How to get 750 credit score in India

750 is the threshold where most Indian banks offer their best rates and fastest approvals. Here is the specific, prioritised plan to get there from wherever you are starting.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

A 750 CIBIL score is the threshold at which most Indian banks offer their best loan rates, fastest approvals, and highest credit limits. Getting there is a specific, achievable goal with a clear plan.

The single most powerful action is paying every EMI and credit card bill on time, every month, without exception. This one habit, sustained consistently, produces more score improvement than any other change.

Credit utilisation, how much of your available credit limit you are using, is the second most impactful factor and the one that can improve most quickly.

The realistic timeline to 750 depends on the starting score: 2 to 3 months from 720, 6 to 12 months from 650, and 18 to 36 months from below 600 with consistent positive behaviour throughout.

If existing debt is causing missed payments and high utilisation, the score cannot reach 750 until the debt is addressed. FREED can help reduce that burden so the recovery becomes possible.

Why 750 Is the Target Score in India

The credit score scale in India runs from 300 to 900. Most Indian banks and NBFCs use 750 as the threshold that separates good from excellent creditworthiness.

Above 750: access to the lowest available interest rates on personal loans, home loans, and vehicle loans. Fastest approvals. Highest credit card limits. Banks compete for your application rather than evaluating it cautiously.

700 to 749: most products are accessible, but sometimes at rates 1% to 2% higher than the best tier. Some banks impose additional conditions on approval.

Below 700: options narrow. Below 650, most mainstream applications are declined. Below 600, most lenders decline outright.

The difference in interest rate between a score of 780 and a score of 650 on a Rs. 10 lakh personal loan over 5 years is typically 4% to 6% annually. That difference amounts to Rs. 1.2 lakh to Rs. 1.8 lakh in total interest on the same loan amount. Getting to 750 is not just a financial hygiene exercise. It is a direct rupee-saving goal.

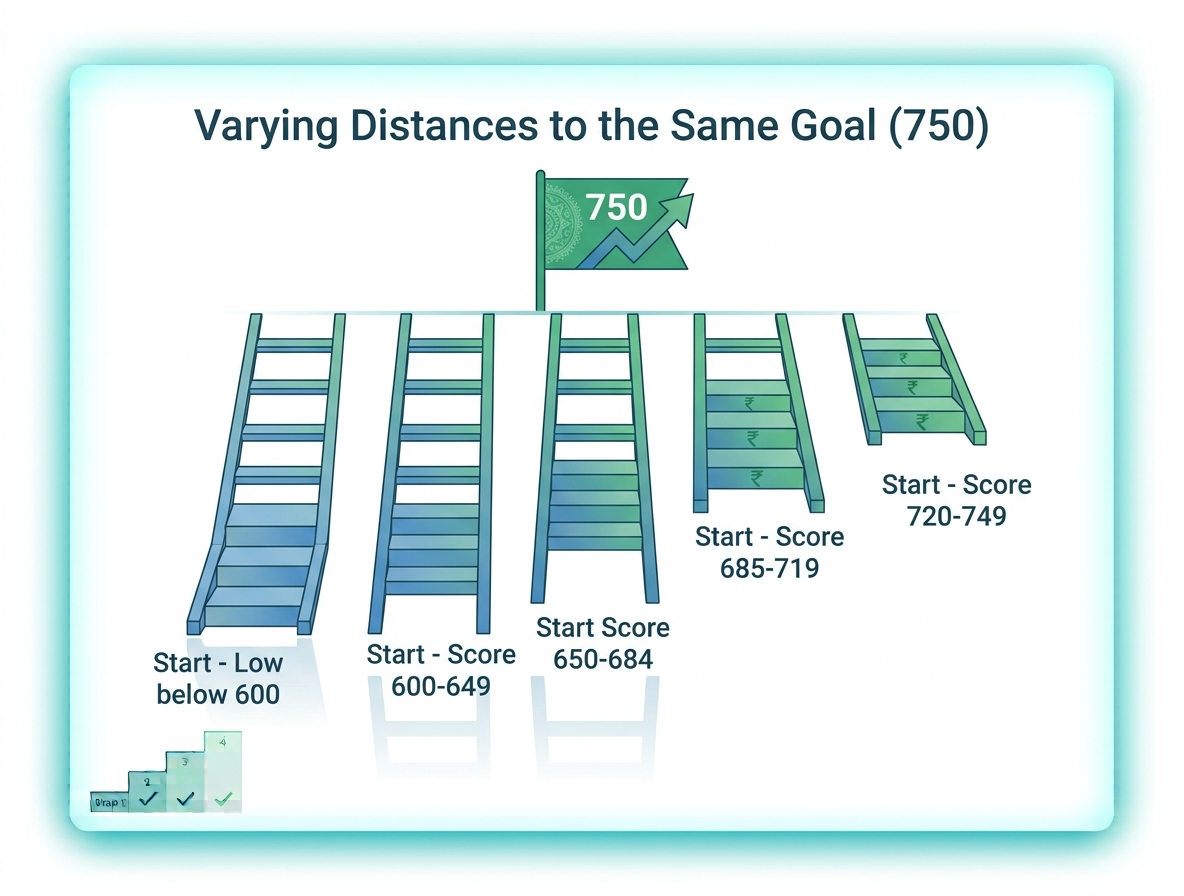

How Long It Takes from Different Starting Points

The timeline to 750 depends entirely on the current score and what is causing it to be below 750.

Starting from 720 to 749: You are close. Two to three months of consistent positive behaviour, particularly on-time payments and reducing utilisation, can push you over the threshold. This range needs maintenance, not repair.

Starting from 650 to 719: Six to twelve months of consistent on-time payments, reduced credit card utilisation, and no new negative marks (missed payments, hard enquiries). Progress will be visible within three to four months and meaningful within six.

Starting from 600 to 649: Twelve to eighteen months of consistent positive behaviour. Negative marks from past missed payments are still relatively recent and carry significant weight. Each month of positive behaviour adds to the recovery trajectory.

Starting from below 600: Eighteen to thirty-six months. This range typically indicates a pattern of missed payments or a default. Recovery is possible and reliable, but it requires patience and consistency throughout. Shortcuts do not exist.

Starting from NH or NA (no history): Six to twelve months to build a meaningful positive credit profile from zero, using the right starting products.

FREED Expert Tip

The fastest way to find out exactly what is keeping your score below 750 is to pull your credit report and read it account by account. In most cases, one or two specific factors, a single account with a string of missed payments, or a credit card consistently at 70% utilisation, are responsible for most of the gap. Fixing the biggest specific problem first produces the fastest score improvement.

Talk to a FREED Counsellor

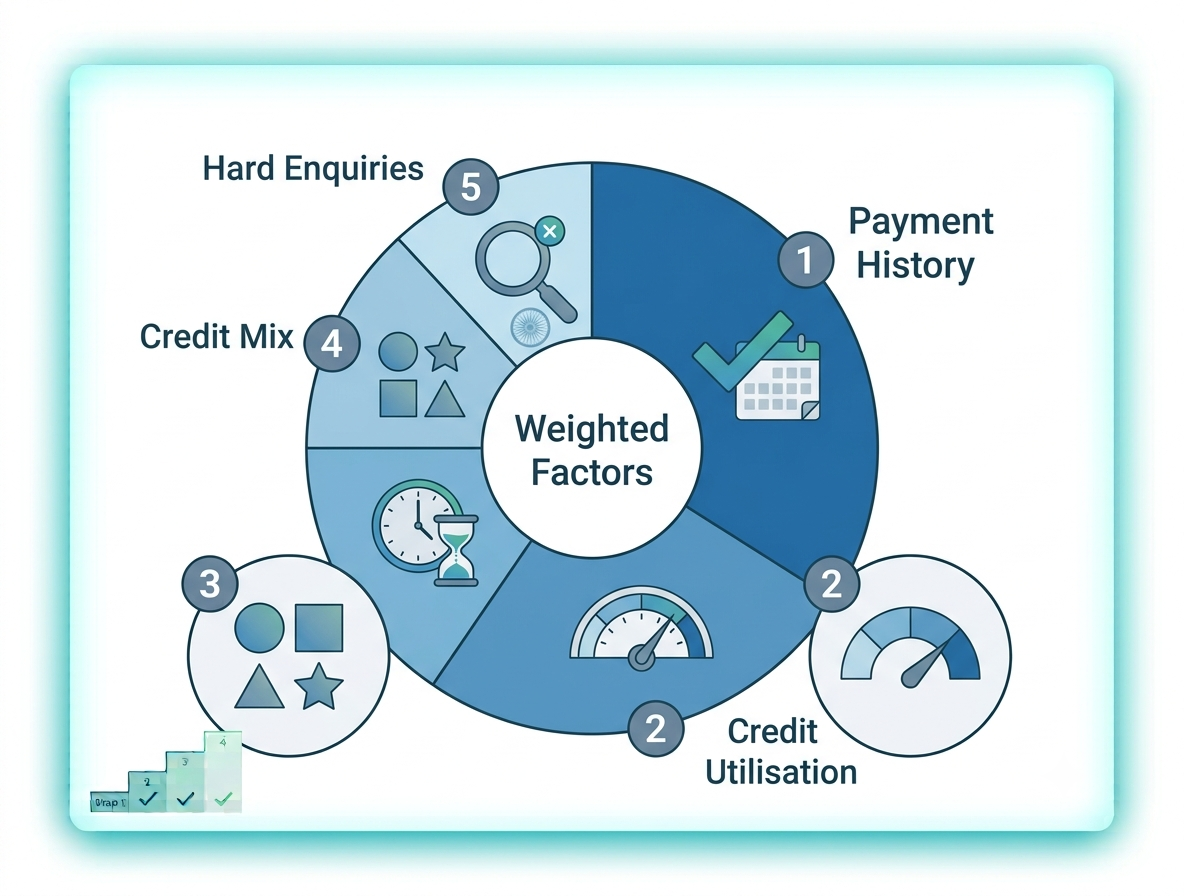

The Five Factors That Determine Your Score

Understanding the five factors and their relative weight is the foundation of any effective improvement plan.

Payment history (35% to 40% weight): Whether you pay every EMI and credit card bill on time, every month. This is the highest-weighted factor. One missed payment can reduce the score by 50 to 100 points. Twelve consecutive on-time payments produce meaningful recovery.

Credit utilisation (25% to 30% weight): What percentage of total available credit limit you are currently using. Below 30% is healthy. Above 50% is a significant score suppressant. Above 70% signals financial stress to lenders and reduces the score substantially.

Credit age (15% weight): How long your credit accounts have been open. Older accounts with clean histories are valued. Closing old accounts shortens credit age and can reduce the score.

Credit mix (10% weight): Whether you have a healthy variety of credit types, both secured loans (home loan, vehicle loan) and unsecured credit (credit cards, personal loans). A borrower with only credit cards has a narrower profile than one with both.

Hard enquiries (10% weight): How many times lenders have pulled your report as part of credit applications. Each hard enquiry causes a small, temporary score reduction. Multiple enquiries in a short period signal financial stress.

Improvement effort should be directed toward factors in order of weight: payment history first, utilisation second, then the others.

Action 1: Pay Every Due on Time, Without Exception

This is the highest-impact, highest-priority action for reaching 750. Everything else is secondary to this one habit.

Set up auto-pay or standing instructions for every EMI and every credit card account, at minimum for the minimum due amount. Automate this today. Then add a phone calendar reminder seven days before each due date as a verification check.

Pay two to three days before the due date, not on it. Bank processing times mean a payment made on the due date may clear late. The two to three day buffer eliminates this risk.

For credit cards, pay the full outstanding balance, not just the minimum. Paying only the minimum keeps the account from defaulting but keeps utilisation high, which suppresses the score through a different factor.

This single habit, maintained without exception for twelve months, produces more score improvement than any other action.

Action 2: Reduce Credit Utilisation Below 30%

If credit card balances are consistently above 30% of the total available limit, utilisation is suppressing the score independently of payment history. Getting below 30% is the second most impactful action.

Three ways to reduce utilisation:

Pay down the outstanding balance directly. Even reducing from 65% to 40% produces a measurable score improvement within one to two billing cycles.

Pay the credit card balance before the billing statement date. The balance the bureau records is what appears on the statement. A payment made two weeks before the statement date reduces the recorded utilisation for that month.

Request a credit limit increase from the card issuer without increasing spending. If the limit increases from Rs. 1 lakh to Rs. 1.5 lakh and the balance stays at Rs. 25,000, utilisation drops mechanically from 25% to 16%, improving the score without changing the actual debt.

Action 3: Check and Fix Report Errors

This is the only action that can improve the score without changing financial behaviour, because errors suppress the score unfairly.

Get your credit report from the official CIBIL website or FREED Credit Insights. Review every account. Check payment histories for any month marked as late when you paid on time. Check account statuses for any loan or card that was closed but still shows as active. Check personal information for accuracy.

If any entry is incorrect, raise a dispute through the bureau's online portal. Under the Credit Information Companies (Regulation) Act, bureaus must investigate and respond within 30 days. Confirmed errors must be corrected.

Correcting a significant error can produce a meaningful score improvement within 30 to 60 days, faster than any behavioural change can achieve.

Legal Note

Under RBI guidelines and the Credit Information Companies (Regulation) Act, you have the legal right to dispute any inaccurate information on your credit report. If the bureau does not respond within 30 days or fails to correct a confirmed error, you can escalate to the RBI Banking Ombudsman at bankingombudsman.rbi.org.in.

Know your credit rightsAction 4: Do Not Close Old Credit Accounts

A common and counterproductive instinct when trying to clean up a credit profile is to close old cards that are not being used. This almost always hurts the score rather than helping it.

When an old credit card is closed, two things happen. Total available credit limit decreases, which raises utilisation on remaining cards automatically. And credit age shortens, because the closed account's history is no longer contributing to the average age of active accounts.

Unless an old card charges an annual fee that cannot be justified, keep it open. Use it once every two to three months for a small, planned purchase and pay it immediately. This keeps the account active, your credit age intact, and your utilisation ratio healthy.

Action 5: Limit New Credit Applications

Every loan or credit card application triggers a hard enquiry on the CIBIL report. Each enquiry causes a small, temporary score reduction and is visible to any lender who subsequently reviews the report.

Multiple applications in a short period create a pattern that signals financial stress, regardless of whether the applications were approved or declined. This pattern actively works against the goal of reaching 750.

While building toward 750, avoid applying for any new credit product unless genuinely necessary. Space any applications at least three to six months apart. Remember: checking your own score is a soft enquiry and has zero impact on the score.

Action 6: Build a Credit Mix

Lenders look more favourably on borrowers who demonstrate the ability to handle different types of credit responsibly, both secured and unsecured.

A borrower with only credit cards has a narrower profile than one who has managed both a loan and a card responsibly. This difference in credit mix can affect the score at the margin.

You do not need to take on unnecessary debt to improve credit mix. The opportunity to diversify arises when a product is genuinely needed: a two-wheeler loan for commuting, a small consumer durable EMI. When these arise and the FOIR permits, they contribute positively to credit mix alongside their primary purpose.

Action 7: Use a Secured Credit Card If Starting from Scratch

For people with no credit history (score of NH or NA) or a score below 600, a secured credit card is the most accessible and lowest-risk tool for building positive credit history quickly.

A secured credit card is issued against a fixed deposit. The bank holds the deposit as collateral and issues a card with a limit equal to or slightly below the deposit amount. Approval does not depend on CIBIL score because the bank's risk is covered.

Use the secured card for small, regular expenses, a grocery run, a utility bill. Pay the full balance every month. Within six months, a meaningful positive payment history begins building. Within twelve months, the score reflects it clearly.

This is the recommended first step for anyone rebuilding after debt resolution, and the most direct path from NH/NA to a meaningful score.

When Debt Is Preventing You from Reaching 750

There is a specific situation in which the actions above cannot produce meaningful progress toward 750: when existing debt is the cause of both the missed payments and high utilisation suppressing the score.

When EMIs consume 60% or more of monthly income, consistent on-time payment of everything becomes impossible. Something always falls through. When credit card balances are near their limits, utilisation cannot be reduced without first reducing the balance. And when there is no surplus to reduce balances, the utilisation stays high.

In this situation, the score cannot reach 750 through behaviour change alone. The debt load needs to be addressed first.

FREED helps people in exactly this position. Through Debt Consolidation, multiple high-interest obligations are combined into one lower monthly payment, freeing the income margin needed for consistent on-time payments. Through Debt Resolution, outstanding dues are settled for less than the full amount, eliminating those obligations from the budget. Both approaches reduce the financial pressure that is preventing score recovery, creating the conditions where the improvement actions above can actually work.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions