HDFC Loan Settlement: Process, Documents, and CIBIL Impact

HDFC loan settlement happens when HDFC Bank agrees to accept a reduced lump-sum payment less than the full outstanding amount to close your personal loan or credit card account permanently. This is called an OTS (one-time settlement, paying it once, and the matter ends). It's only available to borrowers who have genuinely fallen behind on repayments. Settlement is not something a borrower chooses out of preference.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

HDFC loan settlement is possible once your account crosses 90 days of non-payment; at that point, the loan is classified as an NPA (loan marked as bad by the bank)

FREED helps borrowers settle unpaid or overdue loans at up to 50%* less, depending on their individual circumstances. Depending on the loan type and default duration

A "Settled" status may remain visible on your credit report for several years.

Settlement timelines vary depending on the lender, account status, and documentation available. From written proposal to final closure letter,

Before settlement, ask HDFC for EMI restructuring; it protects your CIBIL score and keeps the account "Closed," not "Settled."

What Is HDFC Loan Settlement and Who Is It Actually For?

HDFC loan settlement is a formal arrangement where HDFC Bank agrees to accept less than what you fully owe. You pay one lump sum. The account is settled once the agreed amount is paid and the lender confirms the settlement terms in writing.

Lenders generally consider settlement when a borrower is facing genuine financial difficulty and full repayment is no longer realistic. Specifically, when it's been overdue for 90+ days and classified as an NPA (loan marked as bad by the bank). That's the RBI's standard threshold for non-performance.

3 types of unsecured loans are eligible for HDFC loan settlement: personal loans, credit cards, and business loans. Secured loans, home loans, car loans, and gold loans are outside this scope entirely. FREED does not handle secured loans.

How big is this problem? As of 31 March 2025, outstanding credit card loans with scheduled commercial banks stood at ₹2,95,084 crore, according to a parliamentary note. HDFC Bank sits at the centre of that pile; it crossed 100+ million active credit cards in 2024 per RBI data, making it India's largest credit card issuer. A meaningful portion of those accounts go into distress every year. HDFC has a formal OTS process for exactly these cases.

When Should You Consider HDFC Loan Settlement?

Settlement is usually considered when financial difficulties have reached a point where repayment is no longer manageable. It's for people who genuinely cannot pay, not even a reduced EMI, not even stretched over 2 more years.

Here are the concrete signals that settlement is worth discussing:

- 90+ days of default. Your account is now NPA. Recovery calls have likely started or escalated.

- Legal notice received. Section 138 of the Negotiable Instruments Act covers cheque bounces, which are a criminal offence. Ignoring legal notices makes things worse, not better.

- Permanent income drop. Job loss, serious medical emergency, or business closure is not a rough patch but a lasting change in your ability to earn.

- No realistic path to full repayment, even in 24 months. If you've run the numbers and the answer keeps coming up short, that's the clearest signal.

About 11% of credit card users in India default for more than 90 days, according to TransUnion CIBIL data. That's not a small number. You're not alone in this situation.

What settlement is NOT for: anyone who has the means to pay, anyone juggling multiple loans but still paying, or anyone who thinks it's a smarter financial move. The trigger is the inability to pay. If you can still pay even less, restructuring protects your CIBIL and should come first.

FREED Expert Tip

Before approaching HDFC for settlement, request a loan statement showing total outstanding principal, interest, and penalties listed separately. This is your negotiating baseline. Without it, you're negotiating blind.

Talk to a FREED ExpertWhat Documents Do You Need for HDFC Loan Settlement?

These documents help the lender better understand your financial situation. HDFC uses your hardship documents to decide whether your case is genuine. Supporting documents generally help lenders assess requests more effectively.

Documents fall into 2 groups:

Group 1 Loan and Identity Documents

- Original loan agreement or credit card application (your copy from HDFC)

- The latest outstanding statement principal, interest, and penalties listed separately

- Identity proof: Aadhaar, PAN, passport, or voter ID

- Address proof: utility bill, bank statement, or rental agreement

- Employment proof: 3 months of salary slips, or business registration documents, if self-employed

Group 2 Hardship Documentation (this group is not optional)

- Bank statements showing income drop over the last 3–6 months

- ITR (Income Tax Return) for the last 1–2 years, if you're self-employed

- Job loss letter, termination letter, or HR communication

- Medical bills or doctor's certificate, if a health emergency was the reason

- Any default notices or legal communication already received from HDFC

One payment rule that protects you: always pay via NEFT, RTGS, or an account payee cheque directly to your loan account number. Never pay cash. Never pay any agent who asks you to transfer money to a personal account. Keep your payment receipt and transaction reference permanently.

After payment clears, collect a No Dues Certificate (NDC clearance letter from the bank) and a written closure letter confirming zero balance. This is not optional. If HDFC doesn't update your CIBIL within 30–45 days, you'll need that NDC to dispute it.

Get a Free Assessment Before Approaching HDFC

A FREED counsellor reviews your case; no paperwork is needed to start.

Get My Free AssessmentHow Does the HDFC Loan Settlement Process Work, Step by Step?

HDFC doesn't advertise its OTS process. You have to initiate it. Here's the full arc from first contact to closure letter.

- Get Your Full Outstanding Statement: Contact HDFC Bank customer care or visit your home branch. Request a detailed outstanding statement with principal, accrued interest, penalty charges, and total dues listed separately. Don't accept a verbal figure. You need this in writing before any negotiation can begin.

- Write a Formal Hardship Letter to HDFC: Draft a written request addressed to HDFC Bank's settlement or collections department. State clearly that you're unable to repay the full outstanding amount due to a specific financial hardship, job loss, medical emergency, or income drop. Formally request consideration for an OTS (one-time settlement). Attach all hardship documents at this stage. A bare request without evidence is typically rejected or gets a lower waiver.

- Wait for HDFC's Counter-Offer: HDFC will review your request and respond based on its internal process. Timelines may vary. This is their opening position, not a final offer. You can counter-negotiate. Be prepared for 2–3 rounds before both sides agree.

- Get the Settlement Letter in Writing Before Paying: Once both sides agree on a figure, HDFC issues a formal settlement letter. Read every clause. Confirm the letter states: (a) the agreed settlement amount, (b) that payment closes the account in full and final settlement, and (c) that HDFC will update the CIBIL status to "Settled" after payment. Never pay before receiving this letter. Verbal commitments mean nothing.

- Pay Through a Traceable Mode Only: Pay via NEFT, RTGS, or an account payee cheque directly to your loan account number. Never cash. Never to a third-party agent. Keep the payment receipt and transaction reference permanently.

- Collect Your No Dues Certificate. After payment clears, collect a No Dues Certificate (NDC) and a written closure letter from HDFC confirming zero balance. Follow up in 30–45 days to verify your CIBIL report has updated from "Overdue" to "Settled." If it hasn't, write to HDFC with your settlement letter and payment proof.

If you're unsure how to write the hardship letter, handle the negotiation, or check the settlement letter for hidden clauses, FREED can handle the entire settlement process for you.

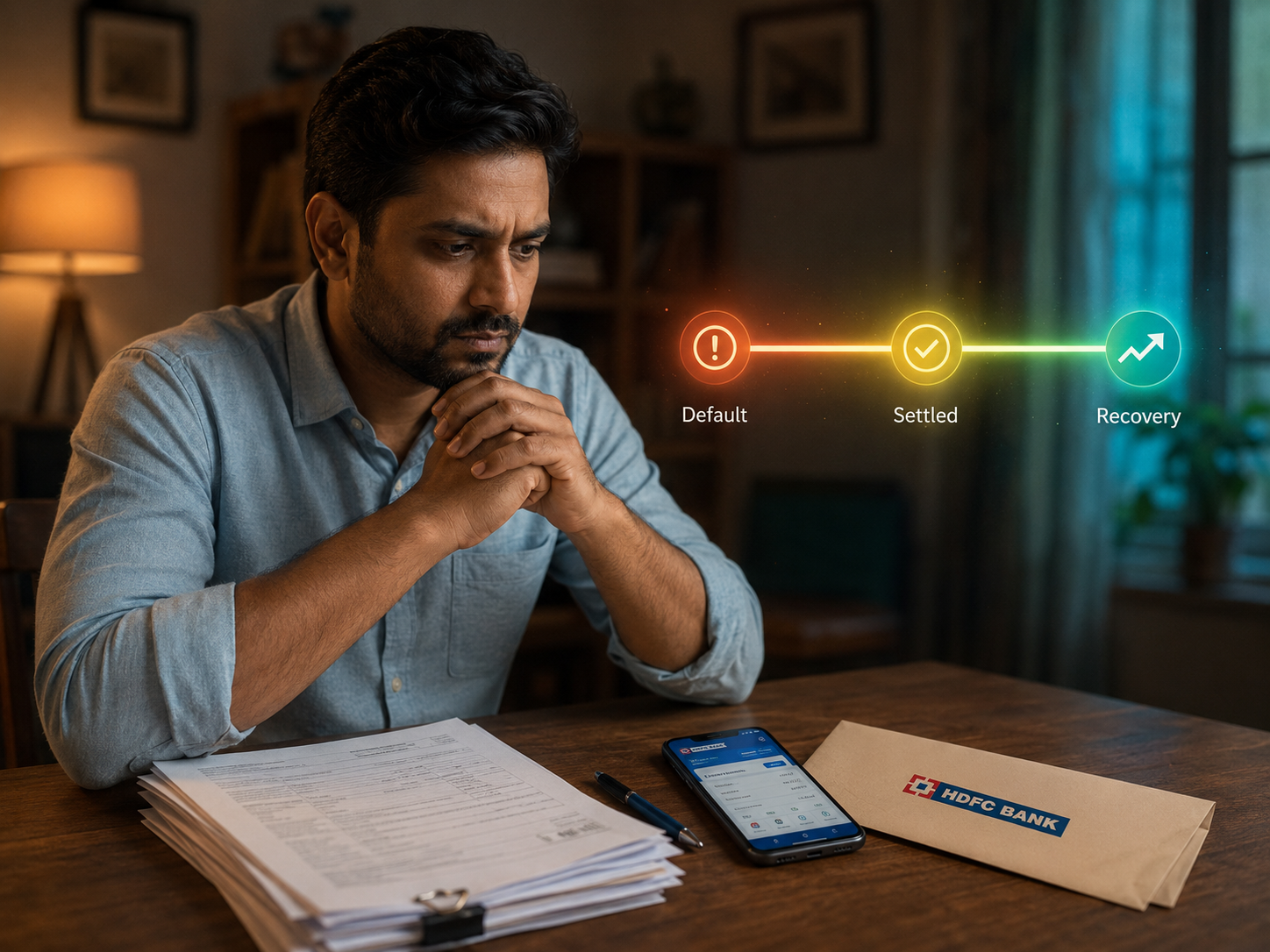

What Is the CIBIL Impact of Settling an HDFC Loan?

This is the question most people are actually asking. The honest answer is "significant, but not permanent."

- 1

The immediate impact

The moment your settlement is processed, HDFC updates your CIBIL account status from "Overdue" to "Settled." That tag stays on your credit report for up to 7 years, visible to every bank or NBFC you apply to for future loans or credit cards. The impact on your credit profile varies from person to person. Sometimes more, depending on how long

- 2

What it means for future credit

Some lenders may take a "Settled" status into account when reviewing future applications. Banks treat "Settled" accounts as a red flag: you paid less than you owed. They don't know the context. They see the tag.

- 3

CIBIL Recovery is real, but takes time

Consistent repayment behaviour over time can help strengthen your credit profile, although outcomes vary. It takes discipline and time. But it is very much possible.

- 4

The honest comparison

"Settled" is not the same as "Closed." A "Closed" account means you have repaid in full clean record. "Settled" is a negative mark. But it's still better than "Written Off", which is what happens if you default and do nothing. Don't minimise the impact. Don't let anyone tell you it doesn't matter. But don't exaggerate the permanence either. People recover

What the Law Says

Under RBI guidelines, HDFC Bank is required to report your account status accurately to credit bureaus. Once you pay the agreed OTS amount, lenders are expected to update credit bureau records accurately and within applicable reporting timelines. If they don't, you have the right to raise a dispute directly with CIBIL and with HDFC in writing, citing RBI's reporting guidelines.

Check Your Settlement OptionsHow Does FREED Help With HDFC Loan Settlement?

Settlement is not something a borrower chooses out of preference. But when it's the only exit left, doing it wrong costs you a bad settlement letter, a missed CIBIL follow-up, and a cash payment with no proof.

Here's what FREED does, specifically:

FREED supports borrowers through the settlement process by helping them understand options, organise documents, and navigate communications with lenders. That includes drafting your hardship letter, preparing your OTS proposal with the right documentation, and managing the back-and-forth across negotiation rounds. Before you make any payment, FREED verifies the settlement letter clause by clause, making sure it says what it needs to say. After payment, FREED follows up with HDFC to confirm your CIBIL report is updated correctly and within the 30-day window.

Settlement reduction: up to 50%* of total outstanding, depending on your loan type, default duration, and hardship documentation.

FREED charges fees only on successful settlement, not upfront. If the settlement doesn't go through, you don't pay.

Timelines vary depending on the lender and individual circumstances.

Facing HDFC Recovery Calls? Talk to Someone Today

Free confidential call, no commitment, no paperwork to start.

Book My Free CallHDFC Loan Restructuring vs. HDFC Loan Settlement: Which Applies to You?

Factor | Loan Restructuring | Loan Settlement (OTS) |

Who it's for | People who can pay a lower EMI but not the current one | People who genuinely cannot pay even a reduced EMI |

Default threshold | Generally available up to 30 days overdue | Available typically after 90+ days (NPA status) |

How it works | Tenure extended up to 24 months, EMI reduced | Lump sum paid at reduced amount, account resolved |

CIBIL status after | "Restructured" negative but less severe than Settled | "Settled" negative may remain visible on the credit report for an extended period. |

CIBIL score impact | Moderate 30–50 point drop | Significant 50–100 point drop |

Credit card status | HDFC deactivates card upon approval | Card already suspended in NPA |

Future loan access | Limited for 1–2 years, recovers faster | Limited for 2–4 years, longer recovery |

Best for | Someone who recently defaulted; income reduced but present | Someone’s income gone, can't pay even the reduced EMI |

Outcomes vary by individual profile, loan type, and negotiation. FREED charges fees only on successful settlement.

About FREED

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions