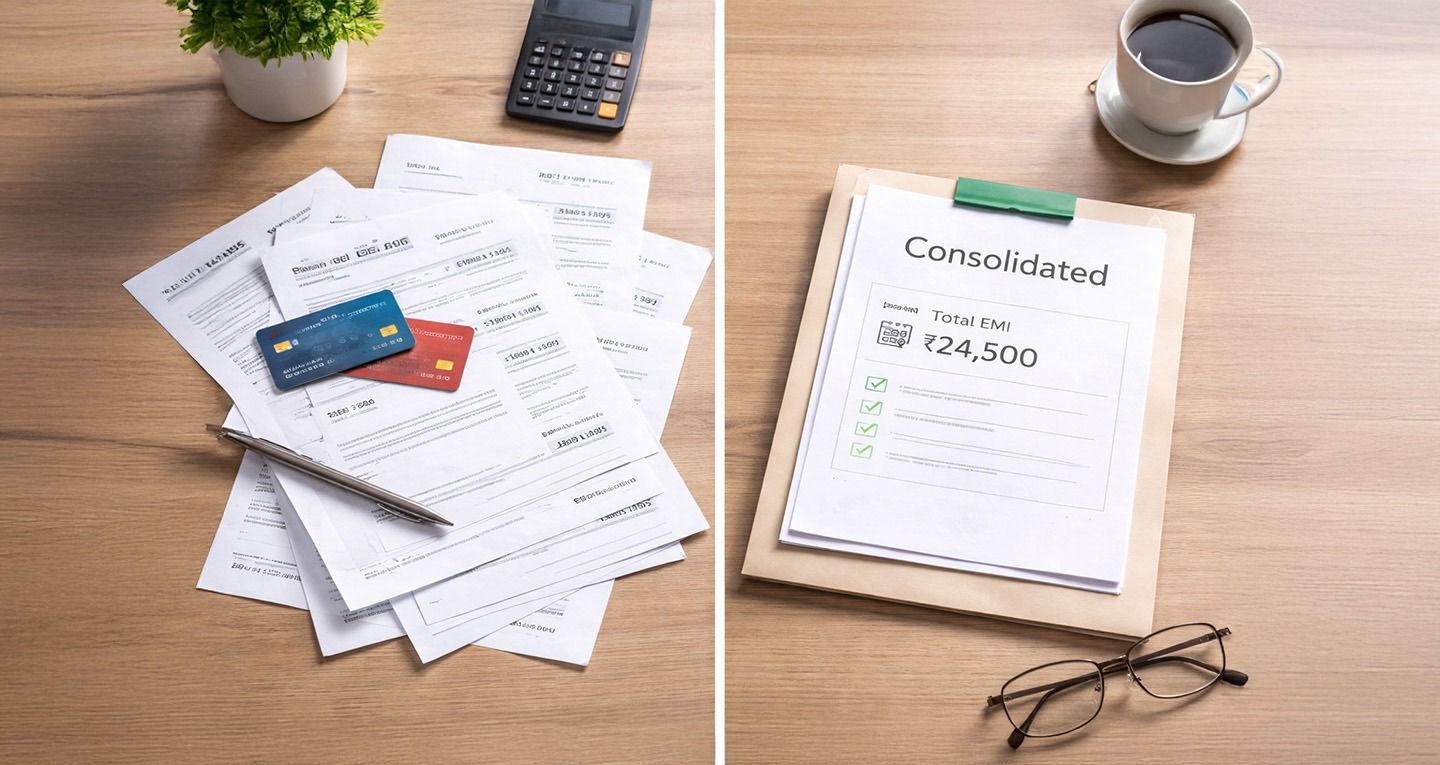

Debt consolidation combines all your loans into one - with a lower EMI and one simple due date every month.

It does NOT make your debt disappear - but it makes repayment far easier and less stressful.

Done right, it can actually improve your CIBIL score over time - not damage it.

It is not just for people who "mismanaged" money - it's a smart financial tool used by lakhs of borrowers across India.

FREED's Debt Consolidation Program is designed specifically for people with multiple loans who need breathing room - without damaging their credit.

What is Debt Consolidation? Let's Start Here.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

Myth 1: It makes your debt disappear

This is the most common myth - and the most dangerous one.

People sometimes think consolidation means getting off scot-free. That somehow the bank forgives everything and you start fresh with zero debt.

That's not how it works.

The Reality: Debt consolidation combines your debts into one loan. You still owe the money. You still have to repay it. What changes is how you repay - in a more manageable, structured way.

Think of it like this. You have 4 glasses of water - all different sizes, hard to carry at once. Consolidation pours them all into one big bottle. The water is the same. But now it's much easier to carry.

The benefit is real - one EMI, lower monthly payment, less stress. But the responsibility to repay is still fully yours.

Myth 2: It ruins your CIBIL score

Many people are scared of this. They think taking a new loan will immediately hurt their credit score and make things worse.

The Reality: Debt consolidation can actually help your CIBIL score over time - if you manage it responsibly.

Here's how:

When you consolidate, you close multiple old loan accounts and open one new one. Yes - there is a small, temporary dip in your score when the new loan application triggers a hard inquiry. That's normal and it's short-lived.

But here's what happens next:

Your credit utilisation drops - because credit card balances get paid off

You make one consistent on-time payment every month

Your score starts recovering within 3–6 months

And improves steadily from there

The real score damage comes from missing EMIs and defaulting - not from consolidating responsibly.

Action | CIBIL Score Impact |

Missing EMIs | Very negative - score drops fast |

Defaulting on a loan | Severe - score can drop 100+ points |

Debt consolidation | Small temporary dip, then improvement |

On-time payments after consolidation | Positive - score steadily rises |

Myth 3: It leads to more debt

Some people worry - what if I consolidate, then start spending on credit cards again and end up with double the debt?

The Reality: Consolidation doesn't create more debt. Your own spending habits do.

This myth has a grain of truth in it - if someone consolidates their credit card debt and then immediately starts maxing out the cards again, yes, they will end up in more debt. But that's a behaviour problem - not a consolidation problem.

Debt consolidation is a tool. Like a knife - it can be used well or badly. The tool itself is not the problem.

The fix is simple. After consolidating, avoid using credit cards for daily expenses. Build a monthly budget. Keep your EMI payments on auto-debit. These habits protect you from falling back.

FREED's program includes budgeting support for exactly this reason - so you don't just consolidate, but stay consolidated.

Myth 4: It's only for people who mismanaged money

There's a feeling of shame around debt. And people assume that if you need consolidation, you must have done something wrong - spent too much, borrowed carelessly, lived beyond your means.

The Reality: Debt consolidation is used by responsible, working people every day - not just those who "messed up."

Life is unpredictable. A pay cut. A medical emergency. A business that slowed down during a difficult year. These are not signs of irresponsibility - they are just life.

Many people who come to FREED for debt consolidation are working professionals, small business owners, and salaried individuals who took loans for genuine needs - a home renovation, their child's education, a medical procedure - and just found themselves stretched thin managing multiple EMIs.

Using a financial tool to manage your situation smarter is not weakness. It is common sense.

What the Law Says

Under RBI's guidelines on Fair Practices, all lenders must give you a clear, written loan agreement with all charges, interest rates, and terms before you sign anything. If any lender is pressuring you to sign without explaining the full cost - that is a violation of RBI's Fair Practices Code. Always ask for a complete written breakup

Know your rights as a borrower in IndiaMyth 5: It's too expensive and complicated

People assume the process must involve lots of paperwork, multiple bank visits, high processing fees, and weeks of waiting. So they don't even try.

The Reality: With the right partner, debt consolidation is actually simpler than managing multiple loans on your own.

Yes - there are processing fees involved. But compare that to what you're currently paying in combined interest on 3–4 high-interest loans. In most cases, the savings far outweigh the one-time cost.

A good debt consolidation program will:

- Explain every fee upfront -no hidden charges

- Do most of the paperwork on your behalf

- Get you a competitive interest rate through lending partners

- Give you a clear timeline for when you'll be debt-free

FREED handles all of this for you - and your first consultation is completely free.

Myth 6: Only banks offer it - and they always say no

Many people assume you have to go to a bank, sit across a desk, and beg for a new loan. And if your credit score isn't perfect, they'll just reject you.

The Reality: Today, debt consolidation is available through NBFCs and lending platforms - not just banks. And eligibility requirements are more flexible than most people think.

FREED works with a network of lending partners specifically for people dealing with multiple loans. We assess your situation first - then match you with the right lender based on your income and debt profile. You don't have to walk into a bank alone and hope for the best.

You may be eligible for debt consolidation if:

- Your CIBIL score is 650 or above

- You have a regular monthly income - salaried or self-employed

- You have 2 or more active loans or credit card dues

- You are currently paying your EMIs - even if it's very tight

Is Debt Consolidation Right for You?

Here's a quick way to check:

Question | Yes? Then... |

Do you have 2 or more EMIs every month? | Consolidation can simplify things |

Is your total EMI more than 40% of your salary? | Consolidation can reduce the pressure |

Are you paying on time but barely managing? | Consolidation is a strong fit |

Is your CIBIL score above 650? | You're likely eligible |

Have you already missed multiple payments? | Debt resolution may suit you better |

Are collection agents calling you? | Talk to FREED immediately |

If you answered yes to 3 or more of the first four questions - debt consolidation is worth exploring right now.

How FREED's Debt Consolidation Program Works

FREED's Debt Consolidation Program is built for people who are still repaying - but finding it very hard to manage multiple EMIs every month.

Here's exactly what happens when you come to FREED:

Step 1 - Free consultation We understand your complete debt situation - all loans, interest rates, monthly payments, and income. No fees. No commitment yet.

Step 2 - We check your eligibility Based on your income and debt profile, we check which of our lending partners can offer you a consolidation loan.

Step 3 - You get one new loan offer We present you a clear offer - new interest rate, new tenure, new single monthly EMI. You see exactly what you'll pay and when you'll be debt-free.

Step 4 - Your existing loans are paid off The new loan amount is used to clear all your existing loans and credit card dues. Those accounts are closed.

Step 5 - You pay one EMI every month One lender. One due date. One amount. That's it.

What you get:

Lower monthly EMI - more breathing room

One simple payment - less stress, less chance of missing a due date

Closed old accounts - clean slate on those debts

A clear debt-free date - you know exactly when it ends

About FREED

FREED is India's first and leading Debt Relief Platform. We help people struggling with credit card bills, personal loans, and multiple EMIs find a legal, stress-free path to becoming debt-free.

We offer two programs - Debt Consolidation (for people who can repay but need a simpler, lower EMI) and Debt Resolution (for people who genuinely cannot repay the full amount). Our certified counsellors guide you through every step - no jargon, no pressure, no hidden charges.

Over 60,000 Indians - from Lucknow to Surat, Bhopal to Patna - have used FREED to take back control of their finances.

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions