CIBIL Score Improvement Agency: What to Know Before You Pay

A CIBIL score improvement agency is a paid consultancy that claims to fix credit report errors and raise your score for a fee, usually Rs. 5,000 to Rs. 30,000. Some genuinely help with dispute filing. Many overpromise results that no agency can legally deliver, because no company can manually edit your CIBIL score.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

KEY TAKEAWAYS

A CIBIL score improvement agency cannot manually change your score. Only credit bureaus and lenders update your report.

Genuine agencies help dispute report errors. Fees range from Rs. 5,000 to Rs. 30,000 or more, and there is no fixed regulation on pricing.

No agency can legally guarantee a fixed point jump or a fixed timeline. Anyone promising "750 in 30 days" is a red flag.

Report errors can be disputed for free directly with CIBIL, Experian, Equifax, or CRIF Highmark.

If your low score is linked to unpaid debt rather than a reporting error, a dispute may not resolve the issue. Depending on your situation, it may be worth exploring options such as debt consolidation or settlement.

Can a CIBIL Score Improvement Agency Guarantee a Higher Score?

No. Your CIBIL score is calculated by the bureau from your actual repayment history, current outstanding debt, credit utilisation, and account status. No agency, however well-connected it claims to be, has the ability to manually edit that number. What can genuinely be fixed are two things: real errors in your report and your own future repayment behaviour.

If your score has been affected by missed payments or high credit utilisation, improving it takes consistent, responsible credit behaviour over time. The time it takes varies from person to person.

. Credit bureaus in India update reports roughly every fortnight (about every 15 days) as new data comes in from banks and NBFCs, so changes don't reflect instantly even after a correction goes through.

Any agency that promises a specific score jump by a specific date, "750 in 30 days" being the classic version, is making a promise it structurally cannot keep. That promise alone is one of the clearest signs to walk away.

FREED Expert Tip

No company can manually edit your CIBIL score. Only genuine errors can be corrected, or you can check what's really affecting your score for free

Check Your ScoreSigns of a Fake or Unreliable CIBIL Repair Agency

A few patterns show up consistently with agencies that overpromise. Watch for these before you hand over any money.

- A guaranteed point jump or fixed timeline. No agency controls bureau calculations, so a guarantee of "50 points in a month" isn't something any legitimate business can back.

- A demand for full payment up front. Genuine service providers are usually comfortable with a partial payment or a payment tied to milestones, not the entire fee before any work begins.

- No written service agreement. If they won't put the scope of work in writing, there's nothing to hold them to later.

- No clarity on what exactly will be disputed. A real agency can tell you which specific entries on your report they intend to dispute and why. A vague "we'll handle everything" answer is a warning sign.

- Claims of "direct CIBIL contacts" or "insider access". No agency has a backdoor into bureau systems. Anyone claiming this is either misinformed or misleading you.

How to Dispute CIBIL Report Errors Yourself for Free

This entire process is free and can be completed directly through the credit bureau without paying an agency.

Step 1: Pull Your Full Credit Report

Download your report directly from CIBIL, Experian, Equifax, or CRIF Highmark. Each bureau gives you one free full report per year, so start with whichever bureau's report the lender who rejected you actually used.

Step 2: Identify the Exact Wrong Entry

Go through the report line by line and note the exact account name, the amount shown, and the status that looks wrong. Take a screenshot or save a copy as proof, since you'll need to reference this specific entry when you file the dispute.

Step 3: Raise a Dispute Directly With the Bureau

File the dispute online through the bureau's own dispute portal. This step needs no agency and no fee. You'll typically need to describe the error and attach any supporting documents, like a bank statement showing the payment you actually made.

Step 4: Follow Up Within 30 Days

Credit bureaus and lenders are expected to resolve disputes in accordance with applicable RBI guidelines. If your dispute remains unresolved, follow up with both the credit bureau and the lender that reported the information.

Step 5: Recheck Your Report After Resolution

Once you're told the dispute is resolved, download your report again from the same bureau and confirm that the correction has been updated.

What the Law Says:

RBI's Master Direction on Credit Information Reporting requires credit bureaus and lenders to resolve disputes within 30 calendar days of filing, and complainants are entitled to compensation of Rs. 100 per day of delay beyond that window. No private agency has any authority to alter your score directly

Get My Free AssessmentWhat If Your Low CIBIL Score Is Because of Unpaid Debt, Not Errors?

Everything above applies when the problem is a reporting error, something incorrect that shouldn't be on your report at all. But if your score is low because of actual missed EMIs, genuine defaults, or accounts marked "written off" after you stopped paying, no repair agency, however skilled, can dispute that away. It isn't an error. It's an accurate reflection of what happened, and disputing an accurate entry simply won't succeed.

In this situation, the real fix isn't a dispute; it's resolving the underlying debt itself. If you're still managing your payments but stretched thin across several loans, that's a different problem than being unable to pay at all, and each has a different solution. Someone managing multiple EMIs but still keeping up with repayments may benefit from exploring consolidation, depending on their financial situation. If repaying the full amount is no longer realistic, settlement may be an option worth understanding for eligible unsecured debt.

Knowing which of these two describes your situation matters more than anything a repair agency could offer, because it determines whether you need a dispute, a repayment plan, or a settlement conversation.

How FREED Helps You Track and Improve Your Credit Health

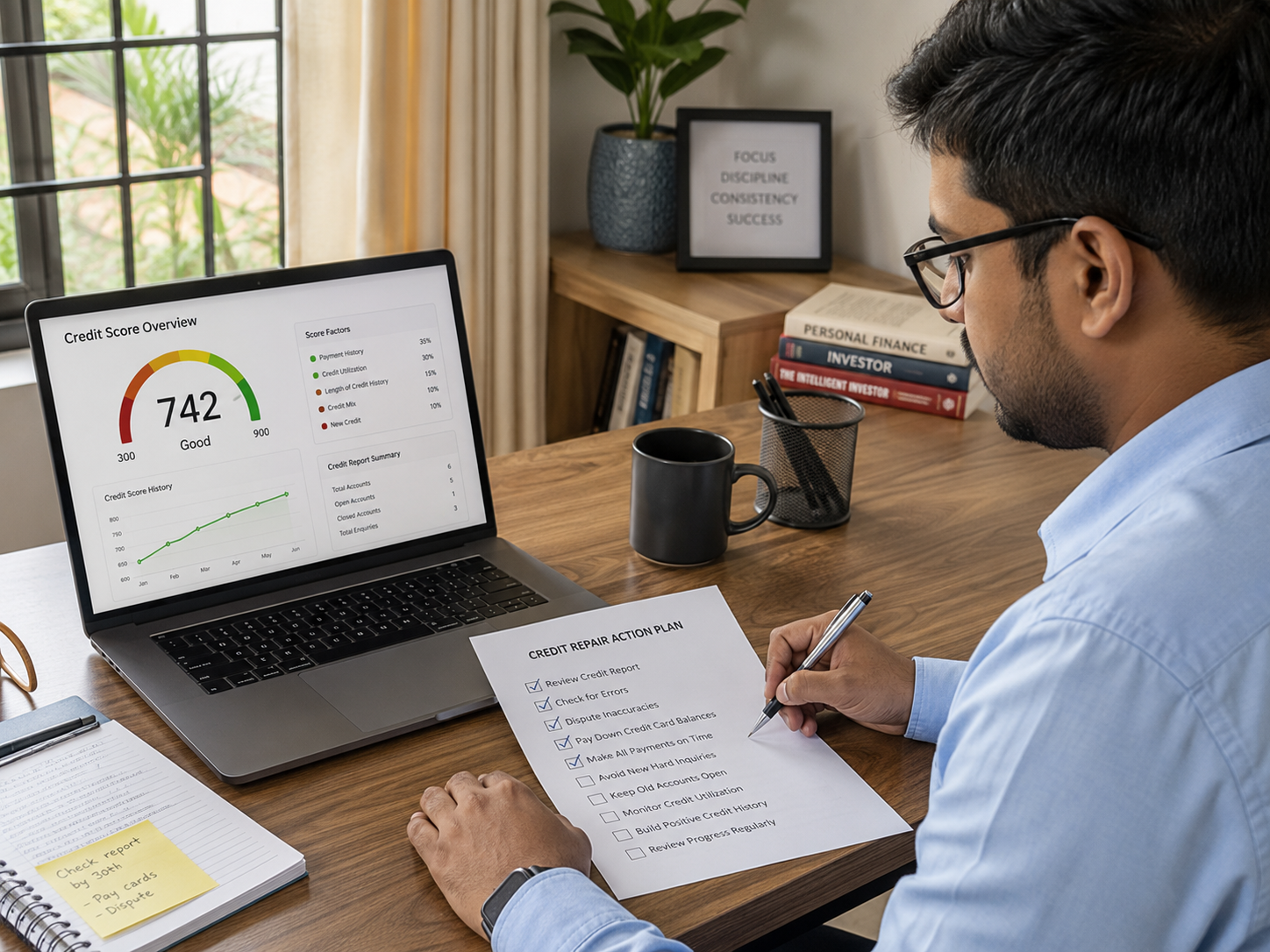

FREED doesn't promise to manually edit your score either, because no legitimate company can. What FREED offers instead is a transparent, real picture of where you stand and an actual plan to work with. FREED's Credit Insights provides your Experian-based credit report, highlights the key factors affecting your credit profile, and offers practical recommendations you can start acting on.

Credit Insights is available to everyone, whether or not you're enrolled in any other FREED program, for Rs 249 for a 3-month subscription. Unlike a repair agency charging thousands of rupees for a dispute you could file yourself, this is a low-cost way to see your actual numbers and understand what's genuinely dragging your score down, without anyone promising results that aren't theirs to guarantee.

If it turns out your low score is coming from unresolved debt rather than report errors, that's a separate conversation. FREED's Debt Consolidation Program (Reduce My EMI) helps eligible borrowers explore whether consolidating multiple EMIs into a single repayment plan is suitable for their situation.

FREED's Loan Settlement Plan (Settle My Loans) is there for borrowers who are genuinely unable to repay in full. Both exist for the debt itself, not for editing a score, and are worth exploring separately from Credit Insights, depending on what's actually going on with your finances.

What to Ask Before Hiring Any Credit Repair Agency

If you still want help with disputes and don't want to do it yourself, ask these questions before you pay anything.

Ask for the scope of work in writing, spelling out exactly what they will do and by when. Ask precisely which entries on your report they intend to dispute, and on what grounds, a real agency can answer this specifically, not vaguely. Ask what their refund policy is if the dispute doesn't succeed, since a confident agency should be willing to put some risk on themselves rather than all of it on you. Ask for their business registration details, so you know who you're actually paying and can verify they're a real, traceable entity.

If an agency can't answer these clearly or gets defensive when asked, that tells you most of what you need to know before you commit any money.

Sources

Claim in Blog | Source |

Credit bureaus and reporting lenders must resolve disputes within 30 calendar days, with Rs. 100/day compensation for delays beyond that | RBI, Master Direction – Reserve Bank of India (Credit Information Reporting) Directions, 2025: https://www.rbi.org.in/Scripts/BS_ViewMasDirections.aspx?id=12764 (full text PDF: https://rbidocs.rbi.org.in/rdocs/notification/PDFs/125MD0601257105ED8375BB487AAA4C45F3B88AD0C5.PDF) |

Credit institutions must submit updated credit data to bureaus on a fortnightly basis (roughly every 15 days) | RBI, Master Direction – Reserve Bank of India (Credit Information Reporting) Directions, 2025: https://www.rbi.org.in/ |

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions