What is a Debt Cycle? Insights and Effective Management Tips

Paying one loan with another? Using your credit card to pay your credit card bill? That's a debt cycle and millions of Indians are trapped in one right now. Here's how to recognise it and break free.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

A debt cycle is when you keep borrowing more money just to pay off existing debt — and the total amount keeps growing, not shrinking.

Most people don't enter a debt cycle through carelessness. They enter through life events — job loss, medical emergencies, rising costs — without a safety net.

The clearest warning sign: paying only the minimum due on credit cards every month. The debt barely reduces while interest keeps compounding.

Breaking the cycle requires three things: stopping new borrowing, prioritising high-interest debt, and getting a structured plan in place.

FREED has helped over 10,000 Indians break out of debt cycles through consolidation, settlement, or a combination of both.

What is a Debt Cycle?

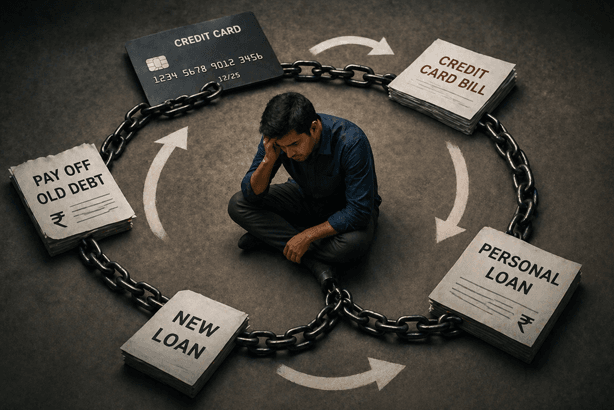

A debt cycle is a pattern where you keep borrowing to pay off what you already owe — and the debt never actually reduces. It just moves around.

Here's a simple example of how it works:

You owe ₹40,000 on a credit card. You can't pay it all. So you pay the minimum ₹2,000. The remaining ₹38,000 carries forward with 38% annual interest adding ₹1,200 in interest that month. Your outstanding is now ₹39,200. Next month you repeat.

Meanwhile, your rent went up. Groceries cost more. An unexpected bill arrived. You swipe the credit card again.

Now you owe ₹45,000. Next month you take a small personal loan to manage it. Now you have two EMIs.

That is a debt cycle. You are borrowing to survive not to progress. And the total amount owed is growing, not shrinking despite your payments.

According to recent data, household debt in India rose to 42.9% of GDP in June 2024 — up significantly from 36.6% in just three years. The rise of digital credit, buy-now-pay-later apps, and instant personal loans has made it easier than ever to borrow — and easier than ever to fall into a cycle.

How Does Someone End Up in a Debt Cycle?

Most people in debt cycles are not careless. They are people reacting to financial pressure without the right tools or knowledge.

It often starts with one event. A medical emergency. A job loss. A business slowdown. An unexpected large expense with no savings to cover it.

The credit card or personal loan feels like a solution. It covers the immediate need. But repayment starts the following month and it doesn't fit comfortably into the budget.

So the minimum is paid. Interest accumulates. The outstanding grows. Another need arises. Another swipe. Another loan.

Before long, multiple EMIs are consuming most of the monthly income. There's no room to save. Any new emergency goes straight to the credit card again. The cycle is now self-sustaining.

This is not a character flaw. It is a structural financial problem, one that gets harder to escape the longer it runs.

Common Triggers of a Debt Cycle in India

- 1

Over-reliance on unsecured credit

Credit cards and instant personal loans are easily available and aggressively marketed. When they become the primary way to manage monthly expenses rather than a tool for planned spending they quickly become unmanageable. Drag Credit card interest of 36–42% per year means your debt grows very fast if not cleared monthly. Using credit for daily expenses groceries, petrol, medicines is

- 2

Income not keeping up with rising costs

Salaries in many sectors have not kept pace with inflation. Rent, school fees, food, medical costs all have gone up significantly in recent years. When expenses rise but income doesn't the gap gets filled with credit. That credit comes with EMIs that make the next month even tighter.

- 3

No emergency fund

When a sudden expense hits car repair, hospital visit, appliance breakdown and there's no savings buffer, the credit card is the only option. One emergency becomes one more debt. The cycle begins.

- 4

Not seeing the full debt picture

₹5,000 EMI on one card. ₹3,000 on another. ₹4,500 personal loan EMI. ₹2,000 app loan. Each feels manageable in isolation. Together that's ₹14,500 per month going to debt. On a ₹30,000 salary, that's nearly 50% of income. The combined picture is very different from the individual loans.

- 5

Using one loan to pay another

This is the classic debt cycle trap. Taking a new personal loan to pay off a credit card. Taking a payday loan to make an EMI. The total debt doesn't reduce — it just moves to a different lender, often at a higher rate.

How a Debt Cycle Affects Your Mental Health

This part is rarely talked about but it's very real.

Living in a debt cycle is not just a financial problem. It is a mental health problem.

The constant calculation — "Can I afford this?" The anxiety before every due date. The shame of hiding the situation from family. The sleepless nights. The inability to focus at work. The constant background stress that never fully goes away.

Research consistently shows that financial stress is one of the leading causes of anxiety and depression in India. People in debt cycles often describe feeling trapped, helpless, and ashamed even though their situation has very common, understandable causes.

You are not alone in this. Millions of Indians are in the same situation across every income level, every city, every profession.

And recognising the emotional weight of debt is the first step to taking it seriously and doing something about it.

How to Break Free - Step by Step

Breaking out of a debt cycle is possible. It requires clarity, a plan, and consistency. Here's exactly what to do:

Step 1: See the Full Picture - Write Down Every Debt

You cannot manage what you don't see clearly.

Write down every loan and credit card you have. For each one:

- Lender name

- Total outstanding amount

- Monthly EMI or minimum due

- Interest rate

- Payment due date

Add it all up. That total number, however uncomfortable, is your starting point. Once you see it clearly, you can build a plan.

Step 2: Stop All New Borrowing - Immediately

This is the hardest step. And the most important.

You cannot break a cycle by continuing to borrow. Every new loan or credit card swipe adds to the total. Even if it feels like it solves the immediate problem - it makes the underlying one worse.

Draw a firm line: no new loans, no new credit card purchases for daily expenses, until you have cleared at least 70–80% of your existing debt.

Switch to cash, debit, or UPI for all daily spending. If the money isn't in your account - don't spend it.

Step 3: Prioritise High-Interest Debt First

Not all debt is equally expensive. Credit cards at 36–42% per year are the most expensive. Personal loans from app-based lenders can be even higher.

These are the ones eating your money fastest. Every month you carry a credit card balance - a significant portion of your payment goes to interest, not to the actual debt.

Put all extra money towards your highest-interest debt first. Pay minimums on everything else. Once the most expensive debt is cleared - redirect that money to the next most expensive.

This is the Avalanche Method. It is mathematically the most efficient way out.

Step 4: Explore Debt Consolidation

If you have multiple loans - managing them separately is expensive and confusing. Debt consolidation combines them into one single loan with one lower EMI, often at a reduced interest rate.

Example: 4 loans with combined monthly payment of ₹18,000 at high interest rates. After consolidation - one loan, ₹12,000/month, lower interest. Simpler. Cheaper. More manageable.

Consolidation works best when your CIBIL score is still above 650 and you can still afford to repay -just need it structured better.

FREED's Debt Consolidation Program handles this end-to-end.

Step 5: Talk to Your Lenders Early

Many people going through a debt cycle avoid calls from their bank. That makes things worse.

Contact your lender proactively. Explain your situation. Ask about:

- EMI restructuring - lower monthly payment over a longer tenure

- Temporary moratorium - a short pause on payments

- Interest waiver on accumulated penalties

Banks prefer negotiating to chasing defaults. They have hardship programs but they don't advertise them. You have to ask.

Step 6: Build Even a Tiny Emergency Fund

The debt cycle often restarts because of one unexpected expense with no savings to cover it.

Even ₹500–₹1,000 saved per month in a separate account builds a buffer. After 6 months ₹3,000–₹6,000. Not a lot. But enough to handle small emergencies without reaching for the credit card again.

This breaks the cycle at its most vulnerable point - the unexpected expense.

What the Law Says

Under RBI's Fair Practices Code, lenders must offer borrowers facing genuine financial hardship a fair and transparent resolution process including the possibility of loan restructuring. If you approach your bank in writing and explain a genuine hardship situation and they refuse to engage or offer any relief, you can escalate this to the RBI Banking Ombudsman at cms.rbi.org.in for free. You have a right to a fair resolution process.

Read your full borrower rights under RBI guidelinesHow Long Does Recovery Take?

There's no single answer - it depends on your total debt and what you can pay monthly.

Here's a realistic guide:

When to Get Professional Help

Try the steps above first. Many people can break their debt cycle with discipline and a clear plan.

But if:

- Your total EMIs and debt payments exceed 50% of your monthly income

- You've already missed multiple payments and collection calls have started

- You've tried to manage but the interest keeps growing faster than you pay

- You feel completely overwhelmed and don't know where to start

- it's time to call FREED.

Professional help is not a weakness. It's a smart move when the situation is genuinely beyond self-management.

How FREED Helps You Break the Debt Cycle

FREED offers two structured programs for people in debt cycles:

Debt Consolidation - for people who can still repay but have multiple EMIs making the situation unmanageable. FREED combines everything into one lower EMI through our lending partners.

Debt Resolution (Settlement) - for people who have already defaulted or genuinely cannot repay the full outstanding amount. FREED negotiates with your lenders to settle for significantly less than what you owe. On average, clients settle at 56% less than the original amount.

Both programs include:

- A dedicated relationship manager who handles all creditor communication

- FREED Shield protection from recovery harassment

- Budget guidance to prevent the cycle from starting again

- Full transparency at every step - no hidden fees, no surprises

We don't just help you get out of the current cycle. We help you build the habits that prevent the next one.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

About FREED

FREED is India's first and leading Debt Relief Platform. We help people who are overwhelmed by credit card bills, personal loans, and EMIs including those stuck in debt cycles find a legal, stress-free path to becoming debt-free.

We offer Debt Consolidation (one lower EMI for multiple loans) and Debt Resolution (settle for less when you genuinely can't repay in full). We protect you from recovery harassment through FREED Shield — trusted by over 15,00,000 Indians.

Over 10,000 Indians have broken their debt cycle with FREED's help.

No complicated language. No hidden charges. No judgement. Just honest, practical help.

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions