Zero CIBIL Score Loan App: What Works, What to Watch Out For, and How to Borrow Safely

A zero CIBIL score is not a bad score. It means TransUnion CIBIL has no data to calculate one. The bureau shows this as NH (No History) or NA (Not Applicable). You have not borrowed before, so lenders have little or no repayment history to assess.Several loan apps in India are built for exactly this profile: they check income, bank statements, and repayment capacity instead of a CIBIL score. But not all of them are safe.

Mohit Juneja

Reviewed by FREED India, Debt Resolution Specialists

KEY TAKEAWAYS

Zero CIBIL score (shown as NH or NA) means no credit history exists, not bad credit. It is a blank slate, not a red flag.

The Ministry of Finance has clarified that lenders cannot reject first-time borrowers solely because their credit history is missing.

Fintech NBFCs and digital lending apps use alternative data, bank statements, salary slips, UPI history, to assess zero-CIBIL borrowers.

Unregulated loan apps targeting zero-CIBIL borrowers have charged effective annual interest rates between 200% and 700% in documented cases.

RBI's Digital Lending Apps directory, live since July 2025, lets any borrower verify whether a lending app is regulated before downloading it.

Using a legitimate loan app that reports to a recognised credit bureau, combined with consistent on-time repayment, can help establish a credit history over time.

What Does Zero CIBIL Score Actually Mean?

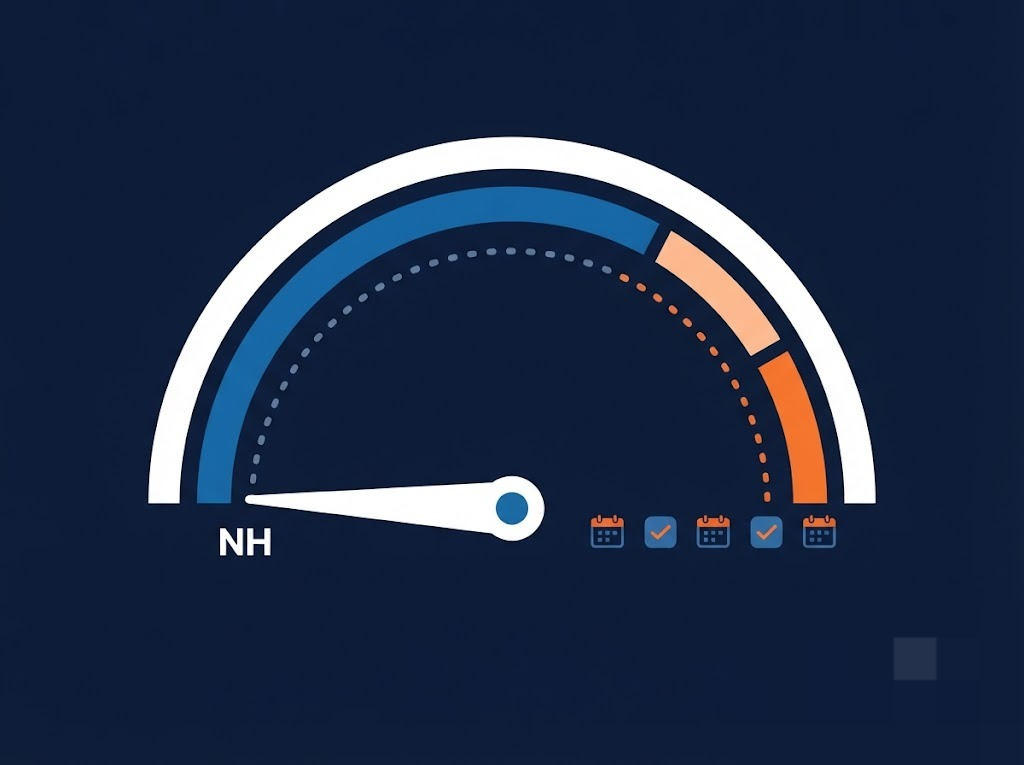

CIBIL scores usually range from 300 to 900. NH and NA sit completely outside this range, they're a separate category, not a low number on the same scale.

NH (No History) means you have never taken a loan or credit card. CIBIL simply has no data on you at all.

NA (Not Applicable) means you do have some credit activity, but it's less than 6 months old, not enough yet for the bureau to calculate a score.

Neither is a penalty. Think of it like a job interview with no work experience listed on the CV. The interviewer can't judge your past performance, but that doesn't mean you'll perform badly. It just means there's nothing to look at yet.

This is an important distinction to hold onto: a zero score is not the same as a score of 300, which would actually mean poor credit behaviour. Zero means unknown, not risky.

In India, industry estimates suggest roughly 7 in 10 credit-eligible adults don't actively use formal credit products, according to TransUnion CIBIL research, which means a large share of the population remains credit invisible or credit underserved. This is an industry estimate rather than an official government figure, but the takeaway holds: you are far from alone in this. The Ministry of Finance has also clarified that lenders cannot reject first-time borrowers solely because of NH or NA status. (source link- https://newsroom.transunioncibil.com/more-than-160-million-indians-are-credit-underserved/)

FREED's Credit Insights, which pulls your Experian report, also covers new-to-credit profiles, so you can check exactly where you stand before applying anywhere.

So who exactly has zero CIBIL, and how do loan apps reach them?

Who Has a Zero CIBIL Score in India?

Being new to credit is far more common than it feels. Here's who typically falls into this category.

Students aged 18 and above who have never held a credit card or loan. Fresh graduates in their first job, with income now but no borrowing history yet. Self-employed individuals running cash businesses who have never used formal credit, even though they may manage large sums of money regularly.

Homemakers who have never held a loan or card in their own name, often because household finances ran through a spouse's accounts. Young professionals who moved from cash payments to UPI and digital payments but have still never formally borrowed anything.

There's also a less obvious group: people who were previously credit-active but have been inactive for 24 to 36 months. If there's been no credit activity in that window, the score can revert to NH or NA, even for someone who once had an established score.

Gen Z accounts for 41% of first-time borrowers in India today, and millennials make up roughly 45% of personal loan borrowers, often taking their first loans for lifestyle needs, home improvement, or starting a business. If any of these describe you, this is a normal starting point, not something to feel behind on.

FREED Expert Tip

Before applying to any loan app, check your Experian credit report via FREED's Credit Insights. It shows whether you are NH, NA, or already building a score, which tells you exactly which apps you qualify for and what interest rates to expect.

Check your Credit InsightsHow Do Loan Apps Assess Zero CIBIL Score Borrowers?

Legitimate fintech NBFCs and digital lending apps don't simply skip credit checks. They replace the missing score with other signals that tell a similar story about your ability to repay.

The most common signal is 3 to 6 months of bank statements, used to understand your income regularity and cash flow. For self-employed applicants, salary slips or GST returns serve a similar purpose.

Apps also look at UPI and digital payment history, which shows spending patterns and financial discipline even without a formal loan on record. Aadhaar and PAN verification confirms identity, while employer type and income stability help the lender judge how consistent your earnings are likely to be.

A co-applicant with a stronger credit profile may improve eligibility, subject to the lender's assessment.

It's worth being precise here: saying these apps do "no CIBIL check" is a slight simplification. Most RBI-registered apps do pull a credit report as part of the process. They simply find NH or NA on file, and then lean more heavily on the alternative signals above to make their decision.

For a first loan under this model, expect amounts in the range of ₹5,000 to ₹50,000 from most fintech NBFCs. Larger amounts typically become available only after you've built some repayment history with them.

What Should You Look for in a Safe Loan App for Zero CIBIL Score?

This is the section worth reading most carefully. Before you download or apply to any loan app, run through this checklist, it takes under 5 minutes.

1. The app must name its NBFC or bank lending partner clearly, either in the app itself or in its terms. If no lender name appears anywhere, that's a red flag on its own.

2. Verify the partner on the RBI Digital Lending Apps directory, live at rbi.org.in since July 2025. Search the lender's name there before proceeding.

3. The app must give you a Key Fact Statement (KFS) showing the actual Annual Percentage Rate (APR), processing fees, and penalty terms, before you accept the loan, not after.

4. Disbursement must go only to your bank account. Loans routed through a wallet or handed over in cash are not how regulated lending works.

5. The app should never ask for access to your contacts, photos, or messages. Legitimate lenders have no legitimate need for this kind of access.

6. Watch the repayment tenure. A 7 to 15 day repayment window is a warning sign. RBI-regulated products typically offer tenures of at least a few months.

RBI's working group identified over 600 fake or suspicious loan apps back in 2021 alone, and documented cases reported in mid-2026 show unregulated apps charging effective interest rates that, in illustrative instances, reached 200% to 700% per year. These are examples from reported cases, not a fixed range. The checklist above exists precisely because of apps like these.

What the Law Says

Under RBI's Digital Lending Directions, 2025, any lending app must clearly name its regulated NBFC or bank partner, provide a Key Fact Statement before disbursement, and disburse funds only to the borrower's bank account. Apps that skip these steps are non-compliant.

Know Your Digital Lending Rights

What Are the Risks of Using a Loan App Without a CIBIL Score?

Even with a legitimate app, there are real trade-offs worth understanding upfront.

Higher interest rates are the most immediate one. Since the lender has no repayment history to judge you by, rates for zero-CIBIL borrowers from legitimate apps tend to run noticeably higher than standard personal loan rates. As an illustrative market example, Jupiter Money's research pegged these at around 18%, running up to 36% or more per year. Actual rates vary by lender and change over time, so always check the Key Fact Statement before accepting any offer.

Smaller loan amounts are common too, until you've built some track record with the lender.

The bigger risk is predatory targeting. Zero-CIBIL borrowers are specifically sought out by illegal apps precisely because they're credit-invisible and often in urgent need of quick money.

This can spiral into a debt cycle. A ₹5,000 loan from an unregulated app, with a 7-day repayment window and a 15% to 30% upfront processing fee, can balloon into a ₹25,000 obligation within weeks if it's rolled over or re-borrowed to cover the shortfall. A survey cited by BusinessToday in 2026 found that 72% of distressed borrowers from digital loan apps had faced harassment from recovery agents.

Here's a point worth sitting with: the supposed benefit of using a loan app to build your CIBIL score only holds if that app actually reports your repayment to a licensed bureau. If the app is unregulated and reports to no one, paying on time, every time, does nothing at all for your score. You'd be taking on the interest and the risk with none of the credit-building upside.

How Can FREED Help a Zero CIBIL Score Borrower?

FREED's role here depends on where you actually stand, not every zero-CIBIL situation needs the same kind of help.

If you're just starting out and want to know where you stand, FREED's Credit Insights pulls your Experian report and tells you clearly whether you're NH, NA, or already building a score. This is often the most useful first step, since it tells you which loan apps you're likely to qualify for and what rates to expect, before you apply anywhere and rack up unnecessary hard enquiries.

If you've taken a few app loans from legitimate, RBI-registered lenders and your EMIs are now stacking up, more than 50% of your take-home salary going toward repayments is a sign the load has gotten heavier than it should be. Debt Consolidation may combine eligible debts into a single EMI, depending on the approved loan terms.

If you're genuinely unable to repay what you owe on legitimate loans, and it's reached a point where full repayment isn't realistically possible, FREED's Debt Resolution Program can help. Settlement is not something a borrower chooses out of preference, it only comes into play when banks and financial companies recognise a genuine inability to repay.FREED helps borrowers settle their unpaid/overdue loans at up to 50% less*. FREED negotiates with your banks through a structured savings process to bring down what you owe by up to 50%*. This does affect your credit report, but for someone in real hardship, it's a controlled way out rather than an unmanaged spiral.

If your debt is from an unregulated or illegal app, FREED's programs don't cover this directly, since these apps fall outside the regulated lending system entirely. The right path here is the cybercrime portal at cybercrime.gov.in, the RBI's Sachet portal, and your local police, since debt from an illegal lender carries no legal enforceability to begin with.

If harassment has started, from a legitimate lender's recovery process turning abusive, or from an illegal app using your contacts against you, FREED Shield helps you understand your rights and can assist in preparing a complaint through the appropriate channels.

The short version: know your status first, then match the help to your actual situation, rather than assuming one fix covers everything.

*Rates and ranges shown are indicative. Final terms decided by the bank. FREED is not a Loan Provider. No outcome is guaranteed. Please verify directly with your bank.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

How Do You Use a Loan App to Build a CIBIL Score from Zero?

Used responsibly, a legitimate RBI-registered loan app is actually one of the fastest ways to build a CIBIL score from nothing.

Start by choosing an app whose NBFC partner reports to at least one licensed bureau, CIBIL, Experian, Equifax, or CRIF High Mark. Verify this before you apply, most RBI-registered apps do report, according to Jupiter Money, but it's worth confirming.

Borrow a small amount you can comfortably repay from your existing income. Don't stretch yourself for a bigger amount than you need.

Repay every EMI before or on the due date. Every on-time payment becomes a positive entry on your credit record, this is the whole mechanism that builds your score from zero.

Once repaid, wait 30 to 45 days and check your report. You should start to see a score appear where NH or NA used to sit.

Don't apply to multiple apps at once. Each application creates a hard enquiry, and multiple enquiries in a short window can actually pull down a score that's just starting to form.

Once you've built a consistent repayment record on an app loan, you'll typically be in a better position to move toward a more formal credit product, a secured credit card or a small personal loan from an NBFC. How long that takes varies entirely by individual profile, since each on-time payment adds to the history lenders and bureaus see, but no fixed number of payments guarantees any particular score.

Got trapped in an app loan debt cycle?

Talk to FREED's team. One call, no pressure, honest answers.

Book My Free Call

How to Borrow Safely from a Loan App with Zero CIBIL Score

- 1

Check your credit report before applying.

Use FREED's Credit Insights or visit cibil.com to confirm your NH or NA status. This tells you exactly where you stand before any application, so you're not guessing.

- 2

Verify the app's NBFC or bank partner.

The lender's name must appear clearly in the app or its terms. If it isn't named anywhere, that's your cue to stop and look elsewhere.

- 3

Check the RBI Digital Lending Apps directory.

Visit rbi.org.in and confirm the app is listed, this directory has been live and mandatory for authorised digital lenders since July 2025.

- 4

Read the Key Fact Statement before accepting.

The app must show you the actual APR, processing fees, and penalties before you accept the loan. If it skips this step, treat it as non-compliant and move on.

- 5

Borrow only what you can repay from your current income.

Borrow only an amount that comfortably fits within your monthly repayment capacity. Starting small protects you from a debt trap and still builds your credit record just as effectively.

- 6

Repay on time, every time.

Each on-time repayment is a positive entry on your credit report. Check your credit report after the lender has had reasonable time to report your repayment information.

- 7

Check your credit report 45 days after repayment.

Confirm the repayment has been reported correctly. If something looks off, raise a dispute at cibil.com right away rather than letting it sit.

Safe vs. Predatory Loan App: How to Tell the Difference

Feature | Safe (RBI-Registered) App | Predatory or Illegal App |

Lender named in app | Yes, NBFC or bank name clearly visible | No, vague, unnamed, or fake name |

RBI Digital Lending Apps directory | Listed (verifiable at rbi.org.in) | Not listed |

Key Fact Statement before disbursement | Yes, APR, fees, penalties disclosed upfront | No, terms revealed only after acceptance |

Repayment tenure | Minimum few months, structured EMIs | 7 to 15 days, designed to trap |

Contact list access requested | No | Yes, often used for harassment if unpaid |

Disbursement method | Directly to bank account | May use wallets or cash |

Bureau reporting | Reports to at least one licensed bureau | No reporting, does not build CIBIL score |

Interest rate range | 18% to 54% per year (legitimate) | 200% to 700% effective APR (documented) |

The table makes one thing obvious once you lay it out: almost every marker of safety is something you can check yourself, in the app or on rbi.org.in, before you ever hand over your PAN or Aadhaar. None of it requires special expertise, just five minutes and a willingness to check before you borrow.

Sources

Claim | Source |

RBI's Digital Lending Apps directory has been operational since July 1, 2025 | RBI / PIB press release on Digital Lending Apps directory and cybercrime reporting mechanisms (pib.gov.in) |

Digital lending apps must provide a Key Fact Statement and disburse funds only to the borrower's bank account | Reserve Bank of India (Digital Lending) Directions, 2025, issued May 8, 2025 (rbi.org.in) |

Data collected by lending apps must be purpose-specific and consent-based, with mobile contact/gallery access barred outside one-time KYC needs | Reserve Bank of India (Digital Lending) Directions, 2025 (rbi.org.in) |

Note: Interest rate ranges for zero-CIBIL borrowers (Jupiter Money), the 200% to 700% effective APR figure for unregulated apps (BusinessToday, June 2026), the 41%/45% first-time borrower demographic split, and the Airtel Finance data on score-building timelines are industry and media data points, not RBI regulation, and are left out of the table above per sourcing rules. These are phrased as "typically" or "documented cases" in the body rather than as guaranteed figures.

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions