What Is a Debt Recovery Plus Letter? Meaning, Response and Your Rights

A Debt Recovery Plus letter is a formal pre-legal notice sent by a bank or NBFC (non-bank loan company) to a borrower who has missed EMIs. It is more serious than a reminder SMS or a collection call, but it is not yet a court notice. It signals that the bank is preparing to move to stronger recovery steps if nothing is done.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

A Debt Recovery Plus letter is a formal pre-legal notice from your bank or NBFC about overdue dues

It usually arrives after 60 to 90 days of missed payments and before legal action begins

Ignoring it may lead to further recovery steps, legal escalation, and additional impact on your credit profile.

You have the right to negotiate, settle, or rework the dues even at this stage

At FREED, we support borrowers during settlement discussions and communication with banks.

What Is a Debt Recovery Plus Letter?

A Debt Recovery Plus letter is a formal written communication from a bank or NBFC to a borrower whose loan or credit card account has gone overdue. It is sent by the bank's internal recovery cell or through a third-party recovery firm working on the bank's behalf.

This letter is different from an SMS reminder or a casual call from a collection agent. Those are early-stage nudges. A Debt Recovery Plus letter means the account has moved from general collections to a dedicated recovery process. The bank is now tracking it more closely and has set a formal deadline for a response.

It is also different from a legal notice under arbitration, a Section 138 cheque bounce notice, or a SARFAESI notice for secured loans. Those come after this stage. The Debt Recovery Plus letter is a warning that recovery and legal escalation may continue if the issue remains unresolved.

Why Did You Receive This Letter?

Banks do not send this letter after one missed payment. It typically arrives after a clear pattern of non-payment. Common triggers include:

- Two to three months of missed EMIs on a personal loan or credit card

- Repeated bounced cheques or failed auto-debit (NACH) attempts

- Your account moving internally from the general collections team to the bank's dedicated recovery cell

- Outstanding dues crossing a certain threshold the bank now considers the account a priority

- A third-party recovery agency being assigned to your account by the bank

Whatever the trigger, receiving this letter means the bank has made a formal record that you are in default. That record matters for what follows.

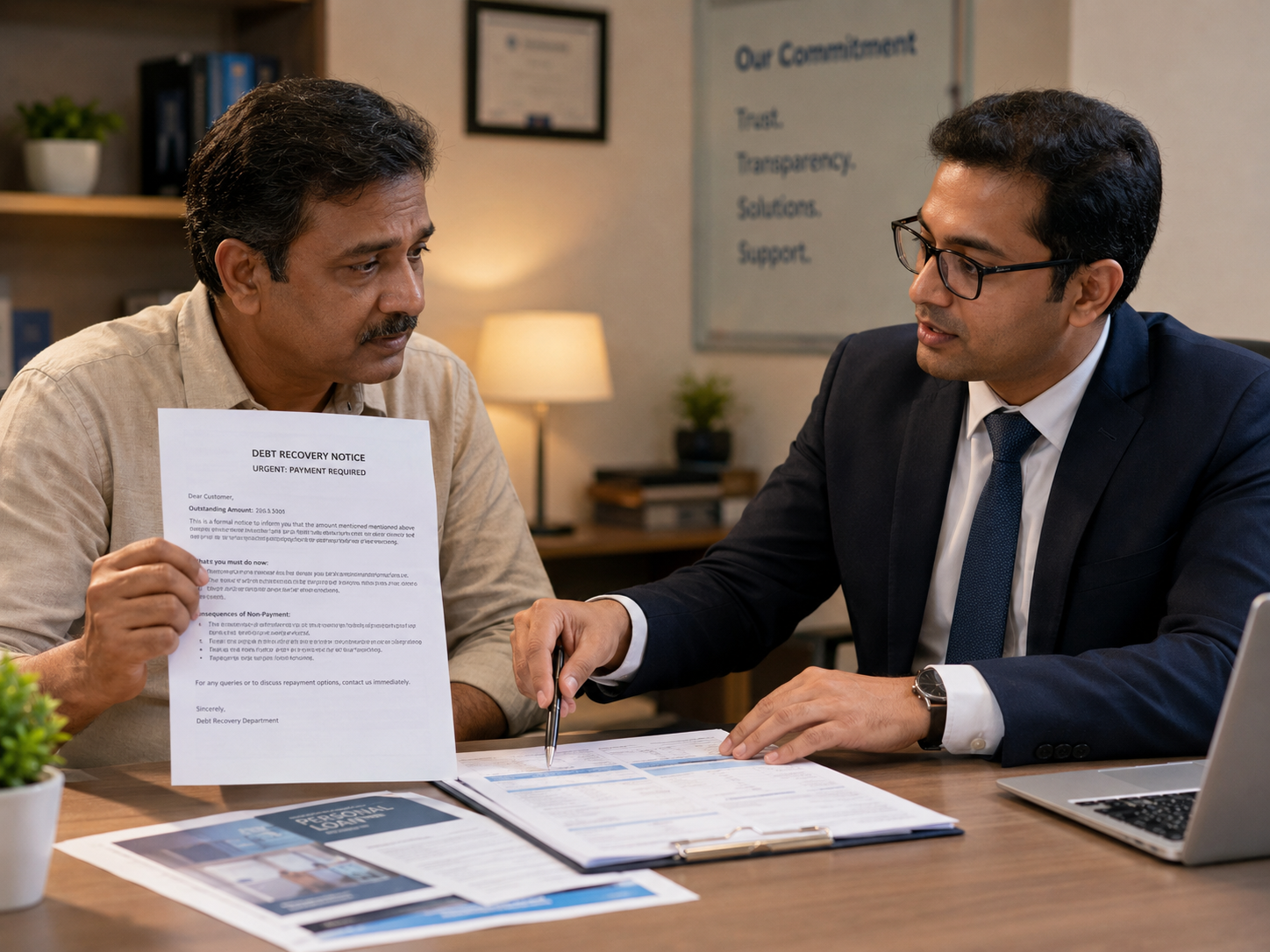

What Does a Debt Recovery Plus Letter Look Like?

The exact format varies by bank and recovery agency. But most letters include the same standard elements.

- Your full name and loan account number

- Total outstanding amount this includes principal, accrued interest, and any penalties

- A deadline by which you must respond or make a payment

- A clear mention of what happens if you ignore the letter, possible legal escalation, credit-bureau reporting, and recovery follow-up.

- Name and contact details of the recovery officer handling your account

- The name of the recovery agency if the bank has outsourced collection

One thing to check carefully: the outstanding amount stated. Banks and recovery agencies sometimes include incorrect fees or calculation errors. Before you respond or pay anything, verify the figure against your last account statement or ask the bank for a full dues breakdown in writing.

What Happens If You Ignore the Letter?

Ignoring a Debt Recovery Plus letter does not make it go away. The bank reads silence as non-cooperation, and the process moves forward without you.

Here is what typically follows, in order:

- Your credit profile may be significantly affected depending on your current score and how long the default continues.

- The account may receive closer recovery attention internally, making any future negotiation harder

- Recovery agent calls and home visits begin or intensify

- The bank issues a formal legal notice this goes on record and is harder to settle quietly

- For unsecured loans (personal loans, credit cards), the bank may file a civil suit or initiate arbitration

- For secured loans (home loan, car loan), SARFAESI proceedings can begin, which can lead to asset action note that FREED works only with unsecured loan settlement

The situation may begin affecting daily life and personal relationships.

Your Rights as a Borrower When You Receive This Letter

Receiving a recovery letter does not strip you of your rights. These protections exist regardless of how much you owe or how long you have been in default.

- Right to know the exact dues breakdown you can ask for a full statement showing principal, interest, and penalties separately

- Right to dispute incorrect amounts if the figure in the letter does not match your records, you can challenge it in writing

- You may approach the bank to discuss settlement or repayment options.

- Right to protection from harassment under the RBI Fair Practices Code no abusive calls, no threats, no contacting your family or employer without your consent

- Right to a written response and reasonable time to act verbal demands or same-day pressure are violations

- Right to ask any agent to clearly identify themselves and show valid credentials before you engage

How to Respond to a Debt Recovery Plus Letter

The worst response is no response. The second-worst is a panicked, unplanned one. Here is the right approach, step by step.

- 1

Do Not Ignore It, but Do Not Panic

Read the letter carefully, twice. Note the deadline. Understand what is being asked. A clear head here saves a lot of trouble later.

- 2

Verify the Outstanding Amount

Pull out your last loan statement or credit card bill. Cross-check the figure the letter states. Errors in fee calculation happen more often than you think. If anything looks off, note it before you respond.

- 3

Do Not Make a Random Partial Payment

Paying a small amount without a written settlement agreement can sometimes affect future negotiation flexibility. Any payment should be part of a clear plan.

- 4

Do Not Sign Anything on the Spot

If an agent visits and pushes for a cheque, auto-debit consent, or a signed acknowledgment, pause. Tell them you need time to review. Signing under pressure often locks you into terms that are not in your favour.

- 5

Document Every Call and Visit

Write down names, dates, phone numbers, and what was said. Screenshot WhatsApp messages. Record calls where you are part of the conversation, this is generally permitted in India. This documentation is useful if harassment escalates or if you need to file a complaint.

- 6

Get Expert Help Before Responding in Writing

This is where most borrowers make an avoidable mistake. A written reply to a recovery letter is a formal document. The wording can affect your legal position later. At FREED, we draft your reply, open the settlement conversation with the bank, and negotiate terms that actually reduce what you owe. Doing this alone is risky because careful wording is important

Don't reply alone. Let FREED handle it for you

Received a Debt Recovery Plus letter? Don’t respond in panic. FREED can help you understand the notice, your rights, and the safest next step.

Get Help from FREEDShould You Settle, Rework the Plan, or Pay in Full?

Three options exist. Each has a different outcome for your CIBIL score and your cash flow.

Pay in Full Best outcome for your CIBIL score. The account closes as ‘Closed’, the cleanest result. But it requires paying the entire outstanding including interest and penalties.If you have the funds, this is the right choice. Most people who receive a recovery letter do not have the full amount available. .

Rework the Repayment Plan The bank stretches your repayment time or temporarily reduces your EMI. This can help if your income will genuinely recover in the next few months. Your CIBIL takes a smaller hit than settlement. But the bank does not always agree, and it does not reduce what you ultimately pay.

Settle You make one final reduced payment typically less than the full outstanding and the bank closes the account permanently. This is reported as "Settled" on your CIBIL report, which is a mark that stays for up to 7 years. But for borrowers in genuine financial difficulty, it resolves the debt through settlement and generally ends recovery activity on that account once documented.

Most people get stuck because they do not know which option fits their actual situation. At FREED, our team looks at your full picture, talks to your bank, and recommends the path that works, not what is easiest for the bank.

Why Negotiating Directly With the Bank Rarely Goes Your Way

It is not that banks are dishonest. It is that they are experienced and you are not. Banks handle thousands of recovery conversations every month. Most borrowers handle one in their lifetime.

Banks have internal recovery steps. Initial offers may not always reflect the most workable long-term solution. They use formal legal language that can feel intimidating to borrowers, even when it is not. Most borrowers, feeling the pressure, accept early offers that are significantly higher than what the bank would have eventually agreed to.

On top of this, agents earn commission on what they collect. Their focus is generally on recovering dues quickly. They are not trying to find the best outcome for you.

There are also important technical details. Not knowing which clauses to dispute. Not knowing how to time a settlement offer for when the bank is most likely to agree. Not knowing what the settlement letter must say to help ensure the documentation and reporting process is handled properly. A single missing clause can mean the bank comes back later claiming the account is still open.

At FREED, our team talks to banks every day. We know how these conversations work, when to push, and how to lock the deal in writing so it holds.

How FREED Helps You Handle a Debt Recovery Plus Letter

Here is exactly what we do for you, not instructions for you to follow alone.

- We study your recovery letter and your full debt position before anything else

- We send formal communication to your bank to support borrowers through formal communication and escalation processes during negotiations.

- We open a direct settlement conversation with your bank's collections team not the field agent

- We negotiate settlement terms based on your financial situation and the bank’s policies.

- We review every clause of the settlement letter before you sign anything

- We help borrowers follow up on documentation and bureau reporting after payment. The outcome is usually much better than borrowers expect.

If you have multiple loans, we handle all of them in one process one point of contact, one resolution

Ignoring vs Responding Smartly A Quick Comparison

Action | CIBIL Impact | Bank Action | Legal Risk | Stress |

Ignore letter | 200-300 pt drop | Legal suit likely | High | Very High |

Random partial payment | Mild damage | Chase full dues | Medium | High |

Settle via FREED | Controlled, recovers | Written settlement, closed | Low | Low |

FREED Expert Tip

The moment you receive a recovery letter is actually the best time to negotiate a settlement. Banks at this stage want to recover something quickly rather than wait years for a court verdict. Wait too long and your bargaining position weakens. Act at the right time with the right approach and borrowers often feel more informed and prepared when they act early.

Talk to a FREED ExpertFREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions