Debt Inheritance Explained: What Happens to Loans After Death?

Confused about debt inheritance? Find out can you inherit debt from your parents in India, what the law says, and how family debts are handled.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

In India, debt does NOT automatically pass to family members after the borrower's death. You do not inherit your parents' or spouse's loans just because you are related.

The bank's claim is limited to the assets the borrower left behind - property, savings, investments. If those aren't enough, the shortfall does not become the family's personal burden.

- Co-borrowers and guarantors are exceptions - they remain legally responsible for the loan even after the primary borrower's death.

Banks cannot legally force family members to repay loans using emotional pressure unless they are officially listed as co-borrowers or guarantors.

If you are facing bank pressure after a family member's death - FREED's team can guide you on your legal rights and what to do next.

The Question Every Family Asks After a Loss

When someone passes away, grief is already overwhelming. And then the calls start.

The bank calls about the home loan. A message comes about the credit card due. A relative asks anxiously "Is this now our problem? Do we have to pay this?"

This moment of confusion and fear is very common in Indian families. Most people don't know what the law says. And banks and collection agents don't always volunteer that information clearly.

So let's answer this directly, honestly, and simply.

Can You Inherit Debt in India? The Short Answer

In India, debt does not automatically pass from a deceased person to their family members.

You do not become responsible for your parent's personal loan just because you are their child. You do not inherit your spouse's credit card debt just because you are married to them.

The loan belonged to the person who signed for it. It does not travel through family relationships.

This is the basic principle of Indian law on debt inheritance and understanding it can save families from enormous unnecessary stress and wrong payments.

How Debt Inheritance Works Under Indian Law

When a person passes away, their loan does not disappear but it also does not automatically move to their family.

Here is what actually happens:

The bank looks at what the borrower has left behind. This is called the "estate" it includes property, money in bank accounts, fixed deposits, investments, gold, or any other assets in the deceased person's name.

The bank's recovery claim is against this estate not against the family's personal money or savings.

If the estate has enough to cover the outstanding loan it gets paid from there.

If the estate does not have enough the remaining amount is typically written off. The family does not have to make up the difference from their own pockets.

The key principle: the lender's claim ends at the boundary of what the borrower owned — not at the boundary of who the borrower loved.

What Happens to Different Types of Loans After Death?

Different loans are handled differently. Here's a clear breakdown:

Type of Loan | What Typically Happens After Death |

Home Loan | Recovered from the property itself. If loan insurance exists, the insurer pays it off. |

Personal Loan | Adjusted against available estate assets. If no assets are typically written off. |

Credit Card Dues | Settled from estate if possible. If insufficient assets balance written off. |

Education Loan | Many are waived or covered by insurance. Check the loan agreement carefully. |

Business Loan | Depends on whether someone was a co-borrower or guarantor on the loan. |

Vehicle Loan | Secured against the vehicle bank may repossess it to recover dues. |

The most important thing to do immediately after a death is to check whether the loan had insurance coverage. Many home loans and large personal loans come with a loan protection insurance policy which clears the outstanding amount automatically upon the borrower's death.

Many families don't know this insurance exists and unnecessarily worry about or even pay loans that would have been covered.

Nominee, Co-Borrower, Guarantor, Legal Heir - Who Pays What?

Role | Are They Responsible for the Loan? |

Nominee | No - only receives and distributes assets |

Legal Heir | Only to the extent of inherited assets |

Co-Borrower | Yes - fully responsible for continued repayment |

Guarantor | Yes - if the primary borrower defaults |

FREED Expert Tip

If you have taken a large loan - especially a home loan - consider getting a loan protection insurance policy. This policy pays off your outstanding loan amount if you pass away. It protects your family from inheriting the burden of your debt. Many banks offer this at the time of loan disbursement

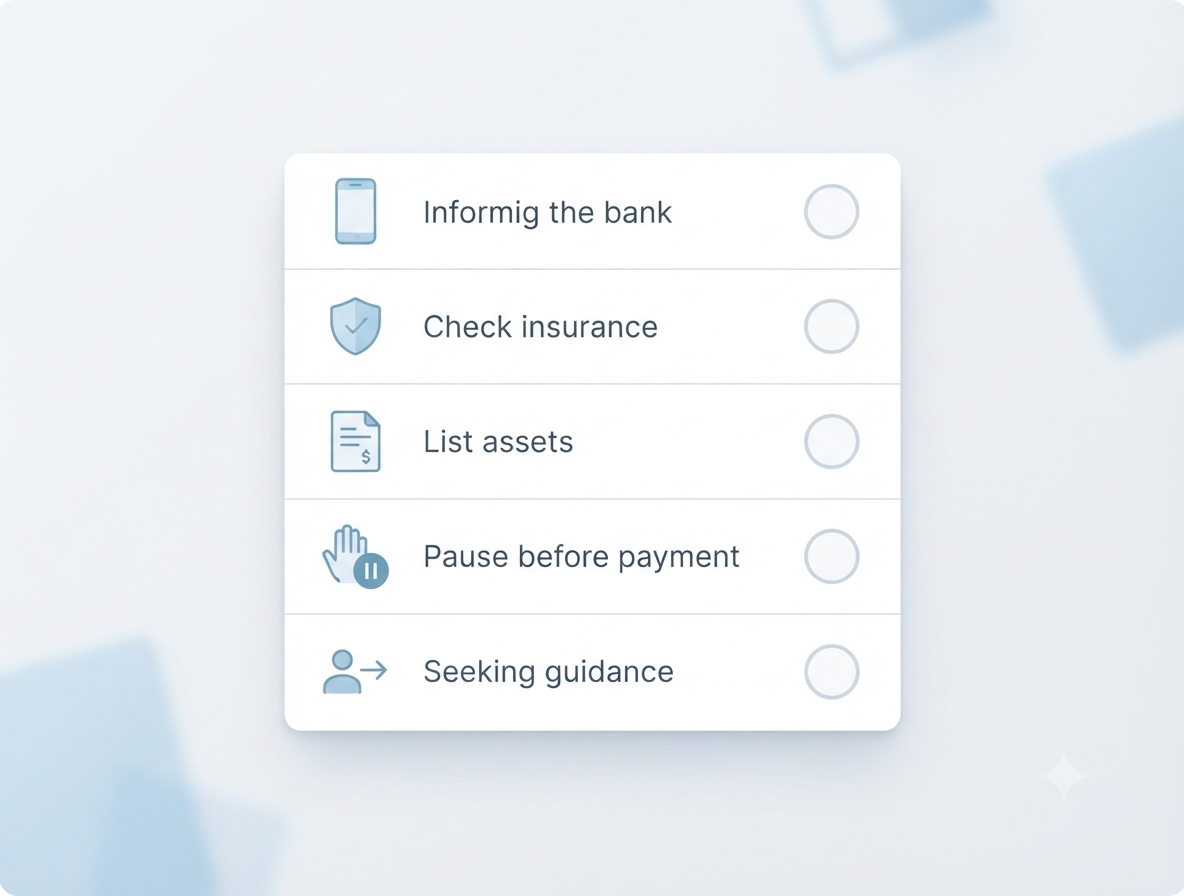

Talk to FREEDWhat Should Heirs Do Immediately After the Borrower's Death?

The first 30 days after a loved one's passing are the most important for managing their financial affairs. Here's exactly what to do — step by step.

- 1

Step - Inform the bank immediately

Call the bank and inform them of the death. Submit a copy of the death certificate. This officially updates the bank's records and stops unnecessary automated follow-up messages and EMI reminders from going out.

- 2

Step - Check for loan insurance

Ask the bank specifically - "Was this loan covered by a loan protection insurance policy?" Get this information in writing. Many home loans and large personal loans have insurance that clears the debt automatically - but families are often not told about it.

- 3

Step - List all assets and liabilities

Sit down and make a clear list. What assets did the deceased own - property, bank accounts, FDs, investments, gold, vehicle? And what loans or credit card dues were outstanding? Having this on paper removes confusion and panic.

- 4

Step - Do not make payments under pressure

Banks and collection agents may call urgently. Do not make any payments just because someone sounds urgent or threatening. Take time to understand the full situation first. You may not be legally required to pay anything at all.

- 5

Step - Get proper guidance if needed

If the situation is complicated - multiple loans, large amounts, aggressive bank communication - speak to a debt counsellor or legal advisor before making any decisions. FREED's team can guide you on your rights in a free consultation.

Can Banks Force Family Members to Pay?

This is the most critical question - and the answer is important.

Banks cannot force family members to pay a deceased person's debt just because they are related.

They cannot legally demand payment from a son, daughter, spouse, or parent - unless that person is officially listed as a co-borrower or guarantor on the loan agreement.

Recovery based on emotional pressure "you are the son, it's your responsibility" - has absolutely no legal standing.

If a bank or collection agent is pressuring you to pay your family member's loan from your personal money - and you are not a co-borrower or guarantor - they are operating outside their legal authority.

You can refuse. You can ask them to communicate in writing. And if harassment continues, you can file a complaint.

What the Law Says

Under Indian law, debt liability does not transfer to family members automatically upon death. The Transfer of Property Act and the Indian Succession Act both confirm that a deceased person's debts are to be settled from their estate - not from their heirs' personal assets. Additionally, under RBI's Fair Practices Code, banks and recovery agents cannot use coercive, misleading, or abusive methods to recover loans from family members who are not legally liable. If a bank is claiming otherwise - that is a violation of your legal rights.

Talk to a FREED CounsellorWhat If the Estate Has No Money to Repay the Debt?

This is a situation many families face and it has a clear answer.

If the assets left behind by the deceased are not sufficient to cover the outstanding loan - the remaining balance is written off by the bank.

This is normal banking practice. Banks account for the possibility of borrower death and loan defaults in their risk calculations. The loan does not become the family's personal burden just because the estate ran out.

The family is not required to use their own savings, sell their own property, or take a new loan to cover the deceased person's outstanding debts - unless they were co-borrowers or guarantors.

How to Protect Your Family Before It's Too Late

The best time to deal with this issue is before it becomes a crisis. If you currently have loans - here are steps to protect your family:

Get loan protection insurance Specifically for home loans and large personal loans. This pays off the outstanding amount if you pass away - so your family doesn't have to.

Be careful before co-signing or guaranteeing a loan. Only co-borrow or guarantee a loan if you are fully prepared to repay it yourself. These are serious legal obligations.

Keep your financial records organised. Make sure your family knows what loans you have, which bank, and whether any are insured. Keep physical and digital copies of important documents where your family can find them.

Do not add family members as co-borrowers unnecessarily When a bank asks for a co-borrower - understand what that means for that person legally before adding them.

How FREED Helps Families in Debt Situations

FREED primarily helps people who are struggling with their own loans - through debt consolidation and debt settlement.

But we also regularly speak to families who are facing confusion after a loved one's death - because banks have contacted them, collection agents are calling, and they don't know what their rights are.

If you are in this situation - FREED's counsellors can:

- Help you understand whether you are legally obligated to pay or not

- Guide you on how to communicate with the bank correctly

- Help you document the situation and respond to the bank in writing

- If you yourself have taken loans that are becoming unmanageable — help you explore settlement or consolidation options

Your first call with FREED is always free. No commitment. No pressure. Just honest guidance.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions