Business Loan for CIBIL Defaulters: What Are Your Real Options?

Business loans for CIBIL defaulters can be challenging, but NBFCs, gold loans, and government schemes offer alternative funding options for low credit scores.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

A CIBIL score below 650 makes traditional bank approval for business loans very unlikely but NBFCs, gold loans, and secured options remain accessible.

Many small business owners carry both business credit problems and overdue personal loans or credit card debt both must be assessed together.

Applying for more credit while overdue personal loans are unresolved often makes the overall financial situation worse, not better.

NBFCs may approve business loans for lower CIBIL scores but at significantly higher interest rates the real cost must be calculated before committing.

Fixing the underlying personal debt burden before applying for new business credit is often the smarter path and more likely to result in approval.

What Does "CIBIL Defaulter" Mean for a Business Loan Applicant?

"CIBIL defaulter" isn't an official legal term. No government list exists. It's how people informally refer to anyone whose CIBIL score (the number that tracks your full loan history) has dropped below 600–650 because of missed EMIs or loan payments.

For a business loan application, this matters in two ways. First, banks and NBFCs (non-bank loan companies) check your personal CIBIL score when you apply. Second, if your business is registered as a company, they may also look at your CIBIL Rank, the business credit score used for company-level assessments. Most small business owners and sole proprietors are assessed primarily on their personal CIBIL score. The two are deeply linked.

This means a default on a personal loan or credit card can directly block a business loan application even if your business is doing well and generating steady income.

Many genuine situations cause defaults. Delayed client payments. A health emergency. A few months of lost income. None of these make someone a bad person or an unreliable borrower. They make someone who went through a rough patch.

Understanding what "CIBIL defaulter" actually means and what it doesn't is the first step to knowing what options you still have.

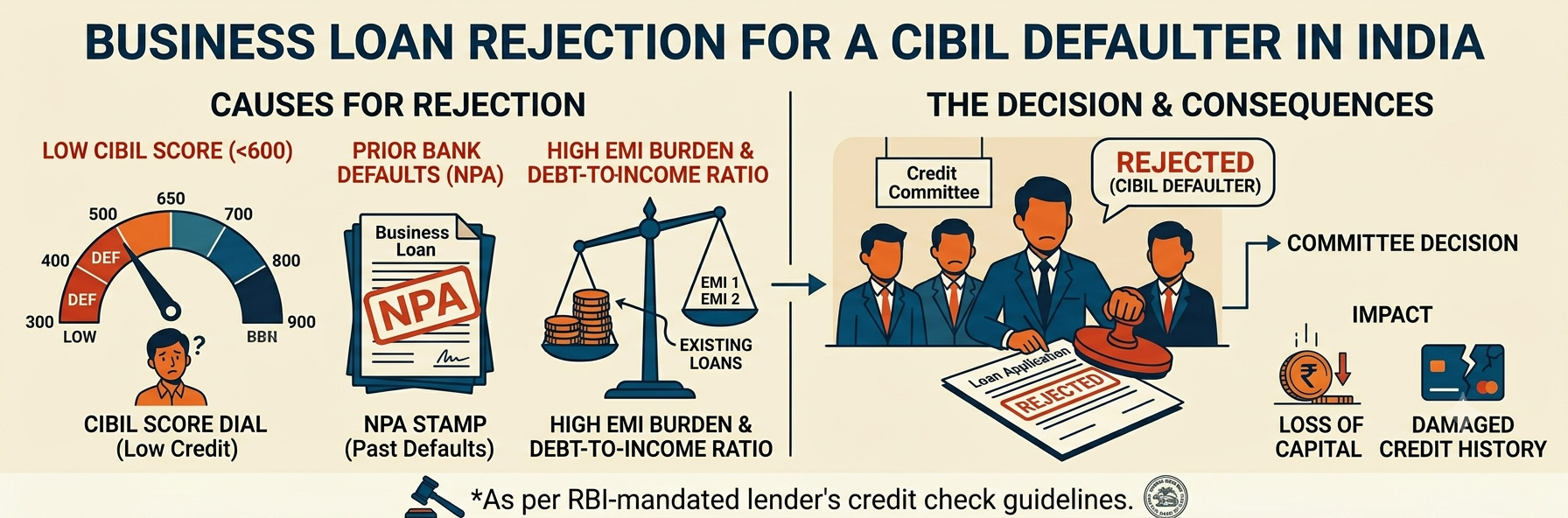

Why Do Banks Reject Business Loans for CIBIL Defaulters?

Banks use your CIBIL score as a primary filter because unsecured business loans carry high risk. There's no collateral for the bank to recover if repayment fails. A past default signals that repayment broke down before regardless of the reason behind it.

Here's what a bank's system actually checks:

Score threshold. Many traditional banks generally prefer higher CIBIL scores for unsecured business loans. for unsecured business loans. Applications below that threshold are often rejected automatically.

Negative entries on the report. If your CIBIL report shows entries marked "Settled," "Written-off," or NPA (loan marked as bad by the bank, usually after 90 days of missed EMI), these are visible to every lender who pulls your report.

High EMI burden. If your existing personal loan EMIs already consume more than 50% of your income, banks consider further lending too risky. It doesn't matter how strong your business looks.

Short business vintage. Most banks want 2–3 years of operating history before they consider a business loan application. A new or informal business adds to the risk picture.

This reflects how lenders evaluate repayment risk internally. It's following a risk model. Knowing that model helps you figure out where you have room to work with.

Business Loan Options Available for CIBIL Defaulters in India

Traditional banks for unsecured business loans are largely off the table when your CIBIL score is below 650. But several other paths exist. None of them are without cost or risk. Here's what each one actually involves.

Secured Business Loan (Property or Machinery as Collateral) If you own property, machinery, or another fixed asset, you can pledge it as collateral. Because the bank has something to recover, your CIBIL score matters less. The trade-off: the lender may recover the pledged asset if repayment obligations are not met under SARFAESI Act 2002 (the law that lets banks take and sell pledged property on a secured default without going to court first).

Gold Loan The most accessible option for most people. Fast processing, minimal paperwork, no CIBIL check in most cases. You pledge gold; the bank lends against its value. The limitations: short repayment tenure, relatively high interest rates against the principal, and your gold is at risk if you can't repay.

Loan Against Property (LAP) Larger amounts, longer tenure than a gold loan. But this is a secured loan like a home loan or car loan which means secured assets may be recoverable under SARFAESI provisions if the loan becomes overdue if the loan becomes NPA (loan marked as bad by the bank). Be clear on that before signing.

NBFC Unsecured Business Loan NBFCs (non-bank loan companies) have more flexible CIBIL thresholds than traditional banks. Some may consider lower-score applications depending on income and business profile.. But interest rates are significantly higher. Calculate the total repayment amount over the full tenure not just the monthly EMI before committing.

MUDRA Loan (Government-Backed) The Pradhan Mantri MUDRA Yojana (MUDRA, a govt-backed small business loan scheme) offers loans in three tiers: Shishu (up to ₹50,000), Kishore (up to ₹5 lakh), and Tarun (up to ₹10 lakh ). No strict CIBIL minimum. Worth exploring for small-ticket business needs. Apply through a bank or NBFC registered under the scheme.

Co-Applicant or Guarantor Route Adding someone with a clean repayment record to your application improves approval chances significantly. But that person carries full liability for the loan if you can't repay. This is a real commitment for them. It shouldn't be taken lightly on either side.

None of these paths are risk-free. Each one comes with a real cost.Higher interest, pledged assets, or liability for someone who trusted you. Understand the full picture before you choose.

FREED Expert Tip

Before applying for any business loan, download your free CIBIL report at cibil.com. Check which accounts are showing as NPA, Settled, or overdue and dispute any errors with the bureau before they block your application.

How to Check Your CIBIL Score: A Step-by-Step GuideThe Hidden Problem Personal Debt Blocking Your Business Loan

This is the part most articles skip. And it's often the real reason a business loan gets rejected.

Many small business owners and self-employed individuals searching for a business loan are already carrying overdue personal loans, credit card debt, or both. That personal debt is sitting on the same CIBIL report the bank checks for your business loan application. The bank doesn't separate the two.

If your total EMIs personal and business combined already consume more than 50% of your income, no bank or NBFC will approve additional credit. Not because your business is failing. Because the numbers say you're already at the limit.

Here's what that means practically: the path to a business loan may run through your personal debt first.

Resolving overdue personal loans doesn't have to mean paying everything at once. A repayment arrangement, a revised EMI schedule, or in cases where repaying in full becomes genuinely difficult loan settlement as a last resort can reduce active default entries on your report and improve how lenders may evaluate your profile over time.

Settlement is not something a borrower chooses out of preference. Banks and financial companies only consider it when you are in a genuine financial difficulty and are truly unable to repay the full amount. It is a last resort, not a shortcut.

FREED works specifically on personal unsecured debt overdue personal loans, credit cards, and loan app debt. If your CIBIL situation includes these, FREED can assess the full picture, identify what is manageable, and where genuine inability to repay is identified, help support communication and documentation with the bank on your behalf.

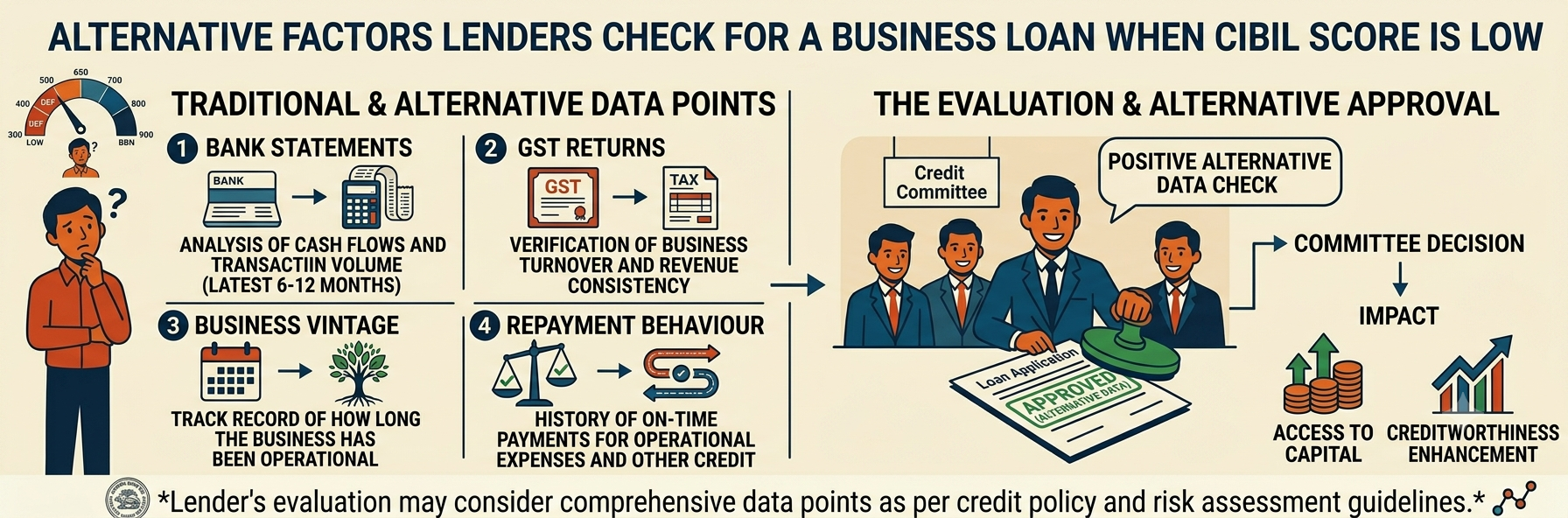

What Lenders Actually Look at Beyond Your CIBIL Score

Your CIBIL score is not the only number a lender checks. Many NBFCs and newer fintech lenders use alternative assessment models. If your score is low, these factors can work in your favour or against you.

Bank Statement Health Six to twelve months of consistent business turnover in your current account is a strong signal. It shows active operations. Strong business cash-flow records may support the overall application review with many NBFCs.

Business Vintage Most lenders require at least 2 years of operating history. A business registered recently is considered higher risk, regardless of how well it's doing now.

GST Returns and ITR Filings Up-to-date GST returns and ITR (income tax return the annual income proof filing required for self-employed individuals) are increasingly accepted as income proof. Most NBFCs weigh these heavily when CIBIL score is low. Gaps or late filings raise questions.

Existing Bank Relationship If you've held an active current account with a bank for several years, that institution may offer more flexibility than one you approach cold.

Age of the Default A default from 4 years ago is viewed differently than one from 6 months ago. Older defaults carry less weight especially if repayment behaviour has improved since. CIBIL records older than 7 years are not factored into your current score at all unless there is an active default.

Whether Overdue Loans Have Been Addressed A borrower who has settled or restructured a past default and resumed on-time payments is viewed more favourably than one with ongoing active defaults. Lenders can see the timeline. Engagement matters.

How to Improve Your Chances of Getting a Business Loan After Default

These are concrete steps. Do them in order. Don't skip to step 4 before steps 1 and 2 are done.

Step 1 Check Both Your Personal CIBIL Report and Business Credit Download your free CIBIL report at cibil.com. Check every account marked NPA, Settled, or overdue. Dispute any errors directly with the bureau before applying anywhere. Errors on your report can affect how lenders assess your application..

Step 2 Address Any Overdue Personal Loans First Even a partial repayment or a formal restructuring arrangement (changing the loan plan to a new schedule with your bank) reduces active default entries. A bank or NBFC looks much more favourably on a borrower who has engaged with their existing debt than one who has gone silent.

Step 3 Keep GST Returns and ITR Filings Current Up-to-date GST returns and ITR filings are your most credible income proof as a self-employed borrower. Lenders weigh these heavily when your CIBIL score is low. Long gaps in filings may create concerns during lender evaluation. that no CIBIL score can fix.

Step 4 Start With Secured Options First A gold loan or a loan against FD (fixed deposit) carries no CIBIL requirement in most cases. Using these for short-term business needs while you rebuild your score is a lower-risk path than an unsecured NBFC loan at high interest.

Step 5 Do Not Apply to Multiple Lenders at Once Every application creates a hard enquiry on your CIBIL report. Multiple hard enquiries in a short period drop your score further and signal desperation to the next lender who checks. Avoid submitting multiple applications within a short period while rebuilding your profile.

Step 6 Resolve Personal Debt Before Taking on Business Credit If overdue personal loans or credit card dues are pulling your score down, resolving those first through repayment, a revised loan plan, or where repaying in full becomes genuinely difficult, loan settlement as a last resort is may improve future credit eligibility over time. FREED offers free assessments to help you understand what is manageable and what options exist.

What the Law Says

Under SARFAESI Act 2002, banks may recover pledged collateral through SARFAESI provisions in certain secured-loan default situations for secured loans without going to court if the loan becomes NPA. This applies to secured loans like home loans, car loans, and Loan Against Property not to unsecured personal or business loans

Borrower Rights in India: What the Law ProtectsBusiness Loan Options for CIBIL Defaulters What Each Path Involves

About FREED

FREED is India's first debt relief company, founded in 2020 and headquartered in Gurugram. FREED works with individuals who are unable to repay unsecured loans, personal loans, credit cards, BNPL products, and loan apps and negotiates loan settlement with banks and NBFCs on their behalf. FREED charges fees only when a settlement is successfully completed. FREED does not handle secured loans (home loans, car loans, gold loans, Loan Against Property) and does not facilitate business loans or business credit.

If your CIBIL situation includes overdue personal loans or credit card debt, FREED can assess the full picture and tell you clearly what options exist.

India's leading debt resolution platform

FREED is India's leading platform for debt settlement and financial wellness. We have helped over 60,000 Indians reduce, manage, and get completely out of debt the right and legal way.

Media Mentions