CIBIL Score Dispute: How to Correct Report Errors

A CIBIL score dispute is a free process where you ask the credit bureau to correct a factual mistake on your credit report, like a closed loan showing as active or a payment marked late by error. It only works for genuine errors, not for accurate but unflattering entries.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

KEY TAKEAWAYS

A CIBIL score dispute can only fix genuine errors, not accurate entries you simply don't like.

Credit bureaus and lenders are expected to resolve disputes within the timelines prescribed under applicable RBI guidelines.

If unresolved past 30 days, you're entitled to Rs. 100 compensation per day of delay.

Common errors include wrong account status, incorrect balance, unfamiliar loan accounts, and wrong personal details.

Your CIBIL report must be less than 60 days old to raise a fresh dispute on it.

What Is a CIBIL Score Dispute?

A CIBIL score dispute is a formal, free request you file with the bureau asking them to correct something on your credit report that is factually wrong. This could be a loan you closed two years ago that still shows as active, a payment you made on time that got marked late, or an account that isn't even yours.

Here's the distinction that trips up a lot of people, and it's the one thing worth understanding before you file anything: a dispute only works for errors, not for entries that are accurate but simply unflattering. If you genuinely missed an EMI six months ago and it's showing correctly on your report, that isn't something a dispute can remove, because there's nothing factually wrong to correct. The bureau isn't in the business of erasing accurate history, only fixing incorrect ones.

One practical detail matters here, too. It's best to use your latest CIBIL report when raising a dispute so you're working with the most up-to-date information available.

If your copy is older than that, pull a new one first, since disputing an outdated report can slow the whole process down or create confusion about what's actually current.

What Kind of Errors Can You Dispute on Your CIBIL Report?

A handful of error types show up most often, and knowing which one you're dealing with helps you file a clearer, faster dispute.

- Wrong personal details. Your name, PAN, or date of birth showing incorrectly can sometimes point to a mix-up with someone else's file.

- Account shown as active after closure. A loan or credit card you paid off and closed still appears as open or outstanding.

- Wrong outstanding balance. The amount shown doesn't match what you actually owe or have paid.

- Unfamiliar account or enquiry. A loan, card, or hard enquiry you don't recognise at all, which can sometimes signal an identity issue worth taking seriously.

- Wrongly marked as a late payment. An EMI you paid on time is showing up as delayed or missed.

How to Raise a CIBIL Dispute Step by Step

The process is the same regardless of which bank or NBFC reported the error, and it doesn't require any paid help to complete.

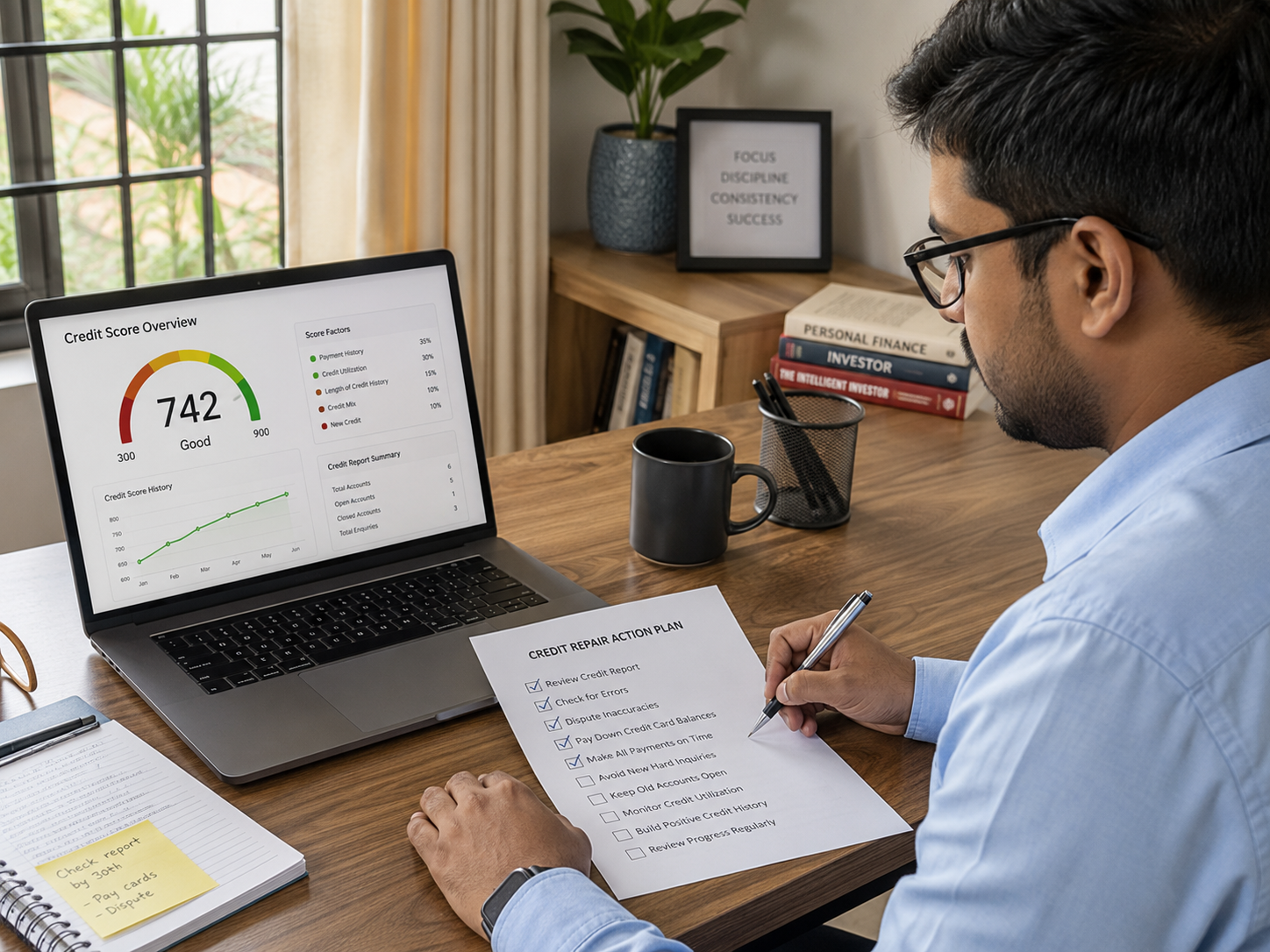

Start by downloading your latest CIBIL report directly from cibil.com. Go through it line by line and mark the exact error, the specific account, the exact wrong detail, and why it's incorrect. This step matters more than people expect. A dispute that says "something is wrong with my report" takes far longer to resolve than one that says "this specific credit card account shows a balance of Rs. 40,000, but I closed it in March with a zero balance."

Once you've identified the error clearly, gather whatever proof supports your claim, a closure letter, a bank statement, a payment receipt, anything that backs up what you're saying. Then file the dispute online through CIBIL's own dispute portal. This costs nothing and needs no agency involvement.

After you submit the dispute, you can track its status through your CIBIL account. If you don't see progress within the timelines prescribed under applicable RBI guidelines, follow up with the reporting bank and the credit bureau for an update.

FREED Expert Tip

Point to the exact account number and error type when filing your dispute. Clear, specific information makes it easier for the credit bureau and lender to review your request.

Check your full reportWhat Proof Do You Need for a CIBIL Dispute?

Supporting documents help the credit bureau and lender review your dispute more effectively.

. What you need depends on the error type, but a few documents cover most cases.

A loan closure letter from your bank proves an account should no longer show as active. A bank statement can confirm a payment you made on time, directly contradicting a wrongly marked late payment. A payment receipt works the same way for a specific EMI or settlement amount in question. If the error involves your personal details, name, PAN, or date of birth, your ID proof, Aadhaar or PAN card gives the bureau something concrete to match against.

Filing a dispute with a vague description and no attached proof is one of the most common reasons resolutions get delayed or the dispute gets rejected outright. The bureau and the bank both need something to verify against, and a clear document does that job far more effectively than a written explanation alone.

How Long Does a CIBIL Dispute Take to Resolve?

The total resolution window is 30 days, split between two parties. The bank or NBFC that reported the disputed information gets 21 calendar days to respond and confirm or correct it. CIBIL then has a further 9 calendar days to update the report based on that response. Together, that's the full 30-day window you should expect from the date you file.

It's worth setting realistic expectations here. This isn't an instant fix, and a dispute filed today won't reflect on your report tomorrow. Even once the bank confirms the correction, it takes CIBIL a few more days to actually update the report and reflect it to you visibly.

If the dispute genuinely isn't resolved within that 30-day window, you may be entitled to compensation of Rs. 100 for each day of delay beyond it.This compensation isn't automatic, though; it typically needs to be claimed through the dispute or complaint process rather than assumed.

What the Law Says

RBI rules give credit institutions 21 days and bureaus 9 days to resolve a dispute, adding up to 30 days in total. Delay beyond that window entitles you to Rs. 100 compensation per day.

Get My Free AssessmentWhat If Your CIBIL Dispute Is Rejected or Ignored?

If your dispute comes back rejected, or simply goes quiet with no update past the 30-day window, there's a clear next step rather than starting over from scratch.

First, follow up directly with the bank or NBFC that reported the disputed information, since they're the ones who need to confirm or correct it on their end before CIBIL can update anything. Keep a record of every communication, dates, reference numbers, and responses, since you'll need this if the issue escalates further.

If the bank still doesn't resolve it, or you believe the rejection itself was unfair, the RBI Ombudsman is the next level of escalation available to you. This is a free, formal grievance channel specifically set up for exactly this kind of unresolved financial services complaint.

Will Fixing a CIBIL Error Actually Improve Your Score?

It depends entirely on what the error was, and it's worth being honest about that rather than promising a guaranteed jump. Some corrections genuinely move your score. Others don't change it at all.

Correcting a wrongly active closed loan or an incorrect outstanding balance may affect your credit profile if the error was influencing your report. On the other hand, correcting a wrong personal detail, like a misspelt name or a wrong date of birth, often has no real effect on the number itself, since these details don't feed into the score calculation the way account status and payment history do.

The honest answer is that a dispute fixes what's inaccurate, and the score moves only if that inaccuracy was actually part of what was pulling it down in the first place. Anyone promising that every correction guarantees a specific point jump is setting an expectation that the bureau's own calculation doesn't support.

What If Your Low Score Isn't From an Error at All?

Everything above works when the problem is a genuine mistake in your report. But if you've gone through your report carefully and everything on it is accurate, real missed EMIs, a genuine default, an account correctly marked written off, then a dispute simply won't help, because there's nothing factually wrong to correct.

In that situation, the real issue isn't your report; it's the underlying debt itself, and that calls for a different kind of solution entirely. FREED's Credit Insights provides your Experian-based credit report, highlights the factors affecting your credit profile, and helps you understand whether you're dealing with a reporting error or an underlying debt issue.

If the issue is unpaid debt rather than a reporting error, disputing your credit report may not resolve it. Depending on your financial situation, options such as debt consolidation or settlement may be worth understanding separately.

Get Your Full Credit Picture, Not Just a Score

See exactly what's helping or hurting your CIBIL score.

Check your score nowGetting a CIBIL Dispute Resolved, Step by Step

Download Your Latest CIBIL Report

Get your report from cibil.com. It must be less than 60 days old to raise a fresh dispute against it.

Mark the Exact Error

Note the account number, the specific section, and the exact wrong detail. A precise description moves faster than a general complaint about "something being off."

Collect Supporting Proof

Gather loan closure letters, bank statements, or ID proof matching the specific error type. Documentation is what actually gets a dispute resolved, not just the description alone.

File the Dispute Online

Use the official CIBIL dispute portal directly. Avoid third-party sites or agencies claiming to file the dispute on your behalf, since this step needs no middleman and costs nothing to do yourself.

Track and Follow Up

Check your dispute status through your CIBIL account regularly. If there's no movement after 30 days, follow up directly with the reporting bank rather than waiting further.

Sources

Claim in Blog | Source |

Credit institutions have 21 calendar days and credit bureaus have 9 calendar days to resolve a dispute (30 days total), with Rs. 100 per day compensation for unresolved delays beyond that | RBI circular RBI/2023-24/72, Framework for compensation to customers for delayed updation/rectification of credit information, dated October 26, 2023: https://rbi.org.in/Scripts/NotificationUser.aspx?Id=12554&Mode=0 |

Unresolved complaints can be escalated to the RBI Ombudsman | RBI, The Reserve Bank – Integrated Ombudsman Scheme, 2021: https://www.rbi.org.in/commonman/english/scripts/PressReleases.aspx?Id=3340 |

Note: The 60-day report validity window for filing a fresh dispute and typical score-recovery impact after a correction are bureau-side operational conventions rather than codified RBI figures, and are stated as "typically" or general guidance in the blog body rather than listed here as sourced facts.

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions