Debt Settlement: The Cheapest Way to Get Out of Debt?

Debt settlement can help you pay less than you owe and close your debt. While it may offer a faster way out of debt, it can also affect your credit score and financial future.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

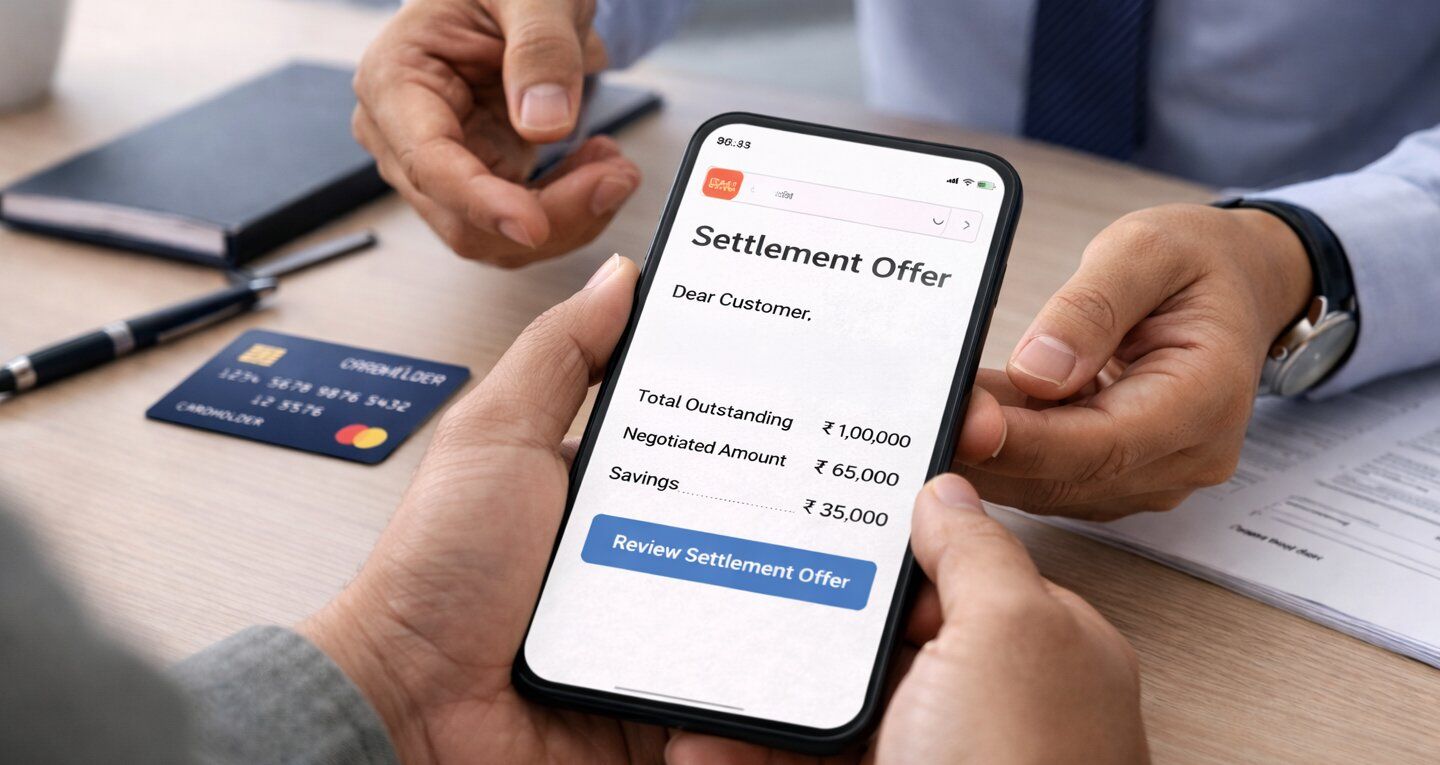

Debt settlement is a negotiated agreement where a bank or lender accepts less than the full outstanding amount as final payment, closing the account permanently.

In India, settlements typically range from 40% to 70% of the total outstanding.

For people in genuine financial hardship whose debt genuinely exceeds what income can repay, settlement can be significantly cheaper than continuing to service high-interest debt for years or allowing it to compound through default.

The consequences are real, a "Settled" remark on the CIBIL report for up to 7 years.

But for the right situation, settlement is not just the cheapest option, it is often the only realistic path to being genuinely debt-free.

What Debt Settlement Actually Is

Debt settlement is a negotiation process in which a borrower approaches a bank or lender -- directly or through a professional intermediary -- and proposes paying a reduced amount as complete and final payment of what is owed.

The bank evaluates the offer. If it concludes that accepting the reduced amount is better than the alternative of continued non-payment, compounding interest without recovery, and the cost and uncertainty of legal proceedings, it agrees to settle. The agreed amount is paid. The account is marked as closed. A settlement letter is issued confirming no further dues.

This is not debt forgiveness. The borrower does not simply walk away from the obligation. They pay something -- typically a significant portion of the principal -- but the accumulated interest, penalties, and charges that have grown the outstanding far beyond the original borrowed amount are partially or fully waived as part of the negotiated outcome.

Settlement is a legal, legitimate financial process. It is used routinely by banks as part of their NPA resolution activity. For the borrower in genuine hardship, it is the mechanism through which an otherwise impossible debt load can be resolved with a defined payment and a permanent close.

Why Banks Agree to Settle for Less

Understanding why a bank would accept less than what is owed is important -- because it clarifies both when settlement is possible and why it works.

When a loan or credit card account goes into default for 90 or more days, the bank is required under RBI accounting norms to classify it as a Non-Performing Asset. Once classified as an NPA, the bank makes internal provisions against the account -- effectively setting aside capital to absorb the expected loss. From the bank's perspective, the money is already partially written off on paper.

At this point, recovering 50% or 60% of the outstanding through a negotiated settlement is a concrete, immediate outcome that compares favourably to the alternative: continued non-payment, compounding interest that the borrower cannot pay, the expense of engaging recovery agents, and the significant cost and uncertainty of civil court litigation to enforce recovery.

Banks that go to court to recover consumer debt face long timelines -- Indian courts are slow, and a small loan recovery case can take years -- and significant legal costs that may rival or exceed the recoverable amount on smaller accounts. Settlement avoids all of this and closes the case immediately.

This is why banks settle. Not out of generosity, but because it is the rational financial outcome when full recovery is not realistic.

FREED Expert Tip

Banks are most willing to negotiate settlement when the account has been in NPA status for 6 to 12 months, the borrower's hardship is clearly documented, and a lump sum can be offered. Approaching a bank with a settlement proposal before default, or immediately after a first missed payment, rarely produces a meaningful reduction because the bank still expects full recovery. Timing and documentation matter enormously.

Enroll NowWhat Types of Debt Can Be Settled

In India, unsecured consumer debt is the primary category eligible for settlement negotiation. This includes credit card outstanding balances, personal loans, BNPL (Buy Now Pay Later) dues, unsecured business loans, and instant digital loans from fintech lenders.

These are unsecured debts -- no asset has been pledged as collateral. The bank's only recourse in non-payment is civil litigation, which is expensive and uncertain. This is what gives the borrower negotiating leverage in the settlement conversation.

Secured debt -- home loans, vehicle loans where the vehicle or property is pledged -- is treated differently. The bank can invoke the SARFAESI Act to take possession of the collateral without court intervention if certain thresholds are met. The borrower's leverage in a settlement negotiation is far lower for secured debt, and the dynamics are entirely different. Settlement of the type described in this article applies primarily to unsecured consumer debt.

How Much Does Settlement Actually Cost

The total cost of settlement has two components: what you pay to the bank as the settlement amount, and the downstream consequences to your credit profile.

On the payment side, most settlements in India are concluded in the range of 40% to 70% of the total outstanding at the time of negotiation. The total outstanding at that point includes the original principal, unpaid interest accumulated during the default period, late payment fees, and penalty charges. Because these additions can be substantial -- an account that was Rs. 2 lakh in principal may show Rs. 3.5 lakh in total outstanding after 12 months of default -- even a settlement at 60% of the outstanding may represent paying less than the original principal.

To illustrate with a simplified example: a borrower with Rs. 2 lakh original credit card debt that has compounded to Rs. 3.5 lakh in total outstanding after fees and interest might settle for Rs. 1.75 lakh -- which is 50% of the outstanding figure but actually less than the original borrowed amount. The total cost of this resolution, in rupees actually paid, is lower than what would have been paid in interest alone if the minimum payment cycle had continued for another two years.

On the credit profile side, the account is marked "Settled" on the CIBIL report. This remark reduces the score and remains for up to 7 years from the date of first default. Future credit applications are affected in the near term. These consequences are real and should be factored into any decision. But they should be compared honestly against the alternative -- continued default, compounding charges, potential legal action, and an indefinitely growing debt load.

Settlement vs Other Debt Resolution Options

Compared to continuing minimum payments on a high-interest credit card, settlement is dramatically cheaper. A borrower paying the minimum on a Rs. 3 lakh credit card outstanding at 40% annual interest may pay more than Rs. 3 lakh in interest alone over the next 5 years without meaningfully reducing the principal. Settlement at 50% of the outstanding closes the account for Rs. 1.5 lakh today.

Compared to a personal loan for debt consolidation, settlement may be cheaper for someone in default whose CIBIL score would attract a high interest rate on any new loan. A consolidation loan at 20% to 24% interest, while better than a credit card, still requires paying the full principal over time. Settlement eliminates a portion of the principal.

Compared to doing nothing and allowing the debt to continue compounding, settlement is always cheaper. Interest, penalties, and charges continue to grow through every month of default. The total outstanding grows. The eventual settlement percentage, when the bank finally initiates legal proceedings or write-off, may be no better -- and the borrower has experienced more damage, more harassment, and more time in the unresolved situation.

Legal Note

Under RBI guidelines, banks must update the credit bureau accurately within 30 days of a settlement. The account should be marked "Settled" -- not "Written Off" or still "Outstanding." If the bank fails to update the bureau correctly after the settlement is paid and the settlement letter is issued, the borrower can raise a formal dispute with CIBIL under the Credit Information Companies (Regulation) Act. FREED assists clients with this process as part of the programme.

Know your rights as a borrowerThe Real Cost of Settlement -- CIBIL and Beyond

The CIBIL consequence of settlement is the most significant ongoing cost and deserves a clear-eyed assessment.

The "Settled" remark stays on the credit report for up to 7 years from the date of the first default -- not from the date of settlement. This means that an account that went into default in January 2025 and was settled in March 2026 will have the negative history on the report until early 2032, regardless of when the settlement happened.

During this period, new credit applications will be affected. Home loans and vehicle loans from major banks are difficult to obtain with a recent settlement on the report, particularly in the first 1 to 3 years. Personal loans are possible but likely at higher rates. Secured credit cards become the primary tool for rebuilding credit history during this period.

After 2 to 3 years of consistent positive financial behaviour -- on-time payments on all obligations, low credit utilisation on any active credit products, no new defaults -- the score typically recovers to the point where major credit products become accessible again. By the 5 to 7 year mark, the impact of the settled account diminishes further as positive history accumulates on top of it.

This is the real cost of settlement. It is not permanent. But it is real, and it should be part of the decision.

How to Settle Debt in India

The settlement process follows a consistent sequence regardless of whether it is handled directly or through a professional.

The starting point is a clear picture of the total outstanding on the account to be settled -- principal, interest, and all accumulated charges -- and an honest assessment of what lump sum the borrower can realistically offer.

The next step is formal, written communication with the bank's settlements or recovery department. A hardship letter explaining the changed financial circumstances and proposing a settlement is submitted along with supporting documentation -- salary slips, bank statements, medical bills, termination letters, or whatever documents support the case.

The bank evaluates the proposal and typically responds with a counter. Multiple rounds of negotiation follow. The final agreed amount is confirmed in a written settlement letter from the bank on official letterhead, stating the settlement amount, confirming the account is being closed, and providing a reference number.

Payment is made only after the settlement letter is in hand. After payment, a No Dues Certificate is obtained confirming no further amounts are owed.

FREED handles this entire process on behalf of enrolled clients -- from the initial creditor contact and documentation to the final settlement letter and NOC, and the credit bureau follow-up that ensures the account is correctly reported.

When Settlement Is the Right Choice

Settlement makes sense when several conditions are present together.

The debt is unsecured -- credit card, personal loan, BNPL. The total outstanding has grown significantly beyond the original borrowed amount due to accumulated interest and charges. The borrower's financial situation has genuinely changed -- income reduced, job lost, medical expenses incurred -- such that repaying the full outstanding over any realistic timeline is not possible. The account has been in default for 90 days or more, making the bank open to negotiation. And the borrower can access a lump sum -- from savings, family support, or a structured programme -- to fund the settlement.

When all of these are true, settlement is not just the cheapest option. It is the most direct path to being genuinely debt-free with a defined, predictable outcome.

When It Is Not the Right Choice

Settlement is not the right choice when the debt is manageable through restructured repayment and the borrower's income can support full repayment over time. The CIBIL consequence of settlement is significant, and if the debt can be resolved without it, that is the better outcome.

It is not the right choice when the borrower has assets -- property, savings -- that could service the debt and that a bank could claim through legal proceedings. Settlement negotiations assume genuine hardship. Approaching a bank for settlement while holding substantial assets is both ethically questionable and practically risky.

It is not the right choice as a tactical move by someone who could pay but prefers not to. Banks are experienced at assessing hardship cases. A borrower who cannot demonstrate genuine financial difficulty will not achieve the settlement percentages that genuine hardship produces -- and may create legal complications by making representations that are not accurate.

About FREED

FREED is India's leading debt resolution platform. We have helped over 60,000 Indians reduce, manage, and completely get out of debt, legally and without harassment.

Our Debt Resolution Programme handles the entire settlement process on behalf of enrolled clients from initial creditor contact to the final No Dues Certificate. No upfront fees. Service fee only on successful settlement.

Visit freed.care

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions