Understanding Settlement of a Loan - What It Is, How It Works, and What to Expect

Struggling to repay a loan? Loan settlement lets you close your debt by paying less than what you owe. But there's a lot you need to understand before you go down this path. This guide explains everything - simply and honestly.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

Loan settlement means you pay a lower amount than what you owe - and the bank agrees to close the account. The remaining balance is waived.

Banks agree to settle only when you can genuinely prove you cannot repay the full amount - usually after 90+ days of non-payment.

Settlement does affect your CIBIL score - your report shows "Settled" instead of "Closed." But it stops further damage from ongoing default.

Always get the settlement agreement in writing - with a clear No Dues Certificate after payment. Never settle verbally.

FREED's certified counsellors negotiate settlements with banks on your behalf - and typically get better outcomes than going alone.

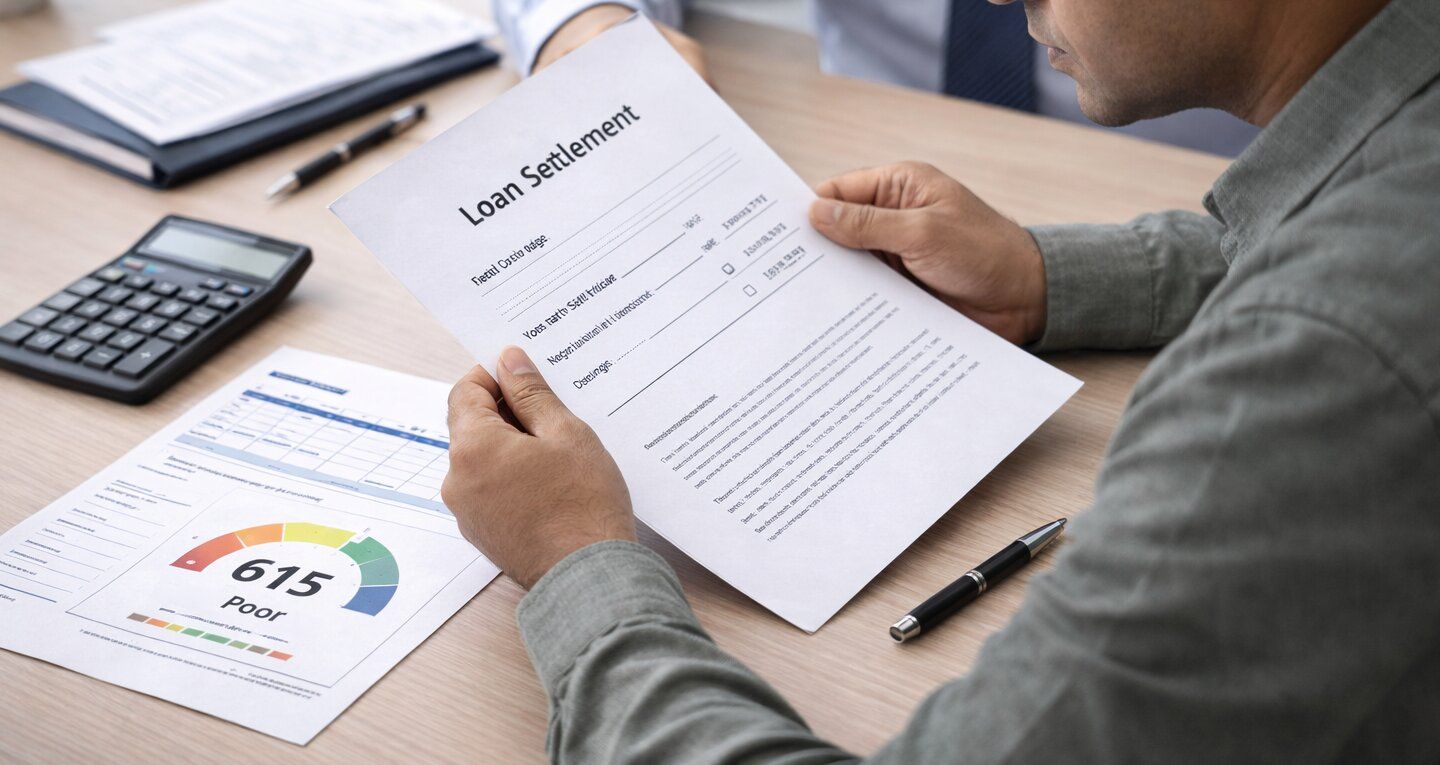

What is Loan Settlement?

Loan settlement is an agreement between you and your bank.

You owe a certain amount. You genuinely cannot pay it all back. So you and the bank agree - you will pay a lower amount. Once you pay that agreed amount, the bank closes your loan account. You have no further obligation.

Here's a simple example:

You owe ₹5,00,000 on a personal loan. You've lost your job. You've been unable to pay for several months. The bank, after reviewing your situation, agrees to settle for ₹2,90,000. You pay that amount. The loan is closed. The remaining ₹2,10,000 is waived off.

That sounds like a big relief - and it is. But it comes with consequences that you must fully understand before deciding.

Settlement is not a loophole or a trick. It is a formal, legal agreement - and both sides must follow through on what they commit to.

You Are Not Alone in Feeling Overwhelmed

According to the Reserve Bank of India's Financial Stability Report, nearly 50% of borrowers who have a credit card or personal loan also have another active loan - like a home loan or car loan - running at the same time.

Managing two or three loans simultaneously is genuinely hard. And when a crisis hits - a job loss, a medical emergency, a business failure - it can become impossible.

Most people who consider loan settlement didn't arrive here because they were careless. They arrived here because life happened.

If you're in this situation - you are not alone. And there is a way forward.

When Should You Consider Loan Settlement?

Loan settlement is a last resort. It is not the first option to explore.

Before thinking about settlement, ask yourself these questions:

- Can I restructure my loan - get a longer tenure or lower EMI?

- Can I consolidate all my loans into one lower monthly payment?

- Can I make partial payments and negotiate with the bank informally?

If the answer to all of these is no - and you genuinely cannot repay even a restructured amount - then settlement is the right conversation to have.

Signs You May Need Loan Settlement Right Now

Warning Sign | What It Means |

Missed 3 or more EMIs in a row | Bank has likely flagged your account as NPA |

Only able to pay minimum due on credit card | Interest is growing faster than you're paying |

Using one loan to pay another | Classic debt trap - situation is worsening |

Receiving calls from collection agents daily | Bank has started active recovery process |

Received a legal notice from the bank | Bank may move to legal recovery soon |

No income or severely reduced income | Repayment is genuinely not possible |

If 3 or more of these match your situation - settlement may be the most realistic option available to you right now.

How the Loan Settlement Process Works - Step by Step

- 1

Step 1 - Understand Your Financial Situation Honestly

Before approaching the bank, be clear about your own numbers. Write down: Total outstanding loan amount Your current monthly income - if any Your monthly essential expenses - rent, food, utilities Any savings or assets you have This tells you two things. First - can you genuinely not repay? Second - what amount could you realistically offer as a settlement?

- 2

Step 2 - Contact Your Lender and Start the Conversation

The next step is to call or visit your bank and tell them you are facing genuine financial hardship. Ask to speak to the settlements department or the collections team. Don't avoid calls or letters. That only makes things worse. When you talk to them: Be honest about why you cannot repay Don't exaggerate - and don't hide anything Ask

- 3

Step 3 - Negotiate the Settlement Amount

This is the most important step - and the most nerve-wracking one for most people. The bank will make an initial offer. You can counter. This is a negotiation - not a take-it-or-leave-it situation. Banks typically settle for 40–70% of the total outstanding. Where you land depends on: How long you've been in default Your documented financial hardship Your ability

- 4

Step 4 - Get the Agreement in Writing

This step is non-negotiable. Never pay a single rupee without a written settlement letter from the bank. The written settlement agreement must clearly state: Your name and loan account number The original outstanding amount The agreed settlement amount The payment timeline and method A clear statement that once the settlement amount is paid, you have no further liability The account

- 5

Step 5 - Make the Payment and Get Your No Dues Certificate

Pay the agreed amount exactly as specified - on time, in the correct manner. If you delay - even by a few days - the bank has the right to revoke the offer. Don't let that happen. After you make the payment: Collect a written confirmation that the account is closed Get a No Dues Certificate (NDC) from the bank

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

What Happens After Settlement?

Once the loan is settled, three things happen:

1. The loan account is closed. You are no longer legally obligated to repay anything more. Collection calls stop. Legal threats stop.

2. Your credit report is updated. The account now shows "Settled" - not "Closed" or "Paid in Full." This is an important distinction. "Settled" tells future lenders that you did not repay the full amount.

3. Your CIBIL score is affected. Settlement has a negative impact on your score. But - and this is important - it is far less damaging than an ongoing default that never gets resolved.

A "Settled" status, combined with clean financial behaviour afterwards, is a path to recovery. An unresolved default with no action taken - is not.

How Does Loan Settlement Affect Your CIBIL Score?

Let's be very clear about this - because people often misunderstand.

Situation | CIBIL Status | Score Impact |

Paid in full, on time | Closed | No negative impact - positive |

Settled for less than owed | Settled | Moderate negative impact |

Default with no resolution | Written Off | Severe negative impact |

Ongoing default, no action | NPA / Overdue | Continuous score damage |

Settlement hurts your score. But it stops the bleeding.

If your loan has been in default for 6 months - your score has already fallen significantly. Settlement does not make that worse. It draws a line under it and gives you a clear starting point for recovery.

After settlement, consistent good financial behaviour - paying all other bills on time, keeping credit utilisation low, not applying for too many loans - will gradually bring your score back up.

Most people see meaningful recovery within 12–24 months of responsible behaviour post-settlement.

Settlement vs Other Debt Relief Options - Which Is Right for You?

Loan Settlement | Debt Consolidation | EMI Restructuring | |

Best for | Cannot repay at all | Can repay - but struggling with multiple EMIs | Can repay - but need lower monthly amount |

What you pay | Less than what you owe | Full amount - but in one lower EMI | Full amount - but over a longer period |

CIBIL impact | Moderate negative | Minimal - can improve over time | Minimal |

Bank approval | Needs negotiation | Needs new loan approval | Needs bank agreement |

Works when score is | Already low (below 650) | Still decent (above 650) | Any - done before default |

Simple rule:

Still paying but tight → Restructuring or Consolidation

Multiple loans, still paying → Consolidation

Already defaulted, cannot pay full → Settlement

Not sure which applies to you? That's exactly what FREED's free consultation is for.

Pros and Cons of Loan Settlement

Before you decide - see both sides clearly.

Pros:

- You pay less than what you owe - real financial relief

- The loan is officially closed - no more collection calls or legal threats

- Faster resolution than years of struggling with minimum payments

- You get a clear end date - and can start planning your financial recovery

- Better than letting the account remain in default forever

- Stops interest and penalties from piling up further

Cons:

- Your CIBIL score takes a hit - the "Settled" status stays for 7 years

- Getting new loans becomes harder for 2–3 years after settlement

- The bank is not obligated to settle - they can say no

- Any amount waived off may be treated as income by tax authorities - consult a CA

- If you don't get the agreement in writing, you have no protection

How FREED Helps You With Loan Settlement

Negotiating a loan settlement alone is stressful and complicated. Banks have experienced teams. Most borrowers don't.

FREED levels that playing field.

Here's what FREED does when you come to us for settlement support:

We evaluate your full debt situation - all loans, all lenders, your income, your expenses. We understand exactly what you owe and what you can realistically offer.

We build your case - we help you gather and organise the right documents to support your hardship claim. A well-documented case gets a better response from the bank.

We negotiate on your behalf - our experienced counsellors deal with banks regularly. We know what they respond to, what they're willing to accept, and how to push for the best possible settlement amount.

We review the settlement letter - before you pay a single rupee, we review every line of the agreement to make sure your interests are fully protected.

We guide your next steps - after settlement, we help you understand how to rebuild your CIBIL score and avoid falling into debt again.

You don't have to face the bank alone. FREED has your back - every step of the way.

About FREED

FREED is India's first and leading Debt Relief Platform. We help people who are overwhelmed by personal loans, credit card debt, and EMIs find a legal, stress-free way out.

Our certified debt counsellors negotiate with banks on your behalf, guide you through the settlement process, and help you rebuild your financial life afterwards. We also offer Debt Consolidation for people who can still repay but need a lower, more manageable EMI.

Over 60,000 Indians - from Lucknow to Coimbatore, Surat to Patna - have used FREED to take back control of their finances.

No hidden charges. No judgement. Just honest, practical help - when you need it most.

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions