Minimum Amount Due Meaning: The Exact Definition and What It Costs You

it is the smallest amount you must pay on your credit card bill by the due date to avoid a late payment charge and keep your account active. In India, this is typically 5% of your total outstanding balance, plus any EMIs, fees, and unpaid dues from the previous month. But paying this amount does not stop interest from building on the remaining balance. It only stops the penalty.

FREED India

Reviewed by FREED India, SEO Intern

Key summury

Minimum amount due (also called MAD) is usually 5% of your total credit card bill paying it avoids a late fee, but does not reduce your debt in any meaningful way.

Interest rates on unpaid balances can be among the highest of any retail credit product. one of the highest rates on any credit product in India.

Only 40% of Indian credit card holders repay their full outstanding amount every month, according to an RBI report, the rest carry a balance that compounds month after month.

A ₹50,000 credit card balance paid at the minimum due only can take over 11 years to fully clear and cost more than ₹1.28 lakh in total.

Credit card delinquencies in the 91–360 days overdue category rose 44.3% year-on-year between March 2024 and March 2025, per CRIF High Mark data.

If credit card debt has crossed the point where even you’re unable to pay minimum payments, FREED can help you assess your options free, confidential, and no commitment.

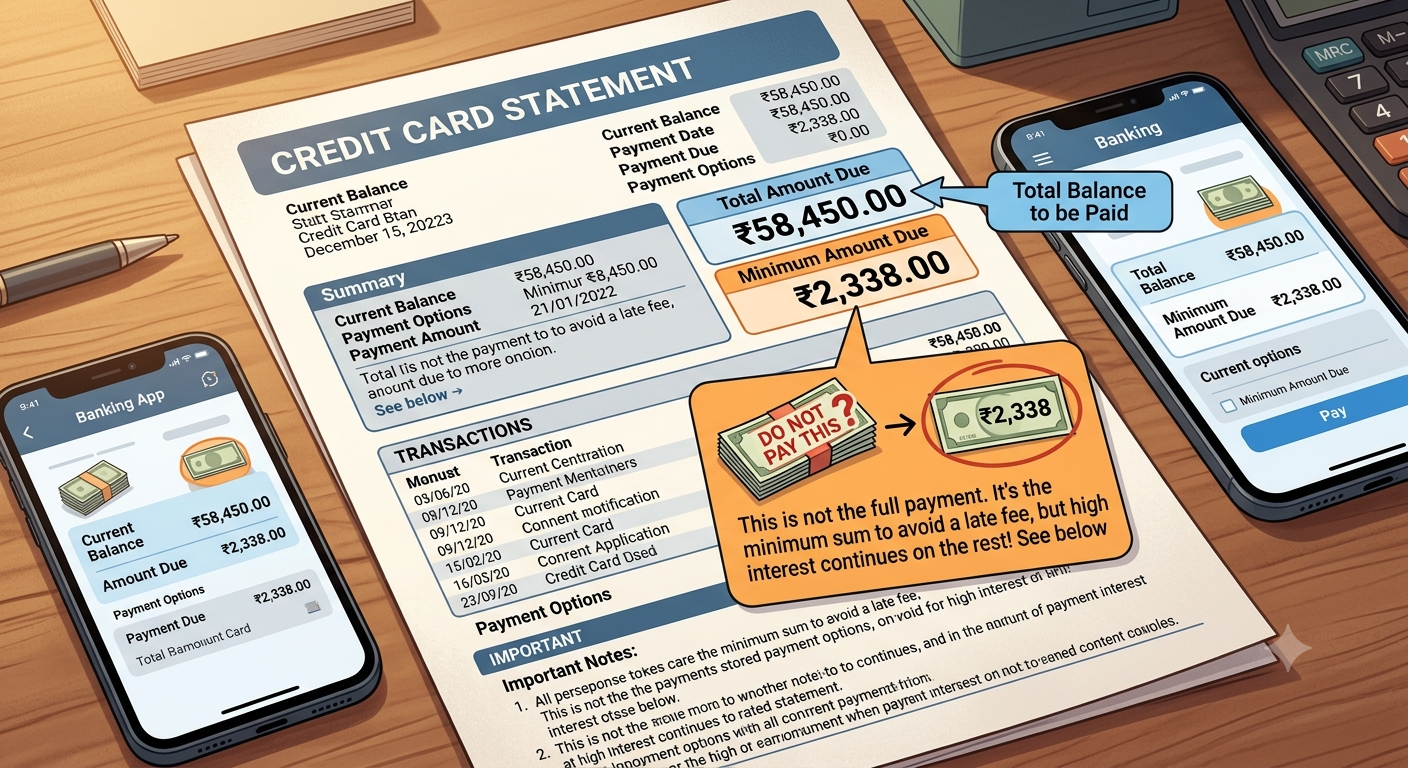

What Does Minimum Amount Due Mean on a Credit Card?

Every credit card statement shows 2 numbers. Most people know one. The other one can have a significant impact on long-term repayment costs.

The first number is the total amount due everything you owe right now. Principal, interest, fees, any unpaid balance from last month. This is the full picture.

The second number is the minimum amount due (MAD), the smallest slice you can pay by the due date without the bank marking you as a late payer or charging a penalty.

The formula for MAD was updated by the RBI effective December 1, 2022. The new rule: the minimum must be the higher of (a) 100% of all interest, fees, and taxes for that month, or (b) 5% of the total amount due. To that, the bank adds any unpaid amount from the previous month, any over-limit amount, and any EMI instalments due that cycle.

The updated formula was introduced to address situations where balances could continue growing despite minimum payments. The bank was fined ₹29.6 lakh in June 2024, HSBC, specifically for calculating MAD in a way that caused exactly that problem in some accounts.

But here is the part no statement makes obvious: paying the minimum amount due does not stop interest. It stops the penalty. The rest of your balance, everything above what you paid, carries forward and attracts interest from the very next day.

How Is the Minimum Amount Due Calculated?

Take a real example. You have ₹50,000 outstanding on your credit card. Your bank charges 3% monthly interest that is 36% per year, a typical rate for most Indian cards. Credit card interest rates in India generally range from 2.5% to 4% per month (30% to 48% per year).

The MAD calculation looks like this:

5% of ₹50,000 = ₹2,500 (principal portion)

3% interest on ₹50,000 = ₹1,500

MAD = ₹4,000

You pay ₹4,000. The remaining ₹46,000 carries forward to next month, and that ₹46,000 starts attracting 3% interest immediately.

Next month, the MAD is calculated on the new balance (₹46,000 plus the fresh interest). If you have made any new purchases, those are added too. The number only comes down slowly. And if you keep spending on the card, it may not come down at all.

This is the core problem with paying the minimum. Your monthly payment chips away at a small piece of the outstanding. But the rest keeps growing, not because you are spending, but simply because of the interest rate. The balance does not shrink the way a personal loan EMI shrinks the loan. It creeps.

FREED Expert Tip

If a large share of your income is already committed to debt repayments If your total EMIs and minimum dues already eat up more than 50% of your take-home salary, you are heading into serious debt trouble

check your actual burden using the free Debt Calculator before it gets worse. →What Happens If You Pay Only the Minimum Amount Due Every Month?

This is the information your credit card statement does not show you.

At 42% annual interest with a 5% minimum due, a ₹50,000 balance paid at minimum due only takes over 11 years to fully clear. Total cost: more than ₹1.28 lakh. That is 2.5 times what you originally spent.

Read that again. ₹50,000 spent. ₹1.28 lakh paid. And it takes over a decade.

These figures illustrate how compounding interest can affect long-term repayment costs. Researchers and finance calculators verified this repeatedly. BankBazaar's EMI logic, InvestingPro's minimum payment calculator, and basic compounding at 42% annual interest all confirm this range.

There is another cost that is harder to see. When you pay only the minimum due, you lose the interest-free grace period. Not just on the unpaid balance, but on every new purchase you make that month too. Whatever you buy on the card in the same cycle, interest starts running from the date of that transaction. Not from the due date. From the day of purchase.

So even if you are careful with new spending, the interest clock is already running on those amounts the moment you tap the card.

Only 40% of Indian credit card holders repay their full outstanding every month, according to an RBI report cited in Business Standard, July 2025. The other 60% are carrying a balance and paying for it at 36–42% per year. (https://www.business-standard.com/finance/personal-finance/paying-only-minimum-due-on-your-credit-card-you-could-be-in-a-debt-trap-125073101745_1.html )

Minimum due is primarily designed to help avoid late-payment penalties, nothing more.

What Is the Difference Between Minimum Amount Due and Total Amount Due?

These two numbers look similar on the statement. They are completely different things.

The total amount due is everything you owe this billing cycle: principal, interest, fees, and any balance you carried forward from last month. Paying this in full means you owe the bank nothing. No interest applies. Your grace period on new purchases is fully intact.

The minimum amount due is the floor. The smallest payment the bank will accept without flagging you as a late payer. It protects your account status. It does not protect your wallet.

Pay the total due: zero interest, grace period preserved, credit utilisation (the share of your credit limit you are using) drops.

Pay the minimum due: interest charged on the full remaining balance from the date of each purchase, grace period gone, utilisation stays high.

The difference is not a matter of degree. It is a structural fork in the road. The long-term cost difference between these two approaches can be substantial.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

Does Paying the Minimum Amount Due Affect Your CIBIL Score?

The honest answer: not immediately and then, over time, significantly.

Paying the minimum on time does not trigger a late payment mark on your CIBIL report. So month to month, your score looks fine.

But credit bureaus look at more than payment history. One of the key signals they track is credit utilisation, the percentage of your total credit limit you are currently using. If your credit limit is ₹1 lakh and your outstanding balance is consistently ₹70,000–₹80,000, your utilisation ratio is 70–80%. Higher credit utilisation may affect how lenders assess creditworthiness. Even if you are making every payment on time.

So this is possible: your minimum due goes in every month without fail, your account stays active, and your credit profile may be affected over time. because the outstanding never really comes down.

The real risk sits one step further down the road. If minimum payments themselves become difficult to make, if the ₹4,000 or ₹5,000 due every month starts to feel impossible, that is where the CIBIL damage accelerates. Miss a payment, and a late mark can appear on your report at the next reporting cycle. Currently fortnightly, moving to weekly from July 2026 as per RBI's updated credit reporting rules. [RBI CIC Amendment Directions 2025 - https://poonawallafincorp.com/blogs/credit-score/why-a-missed-payment-could-hurt-your-score-quicker]

Go past 90 days overdue, and the loan is classified as an NPA (loan marked as bad by the bank). That classification shows on your credit report and significantly reduces your score.

Paying the minimum keeps you in the game. It does not mean you are winning it.

When Does the Minimum Amount Due Trap Become a Debt Crisis?

Your EMI has slipped one in the last 2 months, maybe 2. Recovery calls have started. The credit card minimum due itself feels like a large amount now.

That may be a sign the debt is becoming harder to manage. And it comes faster than most people expect.

It starts quietly. One tight month, minimum paid instead of full. The balance carries forward. A few more purchases go on the card because cash is short. The minimum due climbs because it is a percentage of a growing balance. Income does not change. The gap widens.

For many people, the same cycle happens across multiple cards at once. Credit card 1 in minimum-only mode. Credit card 2 also. Personal loan EMI running alongside. By the time recovery calls start, the combined monthly obligation has already crossed 60–70% of income.

Credit card delinquencies in the 91–360 days overdue category rose 44.3% year-on-year from ₹23,475.6 crore in March 2024 to ₹33,886.5 crore in March 2025, according to CRIF High Mark data. This is not a small number of people in unusual situations. This is a large and growing group.

At this point, borrowing a personal loan to pay off the credit card balance is almost always the wrong move. The personal loan adds a new fixed EMI on top of an already strained income. If the interest rate on the personal loan is not clearly lower than the card rate and the income cannot genuinely support the new EMI, the situation gets worse, not better. Stop and assess first.

Credit card interest rates exceed 36% per year for most Indian issuers. Among all retail credit products available in India, this is among the highest.

What Are Your Options When Credit Card Dues Are Out of Control?

Options in order start with the least disruptive.

1. Pay more than the minimum. Even ₹500 or ₹1,000 above the minimum each month makes a real difference to the total interest you pay and how long it takes to clear the balance. The minimum due protects your account. Every rupee above it reduces your actual debt.

2. Call the bank before missing a payment. Most banks have a hardship plan (the bank's help plan for difficult cases) that can reduce the interest rate or restructure the repayment schedule for customers facing genuine financial difficulty. Banks are more flexible when you reach out first before the account shows a missed payment, not after.

3. Balance transfer. Move the outstanding balance to another card or product with a lower interest rate. This can work, but only when 2 conditions are met: the new rate is genuinely and significantly lower than your current card rate, and you stop using the old card entirely. A balance transfer that keeps the old spending running alongside the new loan does not solve the problem.

4. Personal loan to clear card dues. This can make sense if the personal loan interest rate is clearly lower than the card rate (most personal loans are 12–24%, far below the 36–42% on credit cards) AND if you can realistically manage the EMI without straining your income further. Be honest with yourself about the second condition.

5. Loan settlement (one-time settlement, or OTS). This is for people who are genuinely unable to repay even the reduced amounts above. Settlement is the last resort. FREED's debt settlement programme helps borrowers in this situation negotiate with banks to bring down the total outstanding. Fees only on successful settlement.

How FREED Helps When Credit Card Debt Has Gone Beyond the Minimum Due

Settlement is not something a borrower chooses out of preference. Banks and financial companies only consider it when you are in genuine financial difficulty and truly unable to repay the full amount. It is a last resort, not a shortcut.

For people who have moved past "tight but managing" into genuine inability to pay even the minimum, FREED's loan settlement programme is one structured option worth understanding.

Here is what settlement means in plain terms: you pay a reduced amount to the bank total outstanding can be brought down by up to 50%* across enrolled unsecured loans, and the account is marked as settled. The bank stops pursuing the remaining amount. The debt is resolved.

The tradeoff is real, and FREED will not hide it from you. Your CIBIL score drops by approximately 75–150 points at the point of settlement. The "Settled" mark on your CIBIL report stays for up to 7 years. Future lenders will see it.

But compare that against the alternative: defaults compounding at 36–42% annually; a growing outstanding that becomes harder to resolve the longer it sits, and the same "Settled" or NPA mark eventually appearing on CIBIL anyway, often after more months of stress.

What FREED does: supports borrowers through communication and settlement discussions with lenders, helps put your documents together, drafts the settlement letter correctly, and guides the process from enrollment to settlement. Fees are charged only on successful settlement.

If you are in that situation, the first step is understanding exactly where you stand, not signing anything. FREED counsellors offer that assessment free, with no commitment required.

Talk to a FREED Counsellor: Free, No Commitment

20 minutes. A real answer on where you stand.

Book My Free Call → freed.care/contactTips for Getting Out of the Minimum Amount Due Cycle

Concrete steps, not generic advice.

Set auto-debit to the total amount due, not the minimum. Your bank's app lets you choose which amount gets auto-debited each month. Change this setting once, and you remove the decision entirely.

If full payment is not possible right now, pay as much above the minimum as you can. Even ₹1,000 extra per month cuts months off your repayment time and saves real interest. The math favours every extra rupee.

Stop using the card for new purchases until the balance is cleared. Every new transaction you put on a card with an existing balance resets the interest clock on that amount from the purchase date. Pause the card until the outstanding is zero.

Call the bank before missing a payment, not after. Once a payment is missed, your leverage to ask for a hardship plan shrinks. Banks respond better to a borrower who calls proactively.

Keep credit utilisation under 30% of your limit even after you have cleared the balance. Stay well below the limit to support a healthier credit profile over time.

Check your CIBIL report every 3 months. The RBI mandates one free credit report per year through the credit bureaus. Use it. Errors on your report can slow recovery; catch them early.

If minimum payments themselves have become unmanageable, a free FREED counsellor call is the first step to understanding your real options. No commitment. No obligation. Just a clear picture of where you stand.

Minimum Amount Due vs Total Amount Due: What Each Choice Means

What You Pay | Late Fee Avoided? | Interest Charged? | Grace Period on New Purchases? | Debt Reduces? | CIBIL Impact |

Total Amount Due (full payment) | Yes | No | Yes, full grace period | Yes, fully | Positive shows responsible repayment |

More than Minimum, Less than Total | Yes | Yes, on unpaid balance | No interest from purchase date | Slowly | Neutral to mildly negative |

Minimum Amount Due only | Yes | Yes, on full remaining balance | No interest from purchase date | Very slowly or not at all | Neutral short-term; negative if utilisation stays high |

Nothing (missed payment) | No late fee applies | Yes, on full balance | No | No balance grows | Negative late payment mark after 3 days |

*Credit card interest rates and minimum due calculations vary by issuer. Verify your specific rate and formula with your bank. FREED is not a lender and does not guarantee outcomes.

About FREED

FREED is India's first debt relief company. Founded in 2020, headquartered in Gurugram, FREED helps people enrolled in its programme negotiate loan settlements on unsecured debt credit cards, personal loans, BNPL, and loan apps. Fees are charged only on successful settlement. FREED does not handle secured loans such as home loans, car loans, or gold loans.

Over 20,000+ accounts settled. ₹1,000 crore+ in debt enrolled.

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions