CIBIL Score Complaint: How to File & Escalate | FREED

A CIBIL score complaint is a formal request you raise with TransUnion CIBIL to fix an error in your credit report. It covers things like a paid loan still showing as active, a wrong default mark, or an account you never opened. CIBIL has to look into it and resolve it within 30 days, and filing is free.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

KEY TAKEAWAYS

A CIBIL score complaint is what you raise to correct a real error in your credit report, and CIBIL must resolve it within 30 days.

CIBIL errors are more common than most people think. Ensure this is backed by internal data or clearly identified as FREED's own experience.

A single incorrect entry may affect how future lenders assess your credit profile.

Under RBI circular RBI/2023-24/72, if your complaint is not resolved in 30 days, you are entitled to ₹100 for each day of delay.

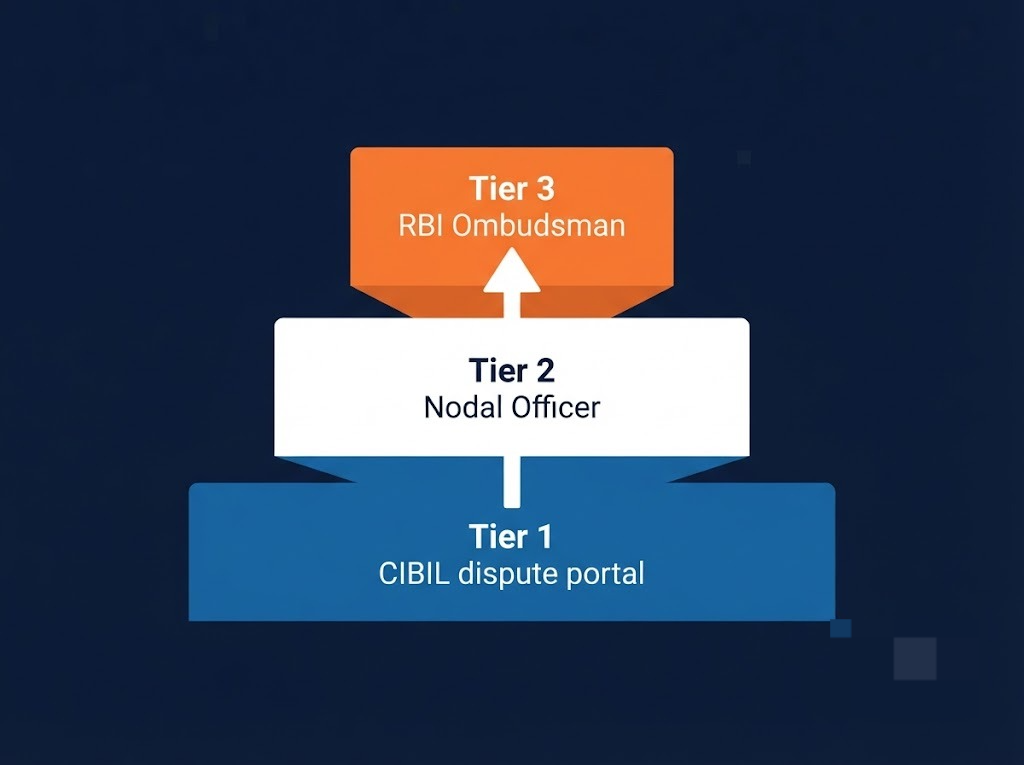

If CIBIL or your bank rejects the complaint, you have a clear escalation path: the bank's grievance officer, then CIBIL's nodal officer, then the RBI Ombudsman. Every step is free.

What Is a CIBIL Score Complaint and When Should You File One?

People use the words "dispute" and "complaint" as if they mean the same thing. In practice, they are two stages of the same fight.

A dispute is your first attempt. You spot a wrong entry in your report, you raise it online, and you wait for CIBIL and your bank to correct it. Most errors get fixed at this stage.

A complaint is what you escalate to when the dispute does not work. Maybe the bank rejected your correction. Maybe nobody responded. Maybe 30 days passed and nothing changed. That is when you move from simply "raising a dispute" to formally pushing the matter up the ladder and, if needed, to the regulator.

A CIBIL complaint is not only for typos. A reporting error may influence how future lenders assess your credit profile

And the stakes are real. A single false default can pull a healthy score down by 50 points or more. For a borrower waiting on a home loan or a personal loan, that drop can be the difference between an approval and a flat rejection. So if a dispute has stalled, do not let it sit. Escalate.

If you have not raised the first dispute yet, start there. Our guide on how to fix wrong entries on your credit report walks through that first step in detail.

What Are the Most Common Errors That Lead to a CIBIL Score Complaint?

Most complaints come from a short list of repeat offenders. Knowing which one you are dealing with matters, because the proof you need is slightly different for each.

- A closed loan still showing as open. You repaid and closed the loan, but the report still shows it as live. You will need your closure letter or clearance letter (called NOC).

- Paid EMIs marked as missed. You paid on time, but the report shows a late or missed payment. Your bank statement showing the debit is your proof.

- "Settled" showing after full repayment. If you repaid the full amount, the correct mark is "Closed", not "Settled". A wrong "Settled" mark hurts your score and needs correcting with your payment proof.

- An account you never opened. This can point to fraud or identity theft. You will need your PAN card copy and a statement that the account is not yours.

- Duplicate accounts. Duplicate entries may misrepresent your outstanding liabilities and could affect a lender's assessment. That alone can get a fresh application rejected.

- Wrong personal details. A mismatched name, date of birth, or PAN can mix your record with someone else's.

- Hard enquiries you did not authorise. Hard enquiries become part of your credit history and may be considered by future lenders during credit assessments.

Each of these is a valid reason to raise a dispute, and then a complaint if the fix does not happen.

FREED Expert Tip

Before you file, pull a fresh report directly from cibil.com. CIBIL only accepts disputes on a report less than 60 days old, so an older report will not be accepted.

Check your optionsHow to File a CIBIL Score Complaint Online

The whole process is online, and it is free. Follow these steps in order.

- 1

Pull your latest report from cibil.com.

Work off current data, not an old download. Read it carefully and find the exact entry that is wrong, whether it is a balance, a status, an account, or a personal detail.

- 2

Gather the proof that matches the error.

For a paid loan showing active, keep your closure letter or NOC ready. For a missed payment mark, your bank statement showing the payment. For an account you never opened, your PAN copy and a short declaration.

- 3

Log in to your CIBIL account and open the Dispute section.

First-time users have to register on cibil.com before they can raise anything.

- 4

Fill out the dispute form with exact details.

Select the specific field that is wrong, describe the correct information plainly, and attach your documents. Add your bank account details too, because that is where any delay compensation would be credited.

- 5

Submit and note down your dispute ID.

Save this ID the moment you get it. It is your reference for every follow-up from here on.

- 6

Track the 7-day updates and the 30-day window.

CIBIL sends an email update every 7 days while your dispute is active, and an SMS once it is resolved. The full resolution target is 30 days: 21 days for the bank to respond, and 9 days for CIBIL to process after that.

- 7

Do not apply for new credit during this window.

Every fresh loan or card application adds a hard enquiry, and that can slow down the verification you are waiting on.

What Happens After You File the Complaint?

Once you submit, the file does not just sit inside CIBIL. Here is the back-end you cannot see.

CIBIL forwards your complaint to the bank or NBFC that reported the entry. That bank gets 21 calendar days to respond. If the bank confirms the error, CIBIL corrects your report and sends you a notification. Your score usually reflects the change 5 to 7 days after the correction.

If the bank says its data is right, CIBIL notifies you that the complaint was rejected, along with the reason. This is the part most people do not realise: CIBIL cannot change your report on its own. It can only update the entry after the bank that submitted the data confirms the correction.

That single fact explains why some complaints stall. The bank points at CIBIL, CIBIL points at the bank, and the borrower is stuck in the middle. When that happens, you are not out of options. You are simply at the point where escalation begins. And there is a deadline working in your favour, which the law spells out clearly.

What the Law Says

Under RBI circular RBI/2023-24/72 (dated 26 October 2023), a CIBIL complaint must be resolved within 30 calendar days. If it is not, you are entitled to ₹100 for every day of delay, credited to your bank account within 5 working days of the resolution. This is why CIBIL asks for your bank details when you file.

Learn About RBI's 30-Day CIBIL RuleWhat Should You Do If Your CIBIL Complaint Is Rejected or Unresolved?

A rejection is not the end of the road. Most rejections happen for one simple reason: the bank said its data was correct, and the borrower's evidence was not strong enough to force a change. So you work up the ladder, one clear route at a time.

Route 1: Re-raise the dispute with stronger proof. Do not just resubmit the same thing. Send your closure letter, your payment proof, and your NOC together, as one solid packet. Weak, single-document disputes get rejected. Complete ones often get reversed.

Route 2: Write to your bank's grievance officer directly. The wrong data came from the bank, so go to its source. Write to the bank or NBFC's grievance redressal officer, quote your dispute reference number, and attach your proof. Banks are required to respond to a written complaint within 30 days before you can escalate further.

Route 3: Escalate inside CIBIL to the nodal officer. If the bank route stalls too, take it up with CIBIL's nodal officer. You can use the escalation desk on cibil.com or email nodalofficer@transunion.com. Always include your dispute ID and a short history of what has happened so far. If the nodal officer does not resolve it, CIBIL has a Principal Nodal Officer above that level as well.

Work these in order. Each step builds the paper trail you will need if the matter goes all the way to the regulator.

Debt on your report causing a score problem?

If the entry is a genuine one and the underlying debt is the real issue, talk to FREED's team. One call, no pressure, clear answers on where you actually stand.

Book My Free CallHow to Escalate a CIBIL Complaint to the RBI Ombudsman

This is the final step, not the first. You only reach it after the bank and CIBIL's nodal officer have both failed, or after you have been wrongly denied the delay compensation you were owed.

The RBI's Integrated Ombudsman Scheme is a free, government-backed way to complain about a regulated entity. Credit information companies like TransUnion CIBIL have been covered under it since 1 September 2022, so a CIBIL grievance now qualifies. Before you approach the Ombudsman, you must have first complained to CIBIL and either waited 30 days with no proper reply or been rejected. That earlier paper trail is exactly why the dispute IDs and grievance IDs matter.

You can file in two ways. Online, through the RBI complaint portal at cms.rbi.org.in, which is the faster route. Or by post, as a signed letter to the Centralised Receipt and Processing Centre, Reserve Bank of India, Central Vista, Sector 17, Chandigarh 160017.

Whichever route you pick, include everything: your dispute ID, the grievance ID from your CIBIL escalation, a clear description of the specific error, and the full history of your earlier communication. The Ombudsman can direct the correction and can award compensation if it was wrongfully denied to you. There is no fixed resolution date, so timelines vary by case, but the process costs you nothing.

How to File a CIBIL Score Complaint

- 1

Get your latest CIBIL report from cibil.com.

The report must be less than 60 days old. Older reports are not accepted for complaints.

- 2

Identify the specific error and gather proof.

Collect your bank statement, payment receipt, NOC, or closure letter, whichever matches the error you found.

- 3

Log in to your CIBIL account and open the Dispute section.

First-time users need to register on cibil.com before they can raise a complaint.

- 4

Fill out the dispute form with exact details.

Select the field that is wrong, describe the correct information, and attach your documents. Add your bank details for any delay compensation.

- 5

Submit and note down your dispute ID.

This ID is your reference for every follow-up. Save it the moment you get it.

- 6

Wait for CIBIL's update within 30 days.

You will get email and SMS updates every 7 days. Do not apply for any new credit during this window.

- 7

Escalate if it is rejected or ignored.

Go to the bank's grievance officer, then CIBIL's nodal officer, then the RBI Ombudsman if needed.

CIBIL Complaint vs. RBI Ombudsman: When to Use Which

Factor | CIBIL Complaint | RBI Ombudsman |

When to use | First step for any report error | Only after CIBIL and the nodal officer have failed |

Time to resolve | 30 days (mandated by RBI) | No fixed timeline; varies by case |

Cost | Free | Free |

How to file | cibil.com dispute portal | cms.rbi.org.in or a letter to Chandigarh |

If delayed | ₹100 per day after 30 days | Can award compensation for a wrongful denial |

Documents needed | Error-proof, payment receipts, NOC | All prior dispute IDs, grievance IDs, full correspondence |

Read the table as a sequence, not a choice. You almost always start with the CIBIL complaint and only move to the Ombudsman if that path is exhausted. The Ombudsman is your backstop, not your opening move.

Sources

Claim in blog | Verified source (opened and confirmed) |

30-day resolution (21 days bank + 9 days CIBIL); ₹100 per day of delay; credited within 5 working days | RBI circular RBI/2023-24/72, DoR.FIN.REC.48/20.16.003/2023-24, 26 Oct 2023 — rbi.org.in |

CIBIL can only update a report after the reporting bank confirms; 30-day limit | Section 21(3), CICRA 2005 and Rule 20(3)(c), CIC Rules 2006 (as set out in the above RBI circular) |

Credit information companies covered by the RBI Integrated Ombudsman Scheme since 1 Sept 2022; file at cms.rbi.org.in or CRPC Chandigarh | RBI Integrated Ombudsman Scheme (CIC inclusion, w.e.f. 1 Sept 2022); RBI complaint portal — cms.rbi.org.in |

CIBIL nodal officer email; 60-day report rule; 7-day status updates; escalation ladder | TransUnion CIBIL Consumer Grievance Redressal Policy and Contact page — cibil.com/contact |

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions