HDFC Debt Consolidation Loan: Eligibility, Process, and What Comes Next

Managing multiple loan EMIs every month can stretch your finances thin. An HDFC debt consolidation loan taken as a personal loan lets you combine all your outstanding debts into a single, lower-interest EMI. This guide covers HDFC's eligibility criteria, the step-by-step application process, what happens after approval, and what to do if the bank route isn't available to you.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

KEY TAKEAWAYS

An HDFC debt consolidation loan works through a personal loan starting at 9.99% p.a., up to ₹40 lakh, repayable over 12 to 60 months

Eligibility requires age 21 to 60, minimum ₹25,000 net monthly income, 2+ years of work experience (min 1 year with current employer), and a CIBIL score of 720 or above

HDFC does not have a product called "debt consolidation loan", the personal loan is what borrowers use for this purpose; your CIBIL score and income decide the interest rate you get

If a large share of your monthly income is already going toward loan repayments, HDFC's approval chances fall sharply, and a bank loan alone may not fix the real problem

FREED's Debt Consolidation Program is for borrowers who are still paying their EMIs but are stretched thin. FREED matches you to a lending partner, which consolidates all your eligible unsecured loans into one lower EMI, without a 'Settled' status being reported on the credit report.

What Is an HDFC Debt Consolidation Loan and How Does It Work?

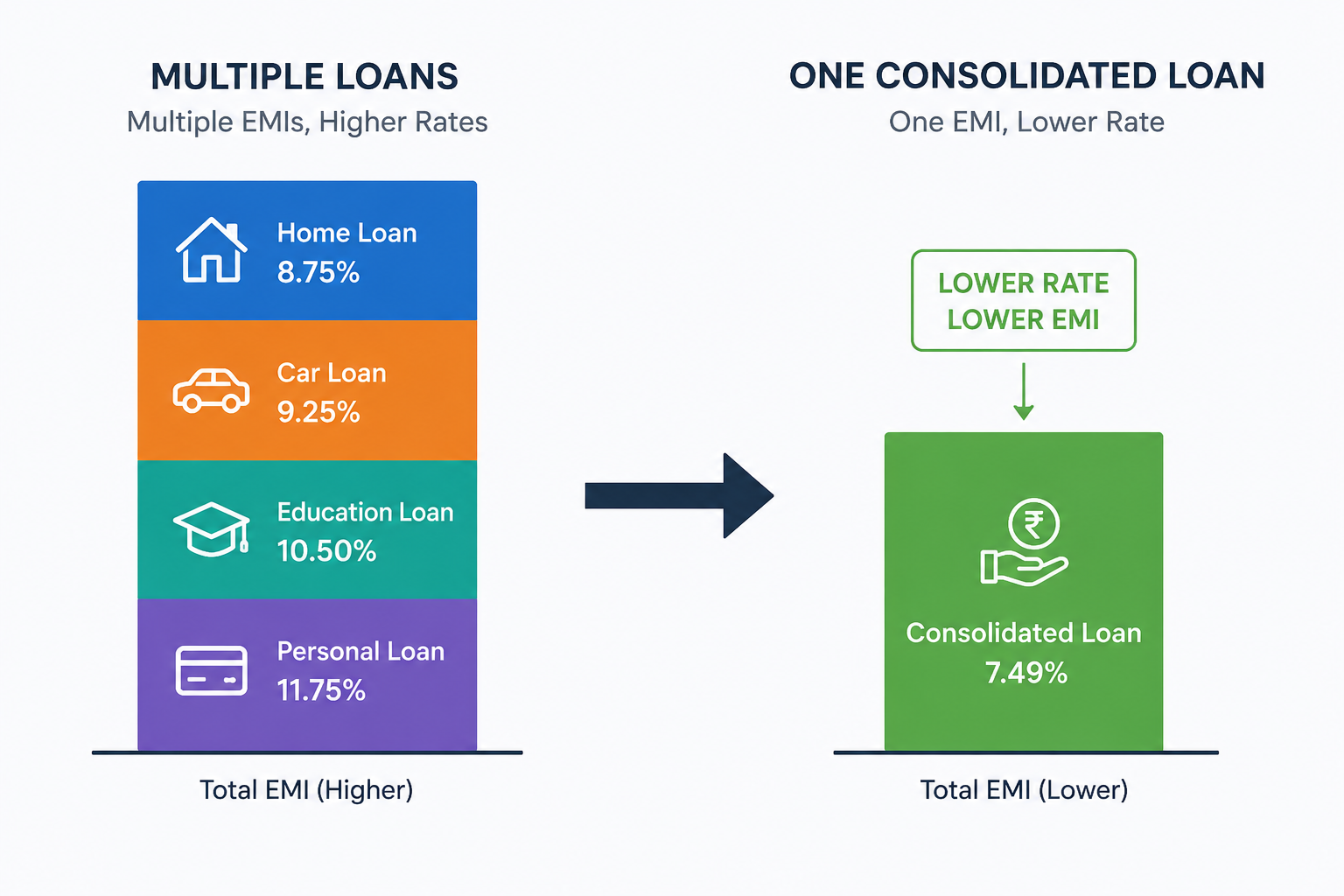

HDFC Bank doesn't have a product labelled "debt consolidation loan." What it offers is a personal loan. Borrowers use that personal loan to pay off all their existing debts in one go: credit cards, other personal loans, BNPL (buy now pay later) dues. After that, only one loan remains. One EMI. One due date. One bank.

This works because HDFC's personal loan is multipurpose. The bank disburses the money into your account. You use it to close each existing debt individually. What's left is a single repayment schedule at a fixed interest rate.

The numbers can make sense. Credit card interest in India typically runs between 36% and 42% per year. HDFC personal loan rates start at 9.99% p.a. If you're carrying credit card dues at 40% and you consolidate into a personal loan at even 14%, the monthly interest saving is real.

The loan amount goes up to ₹40 lakh and can be repaid over 12 to 60 months .

The key thing to understand: this doesn't reduce what you owe. The total debt amount stays the same. What changes is the structure. Lower rate, single payment, fixed end date.

If the bank route isn't available to you, FREED has a path built for exactly this situation. India's first debt relief company, FREED has been helping borrowers since 2020, and its Debt Consolidation Program works through a lending partner network instead of a direct bank application.

Stretched across multiple EMIs every month?

Find out if one lower EMI is possible for you.

Check If I Qualify for ConsolidationWhy Do People End Up Needing Debt Consolidation?

Most borrowers with multiple EMIs didn't plan for things to get complicated. A medical bill one year, a vehicle loan the next, a credit card for home repairs. Each one made sense at the time. Salaries didn't always keep pace.

Over time, three or four EMIs are leaving the account every month, to different banks, on different dates, at different interest rates. Miss one because your salary arrived late, and it can affect your credit profile.

When total EMIs take up almost all of your take-home salary, there isn't much left for rent, groceries, and transport. People start using one credit card to pay another. That's when the structure itself becomes the problem, not the amount.

Multiple active loans also mean multiple banks to track. Different customer care lines. Different interest cycles. Different foreclosure rules if you ever want to close one early. It adds up to a lot of maintenance for something that should run quietly in the background.

Loan consolidation addresses the structure problem. It doesn't erase loans. It reorganises repayment so you're managing one thing instead of four.

You don't have to figure this out alone. FREED has helped over 20,000 borrowers work through similar situations, step by step

Are You Eligible for an HDFC Debt Consolidation Loan?

Criterion | Requirement |

Age | 21 to 60 years |

Employment type | Salaried only: private company, PSU, central or state government |

Work experience | Minimum 2 years total; at least 1 year with current employer |

Monthly income | Minimum ₹25,000 net take-home |

CIBIL score | 720+ for clean approval; 760+ for preferential rates |

Existing EMI load | Bank checks FOIR (how much of your salary already goes to EMIs). If this is above 40 to 50%, approval chances drop |

One important note for self-employed borrowers: HDFC's personal loan is for salaried individuals only. If you're self-employed, you'd need to apply for a business loan instead. The consolidation route through HDFC personal loan is not available to you.

An existing HDFC salary account or prior relationship with the bank can speed up approval. Pre-approved customers can receive funds in as little as 10 seconds. Other applicants typically wait up to 4 working days after submitting documents.

FREED Expert Tip

Before applying to HDFC, pull your CIBIL report and check for errors. Even an incorrectly reported DPD may affect how lenders assess your application. Even a single incorrectly marked DPD (Days Past Due) can push your score below the approval threshold. FREED's team can help you read your report and spot what needs fixing before you apply.

Read MoreWhat Documents Do You Need to Apply?

For pre-approved HDFC customers: In many cases, no documents are needed at all. The process runs on Aadhaar-based eKYC (digital identity verification). Funds can arrive in seconds after acceptance.

For other applicants, keep these ready:

- Identity proof: Aadhaar card or PAN card

- Address proof: Aadhaar, passport, or driving licence

- Income proof: Last 3 months' salary slips

- Tax proof: Latest Form 16 or ITR

- Bank statements: Last 6 months (the account where salary is credited)

- Employment proof: Appointment letter or employer certificate, if required by the branch

HDFC's digital application process accepts scanned copies. You don't need to visit a branch unless your situation requires it. The documents list above applies to first-time or non-pre-approved applicants.

How to Apply for an HDFC Debt Consolidation Loan: Step by Step

- 1

Calculate Your Total Debt Load

Add up the outstanding balance on every active loan and credit card. This total is the amount your consolidation loan needs to cover.

- 2

Check Your CIBIL Score First

A lower score may reduce approval chances or affect pricing. Knowing where you stand before applying avoids unnecessary credit applications.

- 3

Use HDFC's EMI Calculator

Go to hdfcbank.com and enter your total debt amount, expected tenure, and an estimated interest rate. Compare the projected single EMI against your current combined EMI total. If the new number is meaningfully lower, the math works.

- 4

Apply Online or Visit a Branch

Existing HDFC customers can apply through NetBanking. New customers can apply at hdfcbank.com or walk into the nearest HDFC branch. Pre-approved customers see their offer immediately after login.

- 5

Submit KYC and Income Documents

Upload Aadhaar, PAN, salary slips, and bank statements. Pre-approved customers may need no documents at all. The process is entirely digital.

- 6

Review the Loan Offer Carefully

When the offer arrives, check the interest rate, processing fee, and the total repayment amount, not just the EMI. Confirm the loan amount is enough to close all existing debts.

- 7

Accept and Use Funds to Close Existing Loans

Once the amount is disbursed, use it to pay off each existing loan or credit card in full. Collect a closure letter and NOC (clearance letter) from each bank. Keep these documents safely.

- 8

Set Up Auto-Debit for the New EMI

Schedule the HDFC EMI auto-debit (automatic bank payment instruction) 2 to 3 days before the due date. This protects against payment failures.

What Interest Rate Will You Get and What Does It Actually Cost?

The rate on your HDFC personal loan is not fixed for everyone. It moves with your credit profile. A borrower with a 780 CIBIL score and a stable corporate salary will get a different rate than someone with a 720 score at a smaller company. The published range is 9.99% to 24% p.a.

Beyond the interest rate, here are the costs people miss:

- Processing fee: Up to ₹6,500. This is deducted from the disbursed amount upfront.

- GST on the processing fee: 18% on the processing fee amount. Factor this in.

- Foreclosure charges on existing loans: When you close your old loans early using the consolidation funds, those banks may charge a foreclosure fee, typically 1% to 5% of the remaining outstanding. This cost comes from your pocket before you even start with the new loan.

- Credit insurance add-ons: HDFC offers personal accident cover and critical illness cover bundled with the loan. These are optional but sometimes presented as part of the standard offer. Read the offer letter to separate what you're actually agreeing to.

The consolidation only saves money if your new interest rate is meaningfully lower than the weighted average rate on all your current debts. Run the numbers before you accept.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

When an HDFC Loan Isn't Enough: What Happens If You Don't Qualify?

Not every borrower who needs debt consolidation will qualify for an HDFC personal loan. Here are the common reasons for rejection:

- CIBIL score is typically below 720 (though cutoffs vary by applicant profile and HDFC's internal criteria)

- FOIR (the share of your salary already going to EMIs) is above 40 to 50%, making it hard for any bank to approve another loan.

- You're self-employed. HDFC personal loans are for salaried individuals only.

- Your total debt load exceeds HDFC's maximum loan amount

If any of these applies to you, you're not out of options. There are steps worth taking.

Balance transfer works if you have a single expensive loan and your CIBIL is around 700 or above. You move that loan to a bank offering a lower interest rate. The EMI drops. It doesn't combine multiple loans, but it reduces the cost on the most expensive one.

EMI restructuring with your current bank is worth asking about. Some banks will agree to extend your loan tenure, which brings the monthly EMI down, if you request this before your repayment starts slipping.

FREED's Loan Consolidation Plan is built specifically for borrowers who are still paying their EMIs but can't get a new bank loan approved because their FOIR is too high or their credit profile doesn't clear the bank's threshold. FREED matches you to a lending partner from its network. That lending partner disburses a new consolidated loan that pays off all your eligible unsecured loans: personal loans, credit cards, BNPL dues, payday loans. You're left with one EMI, one due date, and a lower monthly outgo. This is different from settlement, which results in a 'Settled' status on the credit report.

FREED handles the matching, the coordination with the lending partner, and the follow-through until every existing loan is closed. You don't need to approach anyone directly.

Multiple EMIs making your salary disappear?

Find out if debt consolidation can bring them down to one lower amount.

Check If I Qualify for ConsolidationDebt Consolidation vs Balance Transfer vs FREED's Program: What's the Difference?

Factor | HDFC Personal Loan Consolidation | Balance Transfer | FREED Loan Consolidation Plan |

Best for | Good CIBIL, multiple unsecured debts | Single loan, rate improvement | Over-leveraged, may not qualify for a new bank loan |

CIBIL impact | No negative impact | No negative impact | No negative impact. Score improves. |

Eligibility | CIBIL 720+, salaried, min ₹25,000 income | CIBIL ~700+, active loan | Assessed by FREED's team |

Process | Self-serve via bank | Bank-initiated | FREED handles end to end |

What it covers | Any use; borrower closes old loans | One loan, one bank | Multiple unsecured loans through lending partner |

Speed | 10 seconds (pre-approved) to 4 days | 7 to 15 days typically | Assessed within days |

FREED is not affiliated with any bank and handles unsecured loans only. Eligibility for each option depends on individual financial profile.

No single option works for everyone. The right one depends on your CIBIL score, your income, how many loans you have, and whether your repayments are still current. Speak to FREED's team when you're ready. One conversation is enough to know which path is actually open to you.

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions