Low CIBIL Score and Need a Personal Loan? How to Actually Choose Between Your Options

When your CIBIL score is below 700, you usually have more than one route that could say yes: an NBFC, a fintech app, a secured loan, or a co-applicant route. The mistake most people make is comparing only the approval odds. The actual decision should weigh total cost, repayment risk, and whether a new loan is even the right tool for the underlying problem.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

Getting approved is not the hard part when you have a low CIBIL score. Several lenders will say yes. The hard part is picking the option that doesn't make your situation worse a year from now.

The same loan amount can cost very differently depending on the route; an NBFC loan and a gold loan for the same ₹1 lakh can differ by tens of thousands of rupees in total repayment.

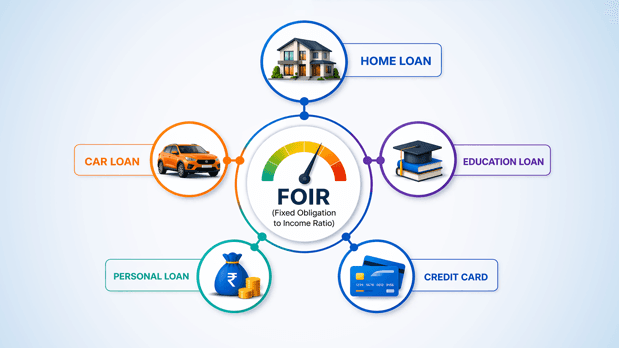

FOIR (Fixed Obligations to Income Ratio) matters more than the CIBIL score itself once you're below 700, since lenders are underwriting your ability to repay, not just your record.

A loan that solves today's cash crunch but pushes your FOIR past 50% is not a solution. It's a deferred problem with interest attached.

If existing debt is driving your search for another loan, it may be worth exploring other options before taking on new borrowing.

Why "Will I Get Approved?" Is the Wrong First Question

Most low-CIBIL content answers one question: which lender will say yes? That's the easy part. NBFCs, fintech platforms, gold loans, and co-applicant routes are among those that will likely approve you even with a score below 650.

The question that actually matters is different: of the options that say yes, which one leaves you better off six months from now?

That depends on three things: the approval decision alone won't tell you the real total cost of the loan (not just the EMI), what happens if your income takes a hit mid-tenure, and whether your FOIR after this loan still leaves you breathing room. A loan you can technically repay on paper today can become unmanageable the moment one EMI is missed somewhere else in your finances.

Comparing the Real Cost: Same ₹1 Lakh, Different Routes

Here's what most comparisons skip: the actual repayment number, side by side, for the same loan amount.

Route | Typical Rate | ₹1 Lakh, 12 Months: Total Interest | What Drives the Cost |

Gold loan | 8.05%–9.30% p.a. | ₹4,300–₹5,000 approx. | Asset-backed, lowest risk to the lender |

Loan against FD | FD rate + 1–2% | ₹6,000–₹8,000 approx. | Asset-backed, only if FD exists |

NBFC personal loan (below 650 CIBIL) | 24%–36% p.a. | ₹13,000–₹21,000 approx. | Unsecured, income-assessed |

Co-applicant loan | Tied to the co-applicant's score | Varies, often close to standard bank rates | Combined risk profile |

P2P lending | Varies widely | Often higher than NBFC | Less standardised, individual lenders |

Figures are indicative and based on reducing-balance calculations. Actual rates depend on your lender's assessment. FREED is not a loan provider and does not guarantee any outcome.

The gap between the cheapest and most expensive route for the identical ₹1 lakh can be ₹15,000 or more in interest alone. That's the number worth comparing, not just whether you'll be approved.

The FOIR Check Most People Skip Before Applying

FOIR (Fixed Obligations to Income Ratio) is what tells you whether a loan is actually affordable, not whether a lender will approve it. The two are different questions, and a low CIBIL score makes this gap more dangerous because the lenders most likely to approve you are also pricing in the highest risk through interest rates, rather than affordability checks.

Add every fixed monthly obligation you currently carry, personal loans, credit cards, BNPL, vehicle EMIs, and divide by your take-home salary. Many lenders consider FOIR as one of the factors while assessing loan affordability. The acceptable range varies by lender.

If adding the new EMI pushes you past that line, the loan may become difficult to manage, even if it is approved. This is worth working out properly before applying anywhere, rather than roughly estimating.

FREED Expert Tip

Run your FOIR with the new EMI included before you apply anywhere, not after. If a new EMI significantly increases your monthly repayment burden, it may be worth reviewing your options before applying.

Talk to a FREED ExpertAre You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

When a Co-Applicant or Secured Route Beats an NBFC Loan

Two routes are consistently overlooked by people focused solely on approval speed.

- 1

Adding a co-applicant with a stronger score

can move you from NBFC-only territory to standard bank rates, sometimes resulting in a 15 to 20 percentage-point difference in the interest rate. The trade-off: your co-applicant's CIBIL score is now tied to your repayment. If you miss a payment, it affects them too, and they can be pursued for recovery. This only works if they fully understand and accept

- 2

A loan against an existing FD or gold

sidesteps the CIBIL conversation almost entirely, because the bank has an asset to recover, not a credit history to trust. If you have idle gold or an FD sitting unused, this may be one of the more affordable options, depending on the lender and your circumstances. The trade-off is real: the asset is at risk if you default. FREED does

What the Law Says

Under RBI's Digital Lending Directions, 2025, all digital lending apps must be linked to an RBI-regulated bank or NBFC, either directly or through a lending service provider acting on that entity's behalf. Before borrowing through a digital lending app, check whether it is associated with an RBI-regulated bank or NBFC. You can check the RBI's Digital Lending Apps directory to verify an app's association before borrowing.

Check Your OptionsWhen the Comparison Doesn't Matter, Because a New Loan Is the Wrong Move

All of the comparisons above assume a new loan is the right tool. Sometimes it isn't, and no amount of rate-shopping fixes that.

- If existing EMIs already account for a large share of your take-home salary, a new loan, even at the cheapest rate on this page, adds a new fixed commitment on top of a position that's already stretched. The math doesn't improve by finding a marginally better rate.

- If the new loan exists to repay an old one, you may only be shifting the debt instead of reducing your overall repayment burden. Usually at a higher cost, given the rates available at a low score.

- If your income is irregular, every option in this comparison assumes a fixed monthly EMI you can reliably meet. An unpredictable income and a fixed obligation are a bad combination, regardless of which lender you choose.

In any of these cases, the better next step is usually one of: talking to your existing bank about restructuring or a moratorium, looking at consolidation if your FOIR and score still qualify you for it, or, if repayment has genuinely become impossible, understanding whether settlement is realistic for unsecured debt.

Already Juggling Multiple EMIs?

See whether consolidation could be a suitable option for your situation.

Check If I Qualify for ConsolidationFREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions