RBI Guidelines on Recovery of Loan: What Banks and Agents Can and Cannot Do

RBI guidelines on recovery of loan are the rules the Reserve Bank of India sets for how banks, NBFCs (non-bank financial companies), and their recovery agents can contact, visit, and take action against borrowers who've missed payments. These rules don't protect you from consequences; missed EMIs do have consequences. But they define exactly how far a bank can go. And they draw a hard line at harassment.

FREED India

Reviewed by FREED India, SEO Intern

Key summury

RBI guidelines on recovery of loan restrict agent contact to 8 AM–7 PM only; calls outside those hours are a documented violation

Loan default in India is a civil matter, not a criminal one; a borrower cannot be arrested for missing EMIs unless fraud is proven. [(Source: Supreme Court position confirmed across multiple rulings see leading case summary: https://www.leadindia.law/blog/en/loan-default-in-india-supreme-courts-guidance-and-your-legal-remedies-explained/)]

Banks remain responsible for ensuring recovery agents comply with applicable RBI guidelines under RBI Master Circular DBR.LEG.BC.21/09.07.005/2024-25

FREED helped 60,000+ customers navigate unsecured debt fees charged only on successful settlement

Over 9.34 lakh complaints were filed with the RBI Integrated Ombudsman in FY2023-24 — a 32.81% rise over the previous year. Loans and advances were the single largest grievance category. [(RBI Integrated Ombudsman Annual Report 2023-24, via Factly: https://factly.in/data-complaints-to-ombudsman-about-banking-related-loans-advances-more-than-tripled-in-five-years/)]

What Are the RBI Guidelines on Recovery of Loan and Why Do They Exist?

Banks have a legal right to recover money owed to them. Nobody disputes that. But without clear limits, recovery becomes harassment. And harassment sustained, threatening, humiliating was exactly what thousands of Indian borrowers reported facing before the RBI stepped in.

The RBI's Fair Practices Code (FPC) and its subsequent circulars set out binding rules for every bank, NBFC, and fintech loan app that the RBI regulates. The most current version is Master Circular DBR.LEG.BC.21/09.07.005/2024-25, issued in July 2024. These rules don't apply only to large public sector banks. They apply to every RBI-regulated entity which includes most banks, most NBFCs, and most digital lending apps operating in India today.

Three things these guidelines make clear:

First: who is covered. Every bank, NBFC, and fintech loan app regulated by the RBI must follow these rules. There is no carve-out for small NBFCs or digital lenders.

Second: who is responsible. When a recovery agent misbehaves, the bank is responsible, not the agent, not the outsourced recovery agency. Banks are expected to oversee the conduct of authorised recovery agents. RBI treats agent misconduct as the bank's own misconduct.

Third: what the RBI is balancing. The bank's legitimate right to recover dues versus the borrower's right to dignity, privacy, and fair treatment. Both are real rights. These guidelines are where that balance is drawn.

The RBI fined Bajaj Finance ₹2.5 crore specifically for persistent recovery agent harassment. That fine is a signal: these rules are enforced, not just written.

What Happens Step by Step When You Miss Loan Payments?

Most borrowers don't know what the recovery process actually looks like. So every call from an unknown number feels like a legal notice. Every visit from an agent feels like the beginning of an arrest. Understanding the actual sequence changes everything.

Recovery is phased. Each phase has a different set of rules. Here's what typically happens:

1. Day 1–30: Reminders only. SMS, email, automated calls. These are informational. No legal process has started. No agent visit is permitted. This is the bank nudging you to pay. [(RBI Fair Practices Code: https://www.rbi.org.in/scripts/NotificationUser.aspx?Id=12378&Mode=0)]

2. Day 31–60: Written notice issued. The bank sends a formal written notice. It states the outstanding amount, the payment schedule, and options that may include restructuring (changing the loan plan) or a moratorium (temporary pause). Read this notice carefully. Respond to it in writing.

3. Day 61–90: Recovery agent visits may begin. Agents must carry a valid ID card and a written letter of authorisation from the bank. They may visit your registered address during socially acceptable hours. They may not visit unannounced at a workplace without your written consent. [(RBI Fair Practices Code: https://www.rbi.org.in/scripts/NotificationUser.aspx?Id=12378&Mode=0)]

4. Day 91–180: NPA classification. After 90 days of non-payment, the loan is classified as an NPA a Non-Performing Asset (a loan the bank has marked as bad). This is a formal internal classification, not a court order. Formal legal escalation becomes possible at this stage.

5. After 180 days: Legal proceedings. For secured loans (where you pledged an asset), the bank may begin SARFAESI (Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act) proceedings but only after serving a 60-day written notice before any repossession. For unsecured loans above ₹20 lakh, the bank may file at the Debt Recovery Tribunal (DRT), a special government court for loan cases. For smaller unsecured amounts, civil court remains the option.

The window before Day 91 is your best window. Restructuring, moratorium, or hardship consideration are all more accessible before NPA classification. After that threshold, options narrow, but they don't disappear

What Can Recovery Agents Actually Do Under RBI Rules?

Most content on this topic only lists what agents cannot do. That creates a lopsided picture. Knowing what agents are actually permitted to do helps you spot what they're not allowed to do.

What agents CAN do:

- Call between 8 AM and 7 PM

- Send written notices

- Visit your registered address during socially acceptable hours

- Present their ID card and bank authorisation letter

- Discuss repayment options and outstanding amounts

- Accept payments against proper written receipts

What agents MUST have and do:

- Carry an RBI-compliant ID card and a written letter of authorisation from the bank

- Be certified by an RBI-authorised body

- Keep a record of every interaction with the borrower

What agents CANNOT do:

- Call before 8 AM or after 7 PM

- Improperly disclose your loan information to unrelated third parties.

- Reveal your loan details to any third party

- Use abusive, threatening, or humiliating language

- Impersonate police or court officials, this is a criminal offence under BNS (Bharatiya Nyaya Sanhita) Section 204 [(https://vakilsearch.com/bns/sections/204)]

- Visit your workplace without explicit written consent from you

- Collect cash without issuing a proper written receipt

- Access your phone contacts or share your data (this applies specifically to loan apps)

Understanding both sides of this list is useful. A borrower who knows what agents are allowed to do can recognise immediately when a line has been crossed.

What the Law Says

Under RBI Master Circular DBR.LEG.BC.21/09.07.005/2024-25, any misconduct by a recovery agent is treated as the bank's own misconduct. The bank cannot outsource its accountability. [(RBI notification:

Read more: freed.care/resources/rbi-guidelines-debt-recoveryWhat Is the Difference Between Secured and Unsecured Loan Recovery?

Most people searching this topic are dealing with personal loans, credit cards, BNPL (Buy Now Pay Later), or loan apps, not home loans or car loans. The recovery process for these two categories is very different.

- Secured loans (home loans, car loans, gold loans) involve an asset you pledged when you took the loan. If you default, the bank has legal recourse to that specific asset through the SARFAESI Act. But even then: a 60-day written notice must come first, and you have the right to appeal at the Debt Recovery Tribunal (DRT) before any repossession happens. This is a defined process, not an overnight seizure.

- Unsecured loans (personal loans, credit cards, BNPL, loan apps) are a different category entirely. You pledged nothing when you borrowed. The bank has no asset to point to. So the recovery path for these loans goes through recovery agent contact, written notices, and for amounts above ₹20 lakh a DRT filing or civil court.

For personal loans and credit cards, household goods, salary, and family assets cannot be seized without a court order. An agent has no police powers. Threatening to seize household goods violates both the RBI Fair Practices Code [(RBI/2022-23/108: https://www.rbi.org.in/scripts/NotificationUser.aspx?Id=12378&Mode=0)] and constitutes criminal intimidation under BNS Section 351. [(https://vakilsearch.com/bns/sections/351)]

FREED works only with unsecured loans: personal loans, credit cards, BNPL, and loan apps. We don't handle secured loan recovery.

Recovery Agents Calling? Know What You Can Do Next.

Free assessment. A counsellor will walk you through your options.

Get My Free AssessmentIs Loan Default a Criminal Offence in India?

This is one of the most searched questions from borrowers under recovery pressure and the question recovery agents exploit most aggressively.

The answer: loan default in India is a civil matter, not a criminal offence. A borrower cannot be arrested simply for missing EMIs on a personal loan or credit card. The Supreme Court of India has repeatedly upheld this position. [(https://www.credsettle.com/can-i-go-to-jail-for-loan-default-in-india)]

There are 3 narrow exceptions where criminal proceedings become possible:

1. Fraud during the loan application. If the loan was taken with fabricated documents, a false identity, or inflated income declarations, that's fraud. That is a criminal matter.

2. Cheque bounce. Under Section 138 of the NI Act (Negotiable Instruments Act law for cheque bounce cases), if you gave the bank a post-dated cheque for repayment and it bounced, criminal proceedings are possible.

3. Wilful default. The RBI defines a wilful defaulter as someone who has the ability to repay but deliberately refuses. This is a formal category with a defined process. Genuine financial hardship job loss, medical emergency, business failure does not make someone a wilful defaulter. The RBI's own definition requires that the borrower have the funds available and still refuse to pay.

Ramesh, who lost his job and has no income, is not a wilful defaulter. He is a borrower in genuine distress. These are not the same thing.

When a recovery agent threatens arrest, such conduct may violate applicable laws and RBI guidelines. Under BNS Section 351, threatening someone to cause alarm is criminal intimidation; the agent, not you, is committing an offence.

FREED Expert Tip

If a recovery agent threatens arrest, ask for their full name, agency name, and the bank's authorisation letter number in writing.

Read more:What Rights Do You Have During the Loan Recovery Process?

These are your rights under the RBI Fair Practices Code and related circulars. They are enforceable rules. The bank is responsible for every one of them.

1. Right to prior written notice. No recovery action may begin without formal written communication from the bank. Recovery agents cannot appear unannounced at your home without a prior written notice being served first.

2. Right to limited contact hours. Calls and visits are only permitted between 8 AM and 7 PM. Any contact before 8 AM or after 7 PM is a direct RBI violation. Document it when it happens.

3. Right to privacy. Your loan details cannot be shared with your family members, neighbours, colleagues, or employer. This disclosure is expressly prohibited under the FPC (Fair Practices Code, the RBI's conduct standard for banks).

4. Right to see ID. Any recovery agent visiting you must produce both a valid ID card and a written authorisation letter from the bank on the spot. You are within your rights to refuse to engage without both documents.

5. Right to dignity. Every interaction must be conducted with basic respect. Abusive language, threats, intimidation, shouting, and public humiliation are prohibited. All of them. There is no situation where an agent is permitted to shame you in front of others.

6. Right to complain. Every bank must publish a Grievance Redressal Officer contact. If the bank doesn't respond to your written complaint within 30 days, you can escalate free of charge to the RBI Integrated Ombudsman at cms.rbi.org.in. The Ombudsman can award compensation of up to ₹20 lakh. [(https://www.rightsofemployees.com/rbi-integrated-ombudsman-scheme-rb-ios-2026-new-rules-compensation/)]

7. Right to restructuring consideration. Under the FPC, banks are required to consider requests for EMI restructuring or a temporary payment pause (moratorium) when you document genuine financial hardship. They are not required to approve it, but they are required to consider it. Make your request in writing. [(RBI Fair Practices Code: https://www.rbi.org.in/scripts/NotificationUser.aspx?Id=12378&Mode=0)]

These are not suggestions. The bank is accountable for enforcing every one of them.

What Are Your Options When the Recovery Process Has Already Started?

Settlement is not something a borrower chooses out of preference. Banks and financial companies only consider it when you are in genuine financial difficulty and are truly unable to repay the full amount. It is a last resort, not a shortcut.

With that said, here are the options, in order:

1. Respond in writing to the bank. Write to the bank's Grievance Redressal Officer (not just customer care). State the reason for missed payments clearly: job loss, medical emergency, business failure. Formally request a revised payment schedule or a moratorium (temporary pause on payments). Doing this in writing before the bank escalates shows good faith and creates a paper trail.

2. Request EMI reduction or tenure extension. Banks can reduce your monthly payment by extending the repayment time. This doesn't reduce what you owe; it makes each monthly payment smaller. This works best in the 30–90 day window before NPA classification.

3. Convert to a debt management programme. A structured monthly payment that consolidates multiple EMIs (merging all loans into one lower monthly amount). This is a formal arrangement, not another loan.

4. One-time settlement (OTS). OTS paying it once so the matter ends, is for borrowers who are genuinely unable to repay at all. Typically, this means 90+ days past due, NPA-classified, recovery agents calling, no foreseeable ability to pay. FREED helps enrolled customers with unsecured loans negotiate settlements with banks: handling the documentation, managing the back-and-forth, and helping ensure settlement documentation is completed correctly. FREED charges fees only on successful settlement. The "Settled" mark on your CIBIL report stays for up to 7 years. The settlement waiver can be up to 50%* of the outstanding amount.

If your total EMIs already eat up more than 50% of your take-home salary, that's a signal worth paying attention to.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

What Should You Do If a Recovery Agent Crosses the Line?

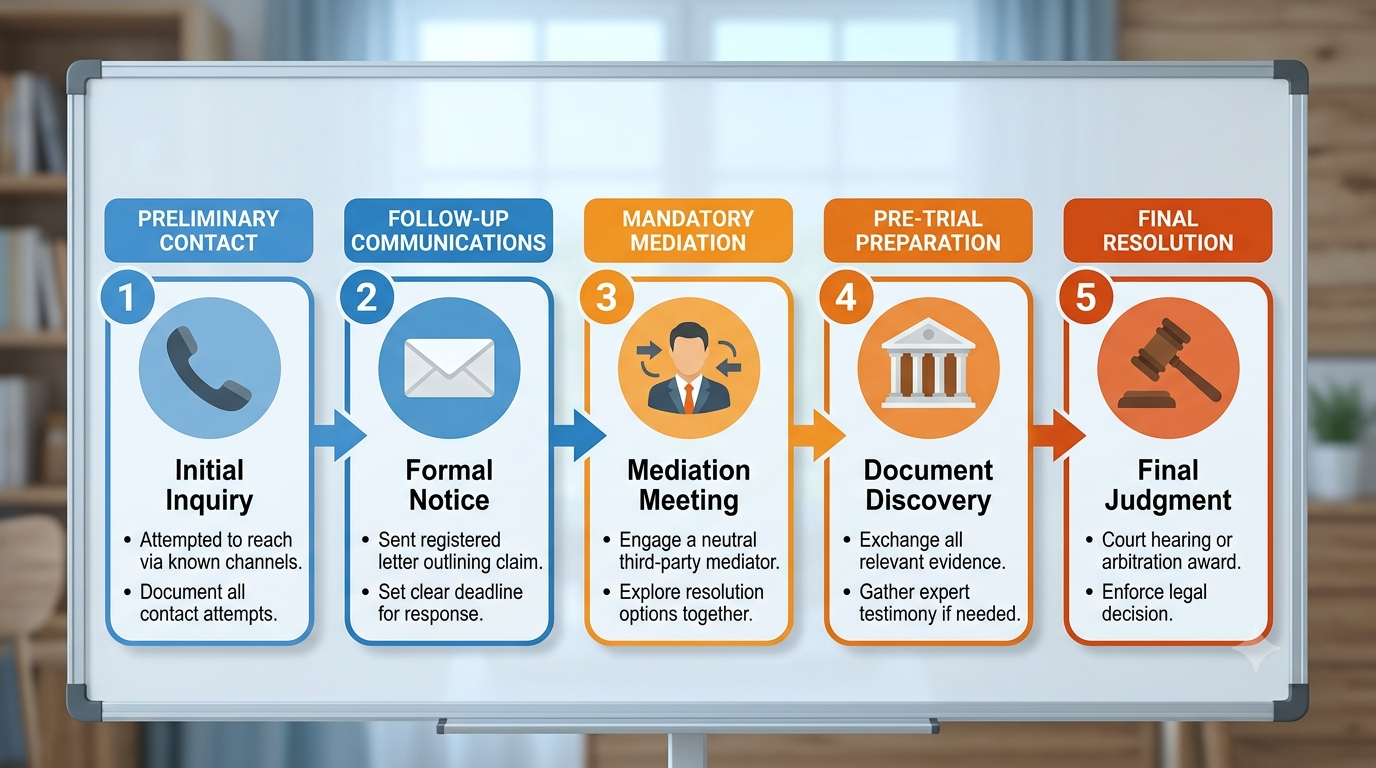

Filing a complaint creates a formal record and escalation path. The underlying debt remains. But illegal behaviour has to stop, and here's how to make that happen.

Step 1: Document first. Screenshot call logs. Record interactions under Indian law, one-party consent makes this legally permissible (you are one of the parties). Note the date, time, exact language used, and the agent's name and agency if you have them. Documentation is what makes a complaint credible. (Section 65B, Indian Evidence Act). [(Reference: https://recordinglaw.com/india-recording-laws/)]

Step 2: Write to the bank's Grievance Redressal Officer. Not the customer care helpline. Every bank is required to publish its Grievance Redressal Officer's name and contact details on its website. Send a written complaint to that specific person. The 30-day resolution clock starts from the date of that written complaint.

Step 3: Escalate to the RBI Ombudsman. If the bank doesn't respond within 30 days or if their response is unsatisfactory, file a complaint at cms.rbi.org.in. This is free. The Ombudsman can award compensation of up to ₹20 lakh. You do not need a lawyer to do this. [(https://www.rightsofemployees.com/rbi-integrated-ombudsman-scheme-rb-ios-2026-new-rules-compensation/)]

Step 4: File an FIR for explicit threats. If an agent explicitly threatens arrest, physical harm, or impersonates a law enforcement official, file an FIR under BNS Section 351 (criminal intimidation). Call recordings and screenshots are admissible under Indian Telegraph Rules with one-party consent. [(https://vakilsearch.com/bns/sections/351)]

FREED can help you understand what the rules say and help you put together the right complaint letter if that's what you need. For step-by-step format, see: freed.care/resources/complaint-letter-recovery-agents

What Banks and Recovery Agents Can and Cannot Do: Full Reference

Area | Permitted | Prohibited |

Contact timing | Calls and visits between 8 AM and 7 PM | Any contact before 8 AM or after 7 PM |

Identification | Must carry ID card + bank authorisation letter | Cannot operate without both; cannot refuse to show them |

Language and conduct | Polite, professional communication only | Abusive language, threats, shouting, intimidation, humiliation |

Third-party contact | Contact the borrower or co-applicant/guarantor only | Contact family, neighbours, colleagues, or employer; disclose loan details to any third party |

Workplace visits | Visit only with explicit written consent from borrower | Unannounced visit to workplace; creating a scene in front of colleagues |

Legal threats | Inform borrower of bank's right to initiate civil or legal proceedings if applicable | Threaten criminal arrest, impersonate police or court officials, issue fake warrants |

Cash collection | Accept payments against proper written receipts | Collect cash without issuing a written receipt |

Digital conduct (loan apps) | Communicate only through official channels | Access phone contacts, share borrower data, use social pressure via messaging |

Banks are fully responsible for every action in this table. The responsibility cannot be delegated to the recovery agency.

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions