Recovery of Debts and Bankruptcy Act 1993: What Borrowers Must Know

The Recovery of Debts and Bankruptcy Act 1993 is an Indian law that set up special courts called Debt Recovery Tribunals (DRTs special courts that handle only bank debt cases) to help banks and NBFCs (non-bank loan companies) recover large unpaid loans. It was created so that debt cases would not get stuck in regular civil courts for years. If a bank files a case against you under this law, you have legal rights including the right to be heard, to contest the claim, and to seek a settlement even after the case is filed.

FREED India

Reviewed by FREED India, SEO Intern

Key Takeaways

The Recovery of Debts and Bankruptcy Act 1993 set up Debt Recovery Tribunals (DRTs) special courts for banks to recover large unpaid loans faster than regular courts could.

DRT cases generally apply to loan amounts above Rs. 20 lakhs writer must verify current threshold before publishing.

Receiving a DRT notice is serious but not the end of the road. You have the legal right to respond, contest, and even negotiate a settlement during proceedings.

Ignoring a DRT notice can result in an ex-parte (one-sided decision without hearing your side) order passed against you.

An OTS (one-time settlement, paying once and the matter ends) can be negotiated at any stage, including after a DRT case is filed, under the RBI's June 2023 Compromise Settlement Framework.

What Is the Recovery of Debts and Bankruptcy Act 1993?

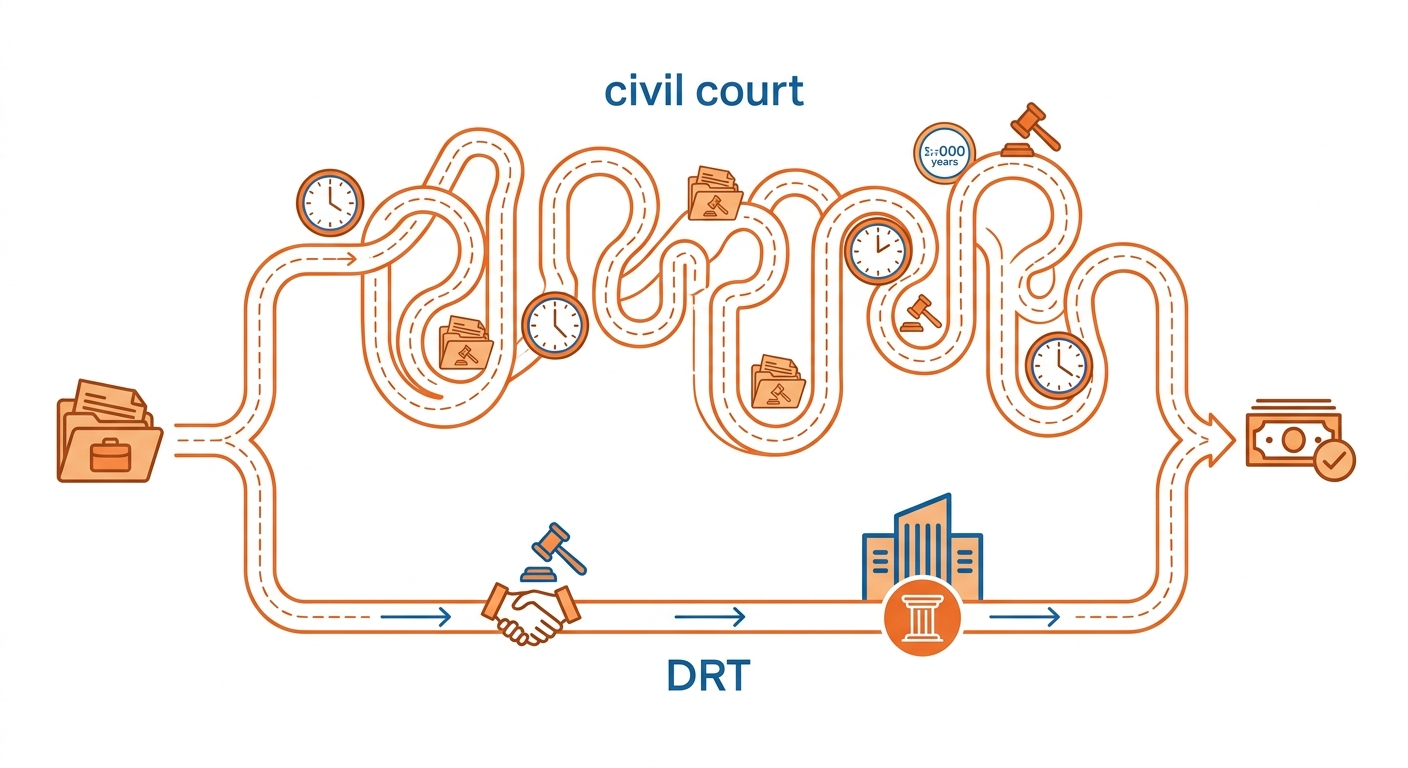

Before 1993, if a bank wanted to recover an unpaid loan, it had to file a case in a regular civil court. Civil courts were handling thousands of cases, property disputes, contract fights, family matters. Bank debt cases often took many years to resolve in regular civil courts. Banks were sitting on crores of unpaid loans with no practical way to recover them quickly.

The government created the Recovery of Debts Due to Banks and Financial Institutions Act in 1993 specifically to fix this. It set up Debt Recovery Tribunals (DRTs) courts that handle only bank and NBFC debt recovery cases. After the Insolvency and Bankruptcy Code (IBC) came in 2016, the Act was renamed to include "Bankruptcy" and was updated to align with the new insolvency framework.

This is a civil law. It is not about arresting borrowers or treating default as a crime. It is a legal process that gives both sides the bank and you a structured forum to present their case and get a decision.

There are currently 39 Debt Recovery Tribunals and 5 Debt Recovery Appellate Tribunals (DRATs the higher court that hears appeals against DRT orders) operating across India.

Does the RDB Act 1993 Apply to Your Personal Loan?

This is the question most borrowers need answered first.

The DRT route is used when the total outstanding amount with a single bank or NBFC crosses the threshold; most sources put this at Rs. 20 lakhs. Writer note: verify official figure. If your personal loan with one bank is above this amount and has been declared NPA (loan marked as bad by the bank usually after 90 days of missed EMIs), that bank may file a DRT case.

If your personal loan is below this threshold, the bank does not use the DRT route for recovery. Instead, it may send recovery agents, issue legal notices, or file a case under Section 138 of the NI Act (cheque bounce law; this one can go criminal if you gave post-dated cheques). For smaller amounts, some banks also file cases in civil courts.

One important clarification: if you have loans with 3 different banks, say Rs. 5 lakhs with one, Rs. 8 lakhs with another, and Rs. 4 lakhs with a third, these are not added together for DRT purposes. Each bank counts separately. None of them individually crosses the threshold, so DRT does not apply in that case.

For most individual borrowers with personal loans from loan apps or small NBFCs, the DRT route is not what they are facing. But that does not mean recovery pressure is lighter. It means different rules other recovery processes such as notices or civil proceedings may apply instead.

Knowing which route your bank is likely to take helps you prepare the right response.

What Happens When a Bank Files a Case Under This Act?

Here is the process, step by step.

The bank files something called an OA (Original Application, the formal case document) with the DRT. This includes the loan details, the amount claimed, and the history of missed payments. The DRT reviews it and, if accepted, issues a summons to you. That summons is the DRT notice you receive.

You have 30 days from the date of the summons to file a written response. Writer note: verify this exact period from the RDB Act and DRT Rules. This is your chance to put your side of the case on record.

If you do not respond, the DRT can pass an ex-parte order, a final decision made entirely in your absence, without hearing your side. Once that happens, a Recovery Certificate can be issued. The Recovery Officer then executes it, which can include attaching (freezing or seizing) your bank accounts or other assets.

If you do respond, the case proceeds with hearings. Both sides present their case. The DRT then passes an order. If the bank wins at this stage, the same Recovery Certificate process follows but you have had a fair hearing, you have placed your defence on record, and you still have the right to appeal.

If you want to challenge the DRT's final order, you can appeal to the DRAT (Debt Recovery Appellate Tribunal, the higher court for DRT appeals). That appeal must be filed within 45 days of the DRT order. Writer note: verify this timeline from the Act. Filing an appeal before the DRAT typically requires depositing 50% of the debt amount, though the DRAT has discretion to reduce or waive this. Writer note: verify exact mechanics from the Act.

Responding in time is the single most important thing you can do. Responding early gives you more opportunities to present your side and explore possible resolutions..

- 1

Step 1 Receive and Read the DRT Summons

Don't ignore it. Read the notice carefully it will state the case number, the amount claimed, and the date by which you must respond.

- 2

Step 2 Note Your Deadline to Respond

You have 30 days from the date of the summons to file your written response before the DRT. Missing this deadline can mean the case is decided without your input.

- 3

Step 3 Gather Your Loan Documents

Collect your loan agreement, all EMI payment records, bank statements, and any communications with the bank. These form the basis of your response.

- 4

Step 4 File a Written Response

You or your legal representative can file a written statement of defence contesting the amount claimed, the NPA classification, or any procedural errors by the bank. The DRT must hear your side before passing any final order.

- 5

Step 5 Explore Settlement at Any Stage

Banks and financial companies only consider it when you are in a genuine financial difficulty and are truly unable to repay the full amount. But if that is your situation, an OTS (one-time settlement paying once and the matter ends) can be negotiated even after a DRT case is filed. The RBI's June 2023 Compromise Settlement Framework specifically allows this.

What the Law Says

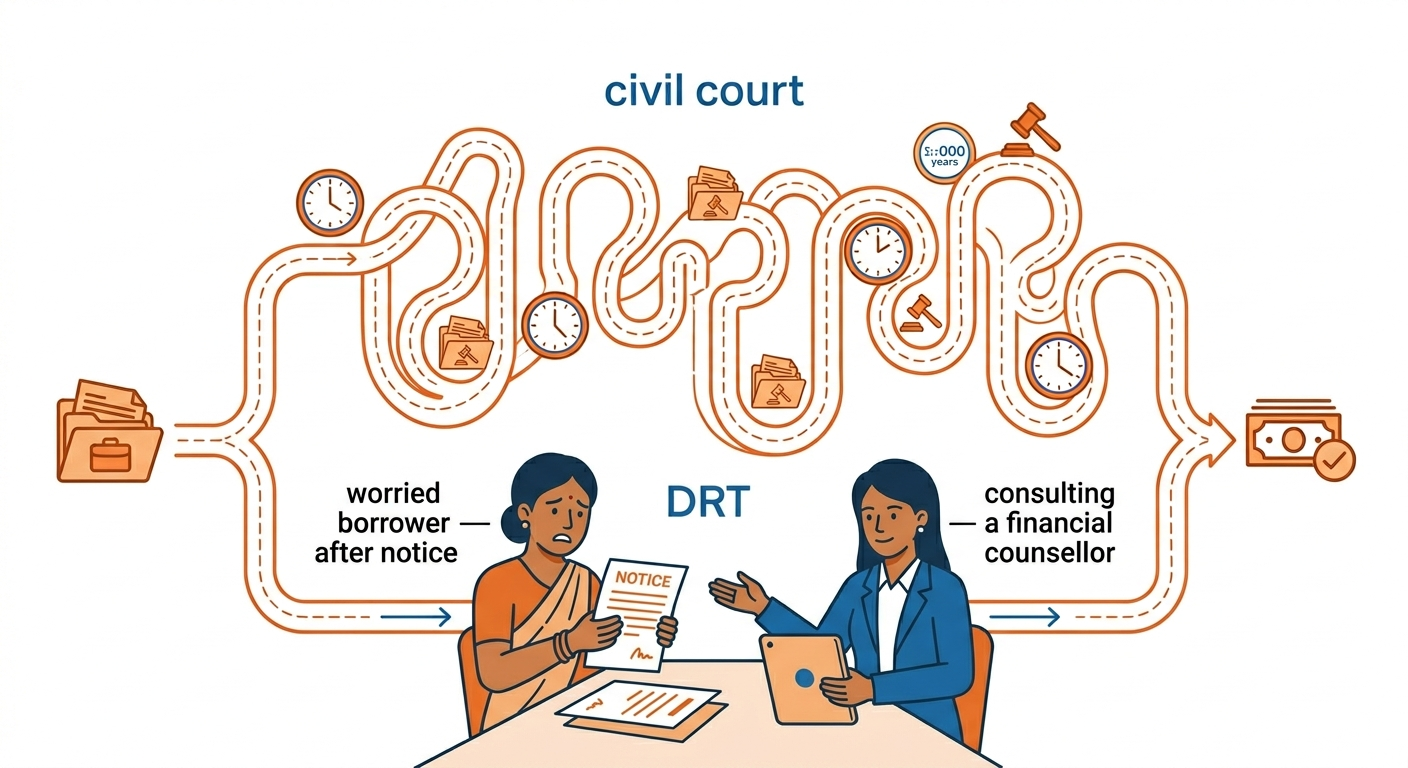

If you receive a DRT summons, don't wait. The 30-day response window is tight. Getting help early legal or financial gives you far more options than waiting until an order is already passed.

Get Legal Help NowWhat Are Your Rights as a Borrower Under This Act?

Most content about the RDB Act is written from the bank's side. Here is what the law gives you.

1. The right to be heard. The DRT cannot pass a final order against you without giving you a fair hearing as long as you have responded to the summons. That response is what keeps this right active.

2. The right to contest the NPA classification. Banks follow a specific RBI process before declaring a loan NPA. If that process was not followed correctly, you can challenge the classification itself, not just the amount.

3. The right to appeal. A DRT order can be appealed before the DRAT within 45 days. Writer note: verify timeline from the Act. This is a real option, not just a formality.

4. The right to seek settlement at any stage. You can request an OTS at any point before the DRT order, during proceedings, or even after a Recovery Certificate is issued. The RBI's June 2023 Compromise Settlement Framework makes this explicit.

5. The right to protection from harassment. Even while a DRT case is running, RBI guidelines on recovery agent conduct apply. Recovery agents still cannot call at odd hours, threaten you, or contact your family or workplace improperly. Those rules do not pause because a DRT case is filed.

These are genuine legal protections. They are not guarantees of winning. But they are your rights and knowing them helps you use the

What the Law Says

Under the RDB Act 1993, a DRT cannot pass a final recovery order against a borrower who has properly responded to the summons without first conducting a fair hearing. Ignoring the summons removes this protection.

Know your borrower rightsWhat Are Your Options If a DRT Case Has Been Filed?

You have more options than most people realise.

Option 1: File a written defence and contest the case. If the bank made errors in the NPA classification, overstated the amount claimed, or did not follow the correct procedure, you can challenge this before the DRT. A legal adviser can help you identify if any of these apply.

Option 2: Seek interim relief from the DRT. If there is an urgent risk like your bank account being attached before the case is fully heard you can ask the DRT for a stay order (a temporary pause on that action) while proceedings are ongoing.

Option 3: Negotiate an OTS. Settlement is not something a borrower chooses out of preference. Banks and financial companies only consider it when you are in a genuine financial difficulty and are truly unable to repay the full amount. If that is your situation, OTS is possible at any stage of DRT proceedings even after a Recovery Certificate is issued, under the RBI's June 2023 Compromise Settlement Framework. This requires the bank's agreement. FREED's counsellors handle the financial side of this process preparing documents, helping organise documents and supporting communication during the process, and getting the settlement worded correctly.

Option 4 Appeal to the DRAT. If the DRT passes an order against you, you can appeal to the Debt Recovery Appellate Tribunal within 45 days. Writer note: verify timeline. The DRAT is an independent body and can reverse or modify the DRT's order.

None of these is automatic. Each requires action on your part ideally with proper legal and financial guidance. The important thing is that you are not out of options once a DRT case is filed.

What Does This Act Mean for Unsecured Personal Loans Specifically?

Most FREED borrowers carry personal loans and credit card dues unsecured debt (debt with no property or asset given as security to the bank). Here is what the RDB Act means for that situation specifically.

The DRT route is used when the outstanding amount with a single bank or NBFC crosses the threshold typically above Rs. 20 lakhs. Writer note: verify and state official figure. For individual personal loan borrowers, reaching that figure with a single bank in a single account is less common. But it does happen especially with large personal loans, or where interest and penalties have compounded over months of default.

For personal loans below this threshold, banks typically use recovery agents, legal notices, or civil court suits. Some banks use Section 138 of the NI Act (cheque bounce law this one can go criminal) if post-dated cheques were given. These routes are different from DRT but are not less serious.

If you have loans with multiple banks, say two personal loans and a credit card across 3 different banks each bank acts independently. There is no combined DRT case brought by all 3 banks together. Each one looks at its own outstanding amount.

For unsecured personal loans below the DRT threshold, the borrower's situation is governed by a different set of rules. FREED helps navigate both the DRT-level cases from the financial side, and the full range of unsecured loan distress situations regardless of amount.

What Should You Not Do If a DRT Case Is Filed Against You?

These are the things that make your situation worse. Not mistakes to judge you for just things to avoid from here on.

Don't ignore the summons. If you do not respond within the deadline, the DRT can pass an ex-parte order (decided without your side being heard). That is far harder to undo than filing a simple written response.

Don't make verbal agreements with bank officers. If any officer tells you "pay this amount and we will stop the case," get it in writing before you pay anything. Verbal assurances do not hold up in DRT proceedings.

Don't pay without a proper settlement letter. Partial payments without written confirmation of what they represent can complicate your case rather than help it.

Don't transfer assets to avoid attachment. This can create additional legal complications and is viewed seriously by courts.

Don't go to unregistered "debt settlement agents." Some unregistered operators may not provide legitimate or transparent support. Any legitimate help legal or financial should be from registered, traceable professionals. FREED is a registered financial company with a record of outcomes and a fee structure based only on successful settlement.

Talk to a FREED Counsellor, Free One call

Honest guidance on your situation and options.

Book My Free CallAbout FREED

FREED is India's first debt relief company, founded in 2020 and based in Gurugram. We work with people who have unsecured loans, credit cards, personal loans, BNPL, loan apps and are genuinely unable to keep up with their EMIs. We negotiate directly with banks and NBFCs on your behalf and charge fees only when a settlement is successfully completed.

We do not handle secured loans like home loans, car loans, or loans against property.

If you are dealing with a DRT notice or just starting to fall behind on EMIs, our counsellors can help you understand your options clearly, without judgment, and at no cost for the first conversation.

DRT vs Other Recovery Routes What Banks Use and When

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions