How to write a loan settlement letter to a bank

The letter is the starting point of every settlement negotiation. Getting it right, tone, content, documentation, determines whether the bank takes the proposal seriously. Here is exactly what to write and how.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

A loan settlement letter is a formal written request to the bank asking it to accept a negotiated lump sum, less than the full outstanding, as complete and final payment.

It must be factual, specific, and supported by documentation. Emotional language is less effective than documented evidence of genuine hardship.

The letter initiates negotiation, not settlement. Expect the bank to counter. The opening offer should be lower than the maximum you can pay.

Never pay any amount before receiving a written settlement letter from the bank on official letterhead confirming the agreed amount closes the account in full.

FREED writes hardship letters, gathers documentation, and negotiates settlements with all major Indian banks on behalf of enrolled clients. First consultation is free.

What a Loan Settlement Letter Is and What It Does

A loan settlement letter is a formal written request from a borrower to a bank or lender, proposing that the lender accept a reduced lump sum as complete and final payment of an outstanding loan or credit card balance.

It is not a complaint. It is not a request for more time. It is a structured, businesslike proposal that says: this is my situation, this is what I can pay, and I am requesting that you accept it as full and final settlement.

Banks receive many such requests. What separates the ones that produce results from those that do not is the quality of the documentation, the specificity of the proposal, and the professionalism of the tone. A well-written letter with strong supporting documentation opens a genuine negotiation. A vague, emotional letter without documentation is typically treated as a standard collection account.

The letter does not settle the debt. It starts the conversation that leads to settlement.

When to Send One

A loan settlement letter is appropriate when the following conditions exist together.

The account is in default, ideally for 90 days or more. Banks are most open to settlement after the account has been classified as an NPA internally. Before this point, the bank still expects full recovery and is unlikely to offer meaningful reductions.

The hardship is genuine and documented. The bank will assess the letter against the evidence. Without documentation, the claim of hardship is just a claim.

A lump sum is available. Banks strongly prefer lump sum settlements over structured payment plans for NPA accounts. A one-time payment closes the case immediately. If a lump sum is not yet available but is being built through savings, FREED's Debt Resolution Programme builds the fund through monthly contributions before approaching the bank.

The borrower is ready to negotiate, meaning the opening offer in the letter is below the maximum that can be paid.

FREED Expert Tip

Do not send the letter on the day you decide to settle. Gather documentation first. A letter sent with comprehensive supporting documents is treated as a serious proposal. A letter without documentation is treated as a standard default account. The documentation is the substance. The letter is the vehicle.

Talk to FREEDWhat to Include: Section by Section

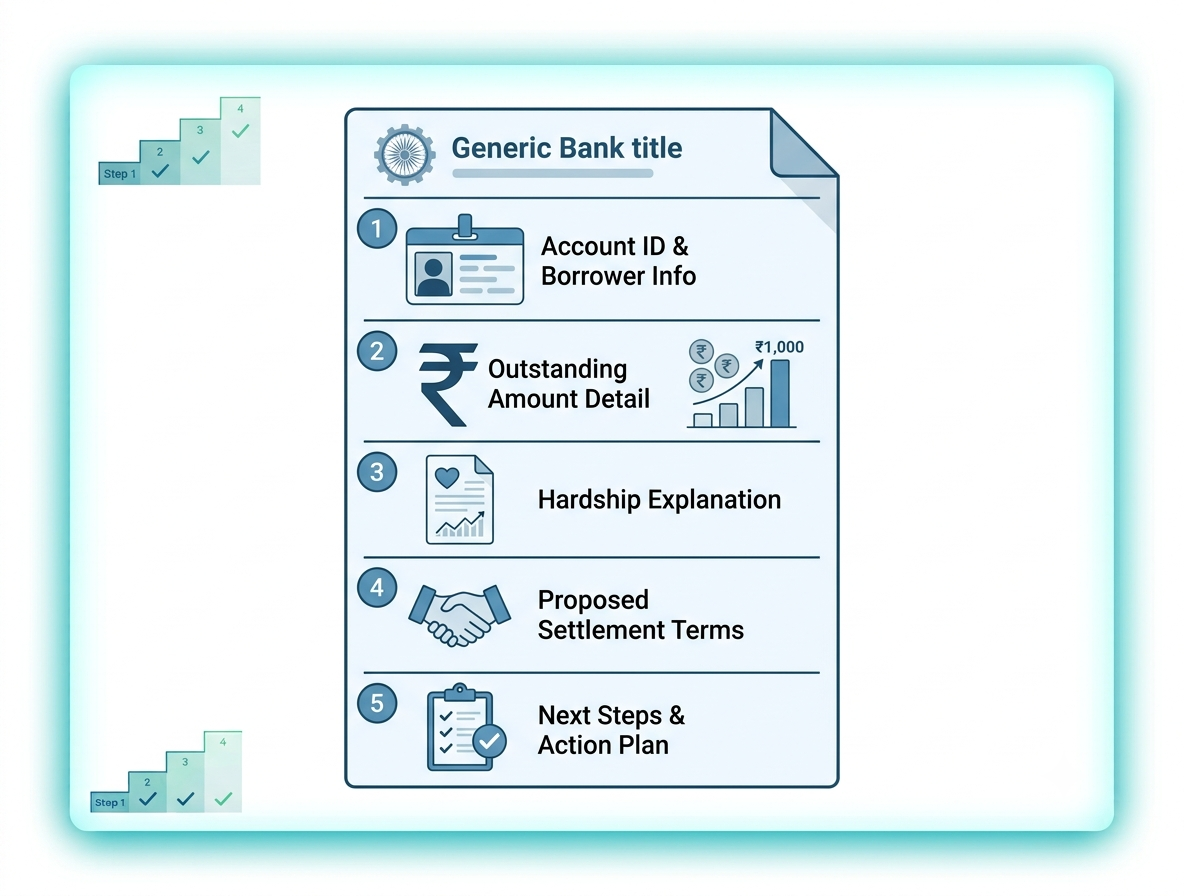

A well-structured settlement letter has five components.

1. Account identification. State the loan account number or credit card account number clearly. Include the bank name, branch, and the account holder's name exactly as it appears on bank records. Include the date of the letter.

2. Current outstanding amount. State the total outstanding as of a recent date, including principal, interest, and accumulated charges. Acknowledge this number clearly. It shows the bank you have reviewed your account and are engaging in good faith.

3. Hardship explanation. Explain clearly and factually what changed, and when. A job loss in a specific month. A medical diagnosis and the associated costs. A business failure with documented revenue collapse. Keep this factual and specific. Banks assess hundreds of hardship cases. Vague language carries far less weight than specific, dated language with supporting documentation.

4. Settlement proposal. State the specific amount being proposed as a one-time lump sum settlement. Explain briefly how this amount has been arranged. Make the offer realistic and lower than the maximum that can be paid, to create negotiating room.

5. Requests and next steps. State clearly that any payment will be made only upon receipt of a written settlement letter from the bank on official letterhead, confirming the agreed amount and that it constitutes full and final settlement with no further dues. Request a No Dues Certificate upon payment.

Documents to Attach

The letter alone is insufficient. Attach everything that supports the hardship claim.

For job loss: the termination or retrenchment letter, the last three months of salary slips before the job loss, the last three months of bank statements showing the income reduction.

For medical hardship: hospital admission and discharge summary, medical bills, doctor's certificates where relevant, bank statements showing the expenditure.

For business failure: GST returns or ITR showing revenue decline, bank statements of the business account, any formal closure documentation.

For all situations: the last three to six months of personal bank statements, a copy of PAN card, and a copy of the loan or credit card account statement showing the current outstanding.

The documentation is the substance of the settlement case. Without it, the letter has no weight.

Sample Loan Settlement Letter Template

[Your Full Name] [Your Address] [City, State, PIN Code] [Your Phone Number] [Your Email Address] [Date]

To, The Recovery / Settlements Department [Bank Name] [Branch Address]

Subject: Request for One-Time Settlement, Loan / Credit Card Account Number [XXXXXXXXXX]

Dear Sir / Madam,

I am writing with reference to my [personal loan / credit card] account number [XXXXXXXXXX] held with your bank. The current total outstanding on this account, including principal, interest, and accumulated charges, stands at approximately Rs. [XX,XX,XXX] as of [Date].

I wish to bring to your attention the genuine financial hardship I have been experiencing since [Month and Year], which has made it impossible for me to continue servicing this obligation under the original terms.

[State the hardship specifically. Example: "I was retrenched from my position as [Designation] at [Company Name] on [Date], as evidenced by the enclosed termination letter. Despite active efforts, I have not been able to secure comparable employment. My monthly income has reduced from Rs. [Amount] to Rs. [Current Income / Nil], and I am currently supporting [family members] on this income."]

[Alternatively: "In [Month/Year], I was diagnosed with [medical condition] and underwent treatment at [Hospital Name]. The medical expenses amounted to Rs. [Amount], as evidenced by the enclosed hospital bills and discharge summary. This has severely depleted my savings and reduced my capacity to service existing obligations."]

Given these circumstances, I am unable to repay the full outstanding amount. However, I am genuinely committed to resolving this account and am in a position to offer a one-time lump sum settlement of Rs. [Proposed Amount], which represents [XX]% of the total outstanding.

This amount has been arranged through [personal savings / support from family / structured savings programme] and can be paid within [Number] days of receiving a written settlement confirmation from your bank.

I respectfully request that your bank consider this proposal and revert with a written settlement offer on official letterhead, clearly stating the agreed settlement amount, the payment deadline, and confirmation that this amount constitutes full and final settlement of the account with no further dues pending.

I wish to clarify that any payment will be made only upon receipt of the above written confirmation. I also request that a No Dues Certificate be issued upon completion of the payment.

I have enclosed the following documents in support of this request: [List documents attached]

I sincerely hope for a positive response and remain available for any further discussion at your convenience.

Yours faithfully,

[Your Signature] [Your Full Name] [Date]

Enclosures: [List all attached documents]

Legal Note

Under RBI Fair Practices Code, a bank must consider a genuine hardship settlement request and respond within a reasonable timeframe. Once a settlement is agreed and payment is made, the bank is required to update the credit bureau to reflect "Settled" status within 30 days. If the account continues to show as "Outstanding" after settlement, raise a formal dispute with CIBIL under the Credit Information Companies (Regulation) Act. FREED assists clients with this process as part of the programme.

Know your rights as a borrowerWhat Happens After You Send It

After the letter is received, the bank's collections or NPA resolution team reviews the account. They assess the outstanding amount, the default history, the hardship documentation, and the proposed settlement percentage against their internal recovery benchmarks.

Most banks respond within two to four weeks. The response is typically a counter-offer, a higher percentage than what was proposed. This is expected. Counter-offer back with a number between the opening offer and the bank's counter. Expect two to three rounds before an amount is agreed.

Once a number is agreed verbally or informally, do not pay anything. Request the formal written settlement letter first. This is the critical document that protects the borrower's position. Without it, there is no legal confirmation that the amount closes the account.

After payment, follow up immediately for the No Dues Certificate. Then monitor the CIBIL report to confirm the account is updated to "Settled" within 30 days.

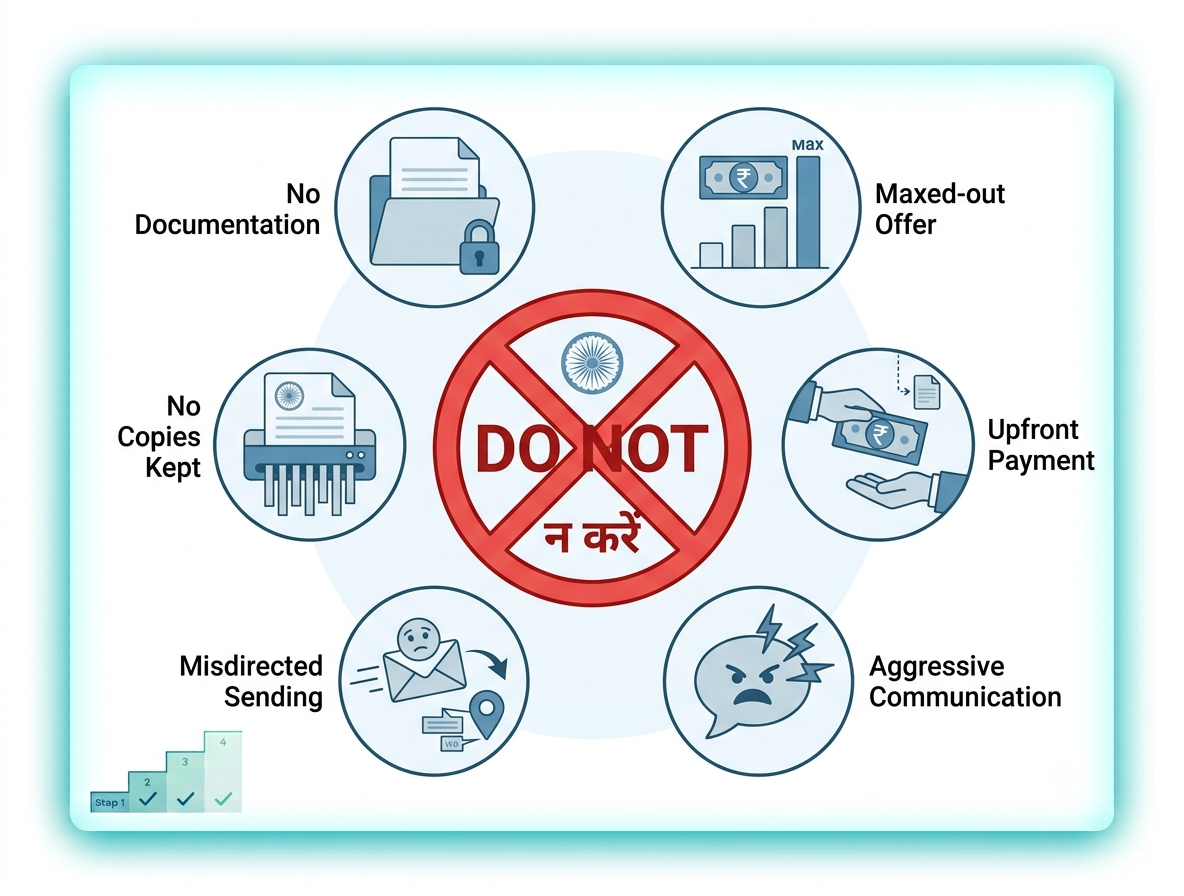

Common Mistakes That Kill Settlements

Sending without documentation. An undocumented hardship claim is treated as unsubstantiated. The documentation is not supplementary. It is essential.

Opening at the maximum. If the most that can be paid is stated in the opening letter, there is no room to negotiate when the bank counters higher. Always open below the actual ceiling.

Paying before receiving the written settlement letter. Once money is transferred, all leverage is gone. The bank must provide written confirmation before any payment is made.

Using emotional or aggressive language. The letter should be factual and professional. Emotional appeals are less effective than documented evidence. Aggressive language damages the relationship needed for the negotiation.

Sending to the wrong department. Address it specifically to the Settlements or Recovery department, or to the Nodal Officer. General customer service does not handle settlement decisions.

Not keeping copies of everything. Keep a copy of the letter, every document attached, every response received, every payment made. These records protect the borrower if any dispute arises.

When to Use a Professional Negotiator

Writing and sending the letter yourself is possible. The risks are: not knowing what settlement percentage the bank is realistically willing to accept, making process errors that lose legal protection, and accepting a worse outcome than what was available.

FREED's debt experts write the hardship letter, compile the supporting documentation, and submit the settlement proposal to the bank on the enrolled client's behalf. They then negotiate the settlement through all rounds using knowledge of what each major Indian bank is willing to accept at each stage of the default timeline.

FREED only charges a fee on successful settlement. The first consultation is always free. For most clients, the improvement in settlement percentage achieved through professional negotiation, combined with correct documentation throughout, more than offsets the service fee.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions