Loans for poor credit score: what they cost and when to avoid them

Loans for poor credit score are personal loans, NBFC loans, or secured loans offered to borrowers with a low credit history, usually at a higher interest rate to offset the lender's risk. They exist and are legal, but the real cost is often much higher than it first looks.

Mohit Juneja

Reviewed by FREED India, Debt Resolution Specialists

KEY TAKEAWAYS

Loans for poor credit are generally designed for borrowers with weaker credit profiles, although eligibility varies by lender.

New poor-credit loan to cover old EMIs deepens debt, directionally correct, standard debt-spiral pattern

Secured loans against gold or an FD carry lower interest since collateral reduces the lender's risk.

Taking a new poor credit loan to cover old EMIs often deepens the debt instead of solving it.

FREED helps assess whether a new loan, consolidation, or settlement is the right next step before you sign anything.

What are loans for poor credit score?

Many banks generally apply stricter eligibility criteria for applicants with weaker credit profiles, although lending decisions vary by institution. That's not the end of the road though. NBFCs, digital lenders, and secured-loan options still work with borrowers in this band, just at a cost that reflects the added risk.

It helps to be honest about one thing upfront: getting approved is not the same as being able to afford it. A lender saying yes tells you they're willing to take the risk at their price. It doesn't tell you whether that price fits your monthly budget, or whether it solves the problem you actually have.

Most borrowers land in this band the same way, a few EMIs slipped over recent months, a credit card balance that kept rolling, or high utilisation that built up over time. None of that makes someone a bad borrower. It just means the score reflects some financial strain, and lenders price for that strain rather than refuse outright.

Not sure a new loan is the right move?

See your actual options assessed before you sign anything.

Get My Options AssessedWhy do some lenders approve loans despite a poor credit score?

Banks tend to rely almost entirely on the score itself, and a sub-650 number usually triggers an automatic rejection. NBFCs and fintech lenders work differently. They look at the score too, but they weigh it alongside other signals, income stability, employment type, and how the applicant's bank account actually behaves month to month.

This is what's called risk-based pricing. A lender willing to take on a riskier borrower charges more for it, the same way insurance costs more for a driver with a rough record. The higher rate isn't a penalty tacked on out of spite, it's how the lender balances the chance that some borrowers in this band won't repay in full.

That also means two people with the same score can get different offers. Someone with a steady salary and a clean bank statement, even at a lower score, may get better terms than someone whose income looks inconsistent on paper.

Signs a poor credit loan could cost you more than it helps

A few patterns are worth watching for before you sign anything.

Approval that feels too fast for your score band is one. If a lender approves you instantly, with almost no questions about income or repayment capacity, that speed is usually paired with a rate high enough to justify skipping the checks.

No written terms before disbursal is another. If the money lands in your account before you've seen a clear breakup of the interest rate, tenure, and every fee, you're signing blind, and that's a real problem regardless of how urgently you need the funds.

A very high effective borrowing cost, after including fees and charges, should be carefully evaluated before accepting the loan. The advertised rate and the real cost can look very different once everything is added up.

Being asked, directly or indirectly, to take this loan to repay another loan is the clearest warning sign of all. That's rarely a fix. It's usually just moving the same debt to a more expensive lender.

What the Law Says

Under RBI's Fair Practices Code, every lender must disclose the annualised interest rate and all charges in writing before you sign a loan agreement.

Check Your Credit InsightHow to apply for a loan with a poor credit score

Check your credit report first. Before applying anywhere, pull your own CIBIL report and look for errors, an old settled account showing as active, a payment marked late that you actually made on time. Correcting inaccurate credit-report information helps ensure lenders assess accurate credit information.

Decide secured versus unsecured based on what you can actually pledge. If you have gold, a fixed deposit, or another asset you're comfortable putting up as collateral, a secured loan will almost always cost less than an unsecured one at this score band.

Compare the total repayment cost, not just the EMI. A lower EMI over a longer tenure can end up costing more overall. Ask for the full repayment figure across the entire loan term before comparing two offers.

Read the agreement in full before signing. Every fee, every penalty clause, every condition on prepayment should be visible and understood, not buried in fine print you skim past.

Avoid applying to several lenders in a short window. Each formal loan application creates a hard enquiry that future lenders may consider during credit assessments.

FREED Expert Tip

Before signing any poor credit loan, calculate the total repayment over the full tenure, not just the monthly EMI. The real cost hides there.

See If Consolidation Fits You BetterWhat are your real options with a poor credit score?

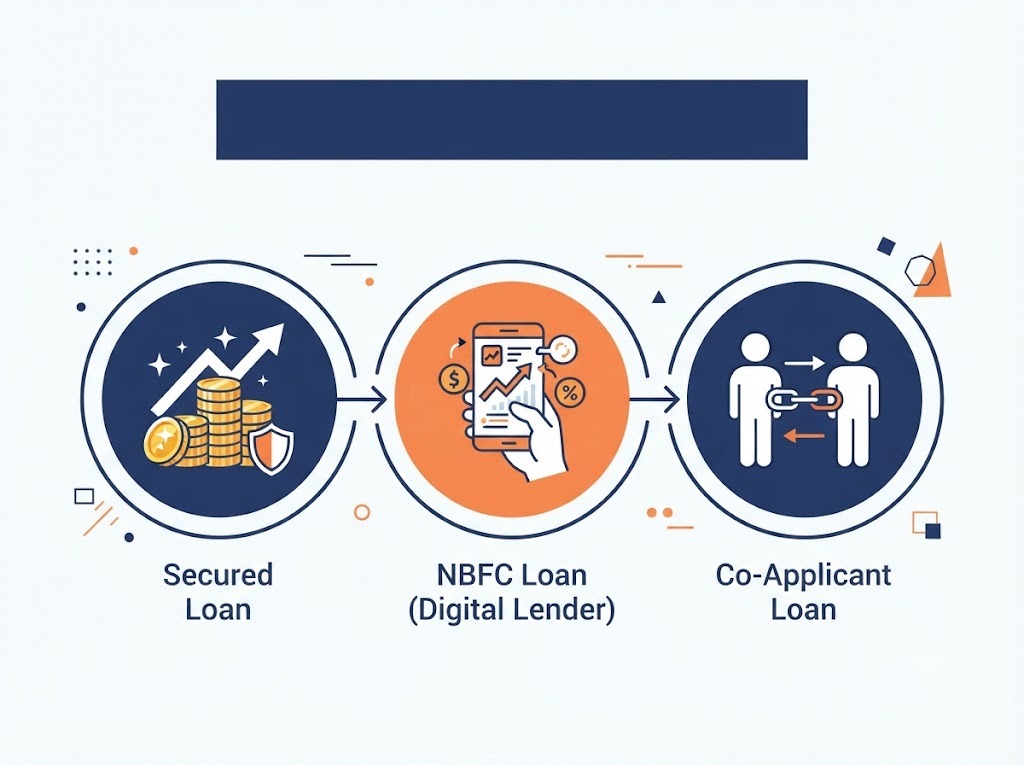

Loans for a Poor Credit Score: Your Real Options

Option | Typical interest range | Needs collateral | Best fit |

Secured loan (gold or FD) | 9% to 14% | Yes | Borrower has an asset to pledge |

NBFC or digital unsecured loan | 15% to 30% | No | Urgent need, no collateral, steady income |

Co-applicant or guarantor loan | Close to standard rates | No | Family member with a good score willing to co-sign |

FREED Debt Consolidation Program | Existing rates replaced with one lower EMI | No | Still paying but juggling multiple EMIs |

FREED Debt Resolution Program | Not a new loan, a settlement of existing debt | No | Genuinely unable to repay existing debt |

A secured loan is usually the cheapest route if you have something to pledge, but it puts that asset at risk if repayment slips. An NBFC or digital loan skips the collateral requirement entirely, at the cost of a much higher rate. Adding a co-applicant with a stronger score can bring the rate close to what a good-credit borrower would get, if you have someone in your life willing to take that on with you. The last two rows aren't new loans at all, and that distinction matters more than it might look on a table. Consolidation and settlement address the debt you already have, rather than adding to it.

FREED is not a Loan Provider. Rates shown are indicative and vary by lender and profile. Please verify current rates directly with the bank or NBFC.

When a new loan is not the right move

The honest answer depends on why your score dropped in the first place, and that's the part most poor-credit-loan content skips entirely.

If the score is low because you're juggling several EMIs that you're still current on, just stretched thin managing all of them, the better move is usually consolidating those into one loan with a single lower EMI, not adding another loan on top. A new loan at a poor-credit rate rarely helps in this situation. It usually just adds one more due date to an already crowded month.

If the score dropped because of missed payments or an actual default, a new high-interest loan usually makes the situation worse, not better. At that point, the debt itself has become the problem, not the absence of fresh credit. Settlement is not something a borrower chooses out of preference. Banks and financial companies only consider it when a borrower is in genuine financial difficulty and truly unable to repay the full amount, and in that specific situation, it can be the more honest path forward than borrowing your way further into it.

These are two different situations, for two different people, and the order matters. Consolidation comes first, for those still managing to pay. Settlement comes after, only when repayment in full has genuinely stopped being possible

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

How FREED helps if poor credit is blocking you from a loan you actually need

FREED's first step is figuring out what's actually causing the low score, before recommending anything at all.

Debt Consolidation may combine eligible debts into a single repayment, depending on the approved loan terms and lender assessment. FREED assesses your profile, matches you to a suitable lending partner, and handles the process end to end. The fee is success-based, charged only once the consolidation goes through.

If repayment in full has genuinely become impossible, FREED's Debt Resolution Program works differently. It's not a new loan of any kind. FREED negotiates with your existing banks to settle each loan for a reduced amount, through the SPA, a savings account you build over time and control yourself. Every settlement needs your authorisation before any payment goes out, and here too, the fee is success-based.

These are two separate paths for two separate situations, and a call with FREED's team is where that gets sorted out before you commit to either one.

Stuck with multiple EMIs and a falling score?

See if consolidation can lower your EMI.

Book My Free CallWhat helps before you take a loan with a poor credit score

Check your full CIBIL report for errors first. A wrongly reported late payment or an old settled loan showing as active can be pulling your score down without any fault of yours, and it's worth ruling that out before you assume you need a poor-credit loan at all.

Calculate the total repayment cost, not just the EMI. The number that matters is what you'll actually pay back across the full tenure, and that figure often tells a different story than the monthly instalment does.

Avoid applying to many lenders at once. A cluster of hard enquiries in a short span can push your score down right when you need it working in your favour.

Talk to FREED if the real issue is existing debt rather than needing a new loan. Sometimes what looks like a need for fresh credit is actually a signal that the current debt load needs restructuring first, and it's worth ruling that out before signing anything new.

Sources

Claim | Source |

Lenders must disclose the annualised interest rate and all charges in writing before a loan agreement is signed | RBI Fair Practices Code for lenders (rbi.org.in) |

Note: the exact poor-credit score threshold and interest-rate bands vary by lender and are not codified by a single RBI directive. These are treated as commonly cited industry figures in the body and are not included in this table for that reason.

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions