Personal Loan Options With a Bad Credit Score

Many lenders generally consider applicants with lower credit scores to be higher risk, although eligibility varies by lender. Approval gets harder and interest rates run higher, but NBFCs, secured loans, and co-applicant routes can still get you funded if you compare terms carefully first.

Mohit Juneja

Reviewed by FREED India, Debt Resolution Specialists

KEY TAKEAWAYS

A personal loan with a bad credit score is possible through NBFCs, secured loans, or a co-applicant, not just banks.

A score under 650 usually means higher interest and stricter terms, not automatic rejection.

Every formal loan application creates a hard enquiry that lenders may consider when assessing future credit applications.

India's household debt-to-GDP ratio crossed 40% by the end of 2024, and multiple-loan borrowing is common.

If old unpaid debt is what's causing the bad score, taking on more debt first can make the underlying problem worse.

What Counts as a Bad Credit Score for a Personal Loan?

CIBIL scores in India run from 300 to 900. Many lenders generally view scores of 750 and above as favorable, often leading to better rates and faster approvals, though this varies by lender and loan type. Scores below 650 are often seen as higher-risk by lenders, and this is generally what people mean when they refer to a "bad" credit score.

It's worth being clear that this is a risk classification, not a judgment on you as a person. Lenders read a low score as a signal that repaying on time might be harder, based purely on patterns in your history. It says nothing about why the score dropped, and the real reasons are usually far from careless. Job loss, a medical emergency, a business slowdown, or simply too many EMIs piling up at once, all of these show up on paper the same way: as missed payments.

Understanding that this is a risk-based number, not a character assessment, helps set the right frame before you start looking at your actual loan options. A bad score doesn't close every door. It just changes which doors are realistically open to you and on what terms.

Why Does a Bad Credit Score Make Loans Harder to Get?

A personal loan is unsecured, meaning there's no asset backing it up for the lender to fall back on if repayment stops. Because of that, the lender's entire risk assessment rests on your history and your current financial profile. A low score signals more uncertainty about repayment, and lenders respond to uncertainty by pricing it in, either through a higher interest rate, a lower approved amount, stricter documentation, or some combination of the three.

This isn't arbitrary. It's simply how risk-based lending works for any product without collateral. A bank or NBFC lending to a lower-score applicant is taking on more potential downside, and the terms offered reflect that trade-off rather than a blanket refusal to lend at all.

Signs You Should Pause Before Taking Another Loan

A few situations are worth pausing over before you apply for anything new, regardless of how urgent the need feels.

You've already missed EMIs on existing loans and haven't caught up yet. You're considering this loan specifically to pay off another one, a pattern known as debt cycling. You're not entirely sure of the total amount you'd end up repaying once interest and fees are added in. You're thinking about applying to four or five lenders at once, hoping one of them says yes.

Any one of these is a reasonable moment to slow down and look at the fuller picture before moving forward with a new application.

How to Approach Applying for a Loan With Bad Credit

Start by checking your credit report before you apply anywhere. This tells you exactly where you stand and whether there's anything factually wrong on it worth correcting first, since a genuine error dragging your score down unnecessarily is worth fixing before you go further.

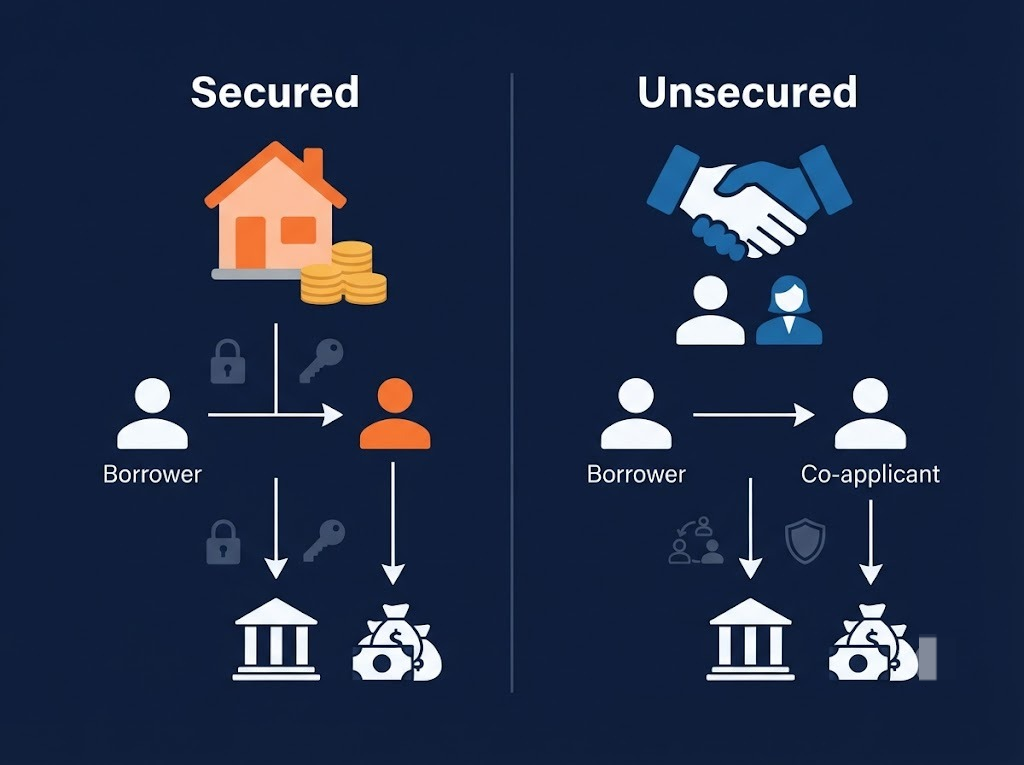

Next, decide between secured and unsecured routes based on what you actually have available. If you hold a fixed deposit or gold you're comfortable pledging, approval remains subject to the lender's assessment. and usually comes at a better rate, since the lender's risk is lower with collateral in place. If you don't have an asset to offer, an unsecured NBFC loan or a co-applicant route becomes the more realistic path.

Compare lenders rather than applying to several at once hoping for the best outcome. Shortlist two or three options based on your research, compare the full terms, and apply selectively. Each application creates a fresh hard enquiry, and stacking several in a short window works against the very score you're trying to borrow against.

Finally, keep the loan amount realistic. Asking for less than the maximum you think you might qualify for improves your approval odds and makes repayment genuinely manageable once the loan comes through.

What the Law Says

RBI's Fair Practices Code requires every lender to disclose the Annual Percentage Rate (APR), the true annual cost of the loan including interest and all fees, through a Key Fact Statement before you sign a loan agreement.

Check your options.The Real Cost of a Bad-Credit Loan

Here's what a higher interest rate actually does to your repayment over time, in plain numbers. Say you borrow Rs. 2 lakh over 3 years. At a bank rate of 13% per annum, available to a borrower with a healthy score, your total repayment comes to roughly Rs. 2.44 lakh, meaning around Rs. 44,000 in interest. At a bad-credit NBFC rate of 28% per annum for the same amount and tenure, your total repayment climbs to roughly Rs. 2.98 lakh, close to Rs. 98,000 in interest.

That's a difference of over Rs. 50,000 on the exact same loan amount, purely from the interest rate gap tied to credit score. This isn't meant to discourage borrowing when you genuinely need it, but it's the real math worth seeing clearly before signing anything, since the headline EMI figure alone often hides just how much more the total repayment actually costs at a bad-credit rate.

FREED Expert Tip

Compare APR (Annual Percentage Rate), not just the headline interest rate. Processing fees change the real cost.

Check your Credit InsightsWhat Are Your Options With a Bad Credit Score?

A few genuine paths exist beyond a straightforward bank rejection, each with its own trade-off worth understanding.

A secured personal loan, backed by a fixed deposit, gold, or property, is usually the easiest to get approved with a bad score, and it typically comes at a meaningfully lower rate than an unsecured option, since the lender's risk is covered by the collateral. The trade-off is straightforward: if repayment fails, the asset you pledged is at risk.

An NBFC unsecured loan doesn't require collateral and works off your income and bank statement instead. It's more flexible on score than a bank, but comes at a higher rate to compensate for that flexibility. A co-applicant or guarantor loan brings someone with a stronger score into the application, which can meaningfully improve approval odds and sometimes the rate too, though it means that person shares full repayment liability if things go wrong. Responsible repayment on a loan reported to a credit bureau can help establish a stronger repayment history over time.

None of these is inherently the "best" choice. Which one fits depends on what you have available, how urgently you need funds, and how much risk you're comfortable spreading to a co-applicant or an asset.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

Should You Fix Your Credit Score Before Applying?

Many readers land at a bad score not through bad luck alone, but because of existing unpaid debt that's already built up. If that's your situation, it's worth pausing to understand exactly what's dragging your score down before taking on a new loan on top of it, since a new loan doesn't resolve the underlying issue that caused the low score in the first place.

The most useful first step here is simply seeing the full picture clearly. Knowing whether your score is low because of a fixable report error, a few missed EMIs that are now behind you, or ongoing debt stress that's still active changes what the right next move actually is. Getting that clarity before applying for anything new usually saves more money and stress than rushing into another loan application.

Know what's really hurting your score

Get your Experian-based credit report and a step-by-step fix plan.

Check Your ScoreHow FREED Helps

FREED's Credit Insights is the natural starting point here. For Rs. 249 for a 3-month subscription, available to everyone whether or not you're enrolled in any other FREED program, it pulls your Experian-based credit report and shows you exactly what's impacting your score, along with clear, step-by-step recommendations on what to focus on next.

If it turns out you're still managing your payments but juggling multiple EMIs across different lenders, FREED's Loan Consolidation Plan (Reduce My EMI) assesses your financial profile and matches you to a lending partner who combines those existing loans into one new loan with a single, lower EMI. Loan consolidation may help simplify repayments for eligible borrowers, depending on repayment behaviour and lender reporting.

If the situation is different, and you've already defaulted and are genuinely unable to repay in full, that calls for a separate conversation entirely. Settlement is not something a borrower chooses out of preference. It's the option available specifically when repayment has become genuinely impossible. In that case, FREED helps borrowers settle their unpaid/overdue loans at up to 50% less* of what you owe.

Waiver percentage shown is indicative and depends on your bank's final decision. FREED is not a Loan Provider. No specific outcome is guaranteed.

What Helps Before You Apply

A few things genuinely improve your position before you submit any application, and they're worth framing as helpful steps rather than mistakes to avoid.

Check your credit report for errors first. A genuine mistake unfairly dragging your score down is worth correcting before a lender ever sees it. Apply selectively rather than widely. Two or three well-matched applications serve you far better than five scattered ones, since each one leaves a mark on your report. Keep the loan amount modest and tied to your actual need rather than the maximum figure a lender might approve. And read the APR carefully, not just the advertised interest rate, since processing fees and other charges can meaningfully change what the loan actually costs you over its full term.

FREED Expert Tip

Compare APR, not just the headline interest rate. Processing fees change the real cost, and that's exactly what an Experian-based check flags before you sign anything.

See Your Full Cost Before You BorrowHow to Approach a Bad Credit Personal Loan Application

Check your credit report first

Pull your Experian or CIBIL report before applying anywhere. Look for errors dragging the score down unfairly, since correcting reporting errors helps ensure lenders assess accurate credit information.

Decide secured or unsecured

A secured loan against FD or gold is easier to get approved than an unsecured one, and usually comes at a better rate too, since collateral lowers the lender's risk.

Compare, don't mass-apply

Shortlist 2 to 3 lenders and compare APR carefully. Every extra application beyond that is a fresh hard enquiry working against your score.

Keep the amount realistic

Requesting a loan amount that aligns with your repayment capacity may improve your application, subject to the lender's assessment.

Consider a co-applicant carefully

A strong-score co-applicant meaningfully helps approval odds, but it's worth being clear with them upfront that they share full repayment liability, not just moral support, if things don't go as planned.

Bad Credit Personal Loan Options: Quick Reference

Option | Collateral Needed | Typical Approval Speed | Who It Suits |

Secured Personal Loan | FD / gold / property | Faster | Borrowers with an asset to pledge |

NBFC Unsecured Loan | None | Moderate | Borrowers with stable income, no asset |

Co-Applicant Loan | None (shared liability) | Moderate | Borrowers who can add a strong-score co-applicant |

Small Credit-Builder Loan | None | Fast | Borrowers rebuilding score with a small, repayable amount |

Terms vary by lender and change over time. Verify current terms directly with the lender before applying. FREED does not recommend or endorse any specific bank or NBFC.

Sources

Claim in Blog | Source |

India's household debt-to-GDP ratio crossed 40% by the end of 2024 | RBI, Financial Stability Report series: https://rbi.org.in/Scripts/FsReports.aspx |

Lenders must disclose the annualised rate of interest (APR) to borrowers under the Fair Practices Code | RBI, Master Circular on Fair Practices Code for NBFCs: https://www.rbi.org.in/commonman/english/scripts/Notification.aspx?Id=867 |

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions