How to Remove a Written-Off Status From a Credit Report

You pulled your CIBIL report and saw a "Written-Off" mark sitting next to one of your old loans. Your score has dropped. New loan applications keep getting rejected. The good news: a Written-Off status is not permanent, and there is a clear way to get it changed. This guide walks you through exactly how.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

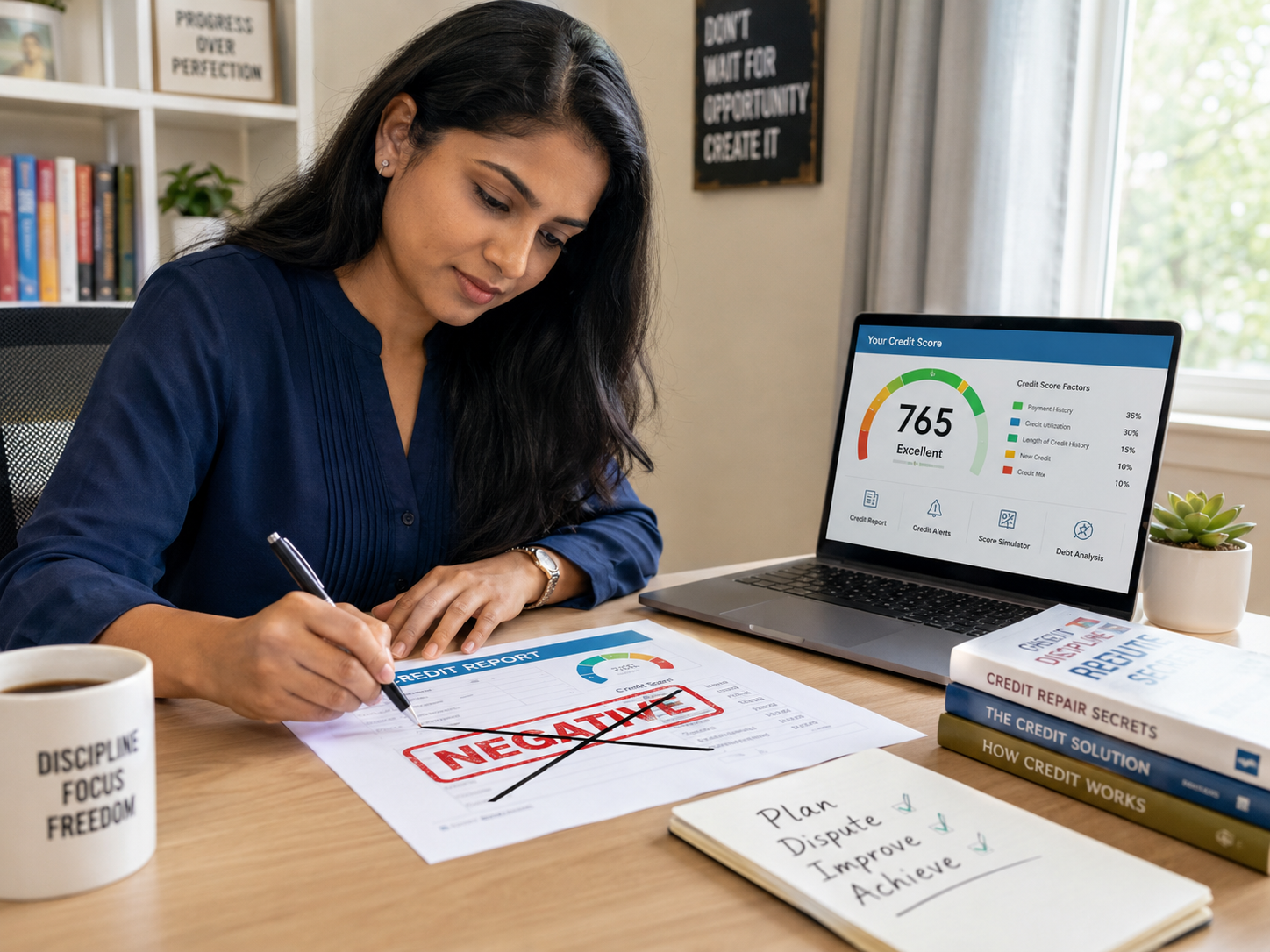

A Written-Off mark can significantly affect your CIBIL score and may remain visible on your report for up to 7 years. The debt is still owed.

A Written-Off mark can pull down your CIBIL score by 100+ points and stay on your report for up to 7 years.

The only proper way to remove the status is to settle or repay the outstanding amount, get the NOC (clearance letter from the bank), and ask the bank to update the bureau.

Bureau updates are commonly reflected within 30 to 45 days after the bank reports the change.

If the Written-Off mark is wrong, you have the right to dispute it directly with CIBIL, Experian, Equifax, or CRIF.

What Does "Written-Off" Mean on a Credit Report?

When EMIs stay unpaid for a long time, usually 180+ days after the first missed payment, the bank stops counting that loan as a live asset. It marks the loan as a loss in its internal books. This is called a write-off. It is an accounting step the bank takes. It does not mean the money is forgiven.

The debt still exists. The bank or its recovery partner can still ask you to pay it. And all 4 credit bureaus, CIBIL, Experian, Equifax, and CRIF, will show the same Written-Off status on your report, because banks report to all of them. This is most common with unsecured loans (loans with no property backing), like personal loans, credit cards, and BNPL or app loans.

Why Is a Written-Off Status Bad for Your CIBIL Score?

A Written-Off mark creates 3 specific problems for your credit profile.

Your score may fall by 100+ points the moment the status is reported. The entry stays on your report for up to 7 years from the date the account was closed or reported, even after you resolve it. And lenders may view a Written-Off mark as a sign of higher repayment risk during future applications. . Some applications may become more difficult to approve during automated screening checks.

The impact goes beyond just loans. Certain employers may review credit history during background verification processes, and a Written-Off mark can show up there too. If you have more than 1 account marked Written-Off, the combined effect on your score is heavier.

Written-Off vs Settled vs Closed: What Is the Difference?

Status | What It Means | What It Says About You | How Long It Stays |

Closed | Loan fully repaid, no dues left | You paid in full | Stays as a positive record |

Settled | You paid a reduced amount, bank accepted it as final | You resolved the loan despite difficulty | Up to 7 years |

Written-Off | Bank gave up trying to recover, marked it as a loss | Loan stayed unpaid for a long time | Up to 7 years |

Of the 3, "Closed" is the only mark that helps your score. "Settled" is recovery from a difficult situation. "Written-Off" is the hardest to live with.

Can a Written-Off Status Be Removed From a Credit Report?

Yes, but only in specific ways.

By settling or repaying the outstanding amount and having the bank update the bureau with the new status.

By disputing the entry directly with the credit bureau if the Written-Off mark is wrong, whether that is the wrong account, wrong amount, or against a loan you already paid off.

By waiting for the entry to age out. Entries can stay for up to 7 years. This is not really "removing" the mark. It is just waiting for it to drop off.

One thing worth understanding: even after you resolve the account, the status changes from "Written-Off" to "Settled" or "Closed". The historical record may still show for up to 7 years. But the impact on your score generally reduces over time as the account moves further into the past.

How to Remove a Written-Off Status From a Credit Report

Here is the step-by-step process to get a Written-Off status changed on your credit report.

- 1

Pull Your Latest Credit Report

Check the exact loan account showing Written-Off. Note the bank or NBFC name, account number, and the date of the entry.

- 2

Contact the Bank or NBFC That Holds the Loan

Ask for the current outstanding amount, including any interest and charges that have been added.

- 3

Negotiate a Repayment or Loan Settlement Plan

You can repay in full. If repaying in full is genuinely not possible due to a real financial difficulty, the bank may agree to settle for less.

- 4

Pay the Agreed Amount and Get the NOC

The NOC (clearance letter from the bank) is your written proof that the matter is resolved. Do not accept a verbal confirmation only.

- 5

Ask the Bank to Update the Credit Bureau

The bank must report the change to CIBIL, Experian, Equifax, and CRIF. Follow up in writing if needed.

- 6

Track Your Report Until the Status Changes

The updated status is commonly reflected within 30 to 45 days after reporting. Pull a fresh report to confirm the update has come through.

How Long Does It Take to Remove a Written-Off Mark?

30 to 45 days after the bank reports the change to the bureau. That is the direct answer.

Here is how that timeline actually breaks down:

- Settlement or full repayment with the bank depends on how quickly you and the bank reach an agreement.

- NOC (clearance letter) issued by the bank usually 7 to 15 days after the final payment clears.

- Bank reports the update to the bureau typically in their next monthly reporting cycle.

- Bureau updates your report 30 to 45 days from the date the bank reports the change.

Keep in mind: the historical Written-Off entry may still be visible on your report for up to 7 years. But the status will show as updated, either "Settled" or "Closed", and the impact on your score reduces over time.

FREED EXPERT TIP

Always collect the NOC (clearance letter from the bank) in writing the day after your final payment clears.The NOC helps support accurate bureau updating and future dispute resolution. Without the NOC, the bank cannot update the bureau, and the Written-Off mark stays as-is.

Get Help from FREED ExpertHow to Dispute a Wrong Written-Off Entry

Sometimes a Written-Off entry shows up by mistake. The wrong account, the wrong amount, or against a loan you already paid off. You have the right to dispute it.

- Go to the credit bureau website, CIBIL, Experian, Equifax, or CRIF, and raise a dispute online.

- Attach proof: your NOC, payment receipts, bank statement, or account closure letter.

- The bureau contacts the bank. The bureau process generally allows time for the lender to review and respond.

- If the bank confirms the entry is wrong, the bureau corrects it within 30 days of the bank's reply.

Dispute is free. Every Indian borrower has this right under RBI's credit reporting guidelines.

What the Law Says

Under the RBI's Credit Information Companies (Regulation) Act and the Credit Information Companies Rules, every credit bureau in India is required to investigate and correct disputed entries within 30 days of the complaint. Banks and NBFCs are also required to report accurate, up-to-date information about closed and settled accounts to all 4 bureaus: CIBIL, Experian, Equifax, and CRIF.

Check Your Credit ReportHow FREED Helps You Resolve a Written-Off Loan

A Written-Off mark often appears after a prolonged period of repayment difficulty. Most people have no idea where to start when they see that mark on their report. That is a real and heavy place to be in. You are not alone.

Here is what FREED does for you:

- Pull the full picture of every loan account, including any marked Written-Off, so you can see the complete situation clearly.

- Helps you prepare for the conversation with the bank or NBFC so you do not have to manage the back-and-forth alone.

- Compliant. Helps you negotiate a settlement of up to 50%* of what you owe, without you taking any new loan , without you taking any new loan.

- Review the settlement letter and NOC wording so the documentation and bureau reporting process is handled correctly.

- Tracks the bureau update with you until the new status actually reflects on your report.

If the Written-Off mark feels too heavy to handle alone, a free call with a FREED counsellor can help you see the way forward.

Don't Let a Written-Off Mark Hold Back Your Future

FREED has helped 60,000+ Indians resolve debt challenges and rebuild healthier financial habits, legally and ethically.

Get My Free Credit AssessmentWhat Is a "Written-Off" Status?

A "Written-Off" status on your credit report means the bank or NBFC has marked the loan as a loss in its own books because it could not recover the money. The debt is not cancelled. To remove the status, you must settle or repay the outstanding amount, collect the NOC (clearance letter from the bank), and ask the bank to update the credit bureau.

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions