Credit Score Going Down? Here Is How You Can Improve It

A falling credit score is not a life sentence. It is a signal -- one that tells you something specific needs to change. This guide explains exactly what is dragging your score down and the practical steps to bring it back up.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

A CIBIL score falls when one or more of five factors deteriorates, payment history, credit utilisation, credit age, credit mix, or the number of hard enquiries.

The single most effective way to improve a score is to pay every EMI and credit card bill on time, consistently, over several months.

Most people can meaningfully improve their score within 12 to 18 months of sustained good financial behaviour.

If existing debt is the root cause of missed payments and high utilisation, the score cannot recover until the debt is addressed.

FREED helps reduce or resolve that debt so recovery becomes possible.

Why Your Credit Score Might Be Falling

Your CIBIL score does not fall without reason. Every drop has a cause and once you identify the cause, the fix becomes clear.

The most common reasons a score falls in India are missed or delayed EMI payments, a spike in credit card utilisation, multiple loan or credit card applications in a short period, a loan default or settlement, and errors in the credit report that are incorrectly dragging the number down.

In some cases, a score falls because of something a borrower did months ago a late payment, a closed account, a hard enquiry, that is only now showing up in the bureau's updated calculation.

Understanding the five factors that go into the score is the starting point for fixing it.

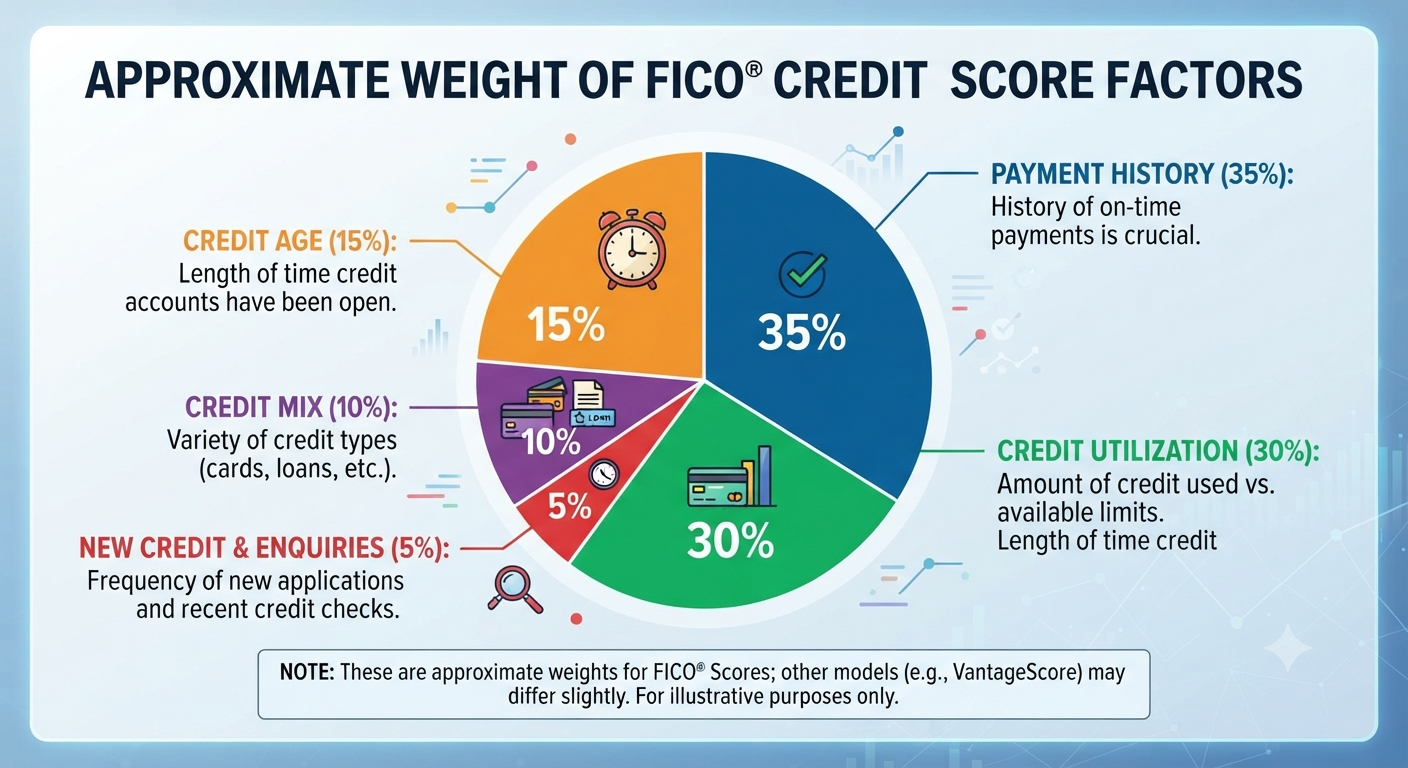

The Five Factors That Make Up Your CIBIL Score

Factor | Impact Level | What It Means |

Payment history | Very High | Whether you pay EMIs and bills on time |

Credit utilisation | High | How much of your credit limit you are using |

Credit age | Medium | How long your credit accounts have been active |

Credit mix | Medium | Whether you have a healthy variety of credit types |

Credit enquiries | Low to Medium | How many times lenders have pulled your report recently |

Each of these can push the score up or down. Most people have one or two dominant problems, identifying yours is the first step.

Step 1: Check Your Credit Report for Errors

Before changing any financial behaviour, check whether your score is being pulled down by something that should not be there.

Credit bureau reports in India contain errors more commonly than most people realise. A loan that was fully repaid still showing as outstanding. An EMI marked as late when it was paid on time. An enquiry from a lender you never actually approached. In some cases, accounts belonging to someone with a similar name appear on the wrong report.

All of these silently reduce your score and none of them reflect your actual financial behaviour.

Get your credit report from CIBIL or any of the other three bureaus (Experian, Equifax, CRIF High Mark). You are entitled to one free report per year from each. Review every entry. If you find anything incorrect, raise a dispute immediately. Bureaus are legally required to investigate and respond within 30 days.

Do this before anything else. A corrected report can sometimes show a meaningful score improvement without any change in financial behaviour.

FREED Expert Tip:

Check your report from at least two different bureaus. Scores and data can vary across CIBIL, Experian, and CRIF. If you find an error on one, check whether the same error appears on others and dispute across all affected bureaus simultaneously.

Check Your Credit ReportStep 2: Pay Every Due on Time Without Exception

Payment history is the single largest factor in your CIBIL score. This one habit paying every EMI and credit card bill before the due date, every single month does more for your score than everything else combined.

One missed payment can drop your score by 50 to 100 points. Consistent on-time payments, over 12 to 18 months, rebuild it progressively. There is no shortcut around this.

The practical steps:

Set up auto-pay or standing instructions for every EMI. At minimum, set it up for the minimum due amount. Ideally, set it for the full outstanding balance. Put every payment due date in your phone calendar with a reminder 5 days in advance. Do not wait until the due date, process payments 2 to 3 days early to account for banking delays. If cash is tight in a particular month, prioritise EMIs and credit card minimums above discretionary spending. A missed EMI costs far more in score damage than the temporary inconvenience of cutting other expenses.

The effect of consistent on-time payments accumulates. At 6 months, lenders begin to see a positive trend. At 12 months, the score reflects it clearly. At 18 to 24 months, recovery is well underway even from significant damage.

Not sure what is specifically dragging your score down?

Check Your FREED Credit Insights Free.

Check Your ScoreStep 3: Reduce Your Credit Utilisation

Credit utilisation is the percentage of your total available credit limit that you are currently using. It is the second most important factor in your CIBIL score.

If your credit card limit is Rs. 1,00,000 and your outstanding balance at billing time is Rs. 70,000, your utilisation is 70%. Most bureaus and lenders consider anything above 30% a warning signal. High utilisation suggests you are financially stretched and dependent on credit.

Three ways to bring it down:

Pay down existing balances as aggressively as possible. Even reducing utilisation from 70% to 40% produces a noticeable score improvement.

Pay the credit card balance mid-cycle rather than only at the billing date. The balance the bureau records is what shows on your billing statement. If you pay down a significant portion before the statement is generated, the recorded utilisation is lower.

Request a credit limit increase from your bank -- without increasing spending. If your limit goes from Rs. 1,00,000 to Rs. 1,50,000 and your spending stays at Rs. 40,000, your utilisation drops from 40% to 27%. This mechanical reduction improves your score without changing your spending behaviour.

Legal Note

Under RBI guidelines, credit card issuers are required to notify you before any unilateral reduction in your credit limit. If a bank reduces your limit without proper notice, this constitutes a violation. A sudden limit reduction also increases your credit utilisation ratio automatically, which can lower your score. If this happens without notice, you can raise a complaint with the bank's Nodal Officer and the RBI Banking Ombudsman.

Know your rights as a credit card holderStep 4: Stop Applying for Credit Unnecessarily

Every time you apply for a loan or credit card, the lender runs a hard enquiry on your CIBIL report. This is recorded, and each one causes a small drop in your score.

One or two enquiries spread across several months is normal and causes minimal damage. But if you have applied for three or four products in a short period -- perhaps after being rejected and trying again elsewhere, the pattern reads as financial stress to every lender who looks at your report.

The rule is simple: do not apply for any new credit while you are trying to rebuild your score. Every new application is a step backward. Wait until your score has meaningfully recovered and your profile is stronger before seeking new credit.

Checking your own score is a soft enquiry. It has no impact on your score whatsoever. Check it as often as you need to this does not count against you.

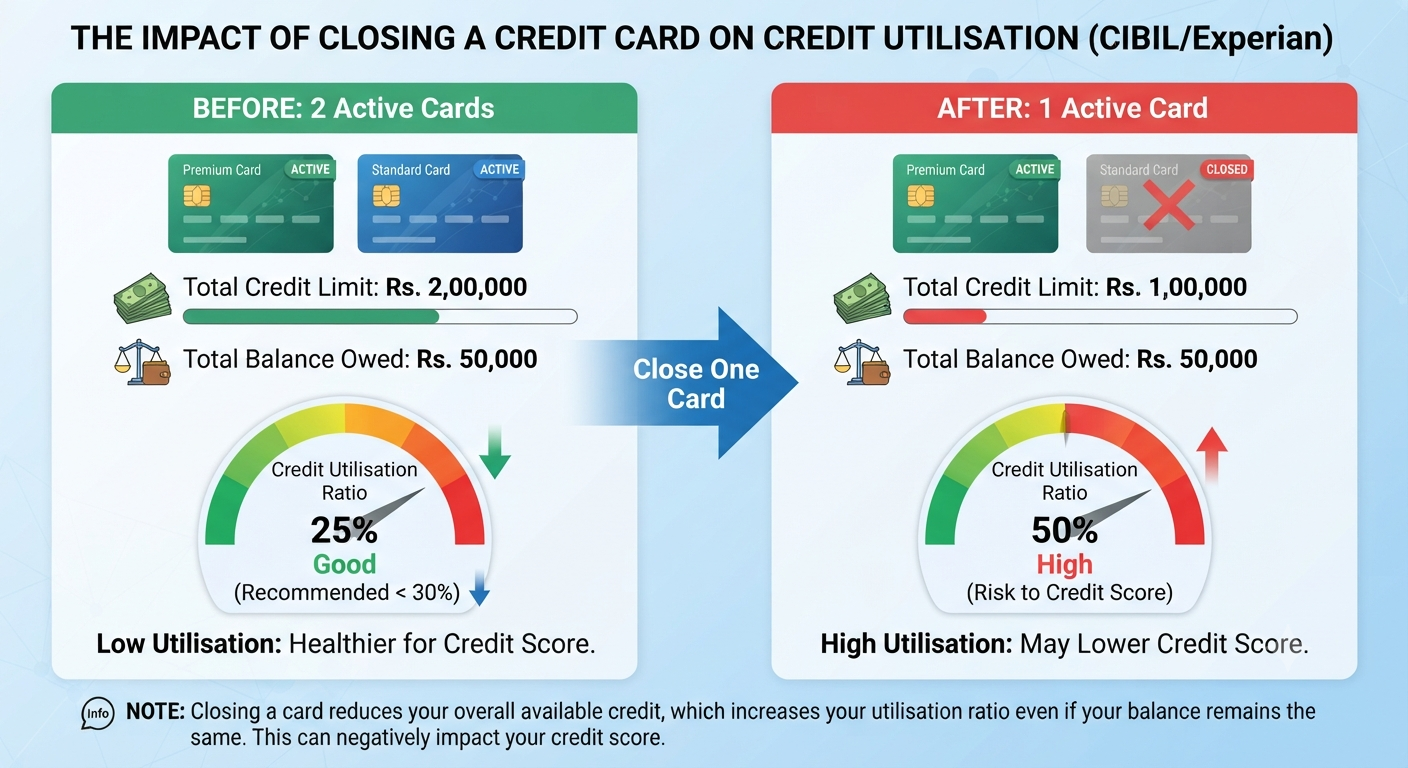

Step 5: Do Not Close Old Credit Accounts

Closing a credit card that you no longer use feels like financial housekeeping. In reality, it can damage your score in two ways.

First, it reduces your total available credit limit. This raises your credit utilisation ratio automatically which can push your score lower even if your spending has not changed.

Second, it shortens your credit age. CIBIL considers how long your accounts have been open. Older accounts with clean histories are valuable because they demonstrate a long track record of responsible behaviour. Closing them removes that history from your profile.

Unless a credit card carries a high annual fee you cannot justify, keep it open. Use it once every few months for a small, planned purchase a utility bill, a grocery order and pay the full amount immediately. This keeps the account active, your credit age intact, and your utilisation ratio healthy.

Step 6: Build a Healthy Credit Mix

Credit bureaus look more favourably on borrowers who demonstrate they can handle different types of credit responsibly both secured loans (home loan, car loan) and unsecured credit (credit cards, personal loans).

A borrower who has only ever used credit cards has a narrower credit profile than one who has managed both a loan and a card responsibly. This difference in credit mix can affect the score, particularly when everything else looks similar.

You do not need to take on unnecessary debt to diversify. If you genuinely need a product a small appliance on no-cost EMI, a two-wheeler loan and can service it without stress, it adds to your credit mix in a positive way. The key is to only take on credit you actually need and can manage, not to borrow purely for the sake of score diversification.

How Long Does It Take to Improve?

There is no universal timeline it depends on how much damage was done and how consistently positive behaviour is maintained. But these are realistic expectations:

1 to 3 months: Score stabilises if the decline is stopped no new missed payments, no new hard enquiries. Does not yet show significant recovery.

3 to 6 months: First visible improvement if all dues are being paid on time and utilisation has been reduced. Lenders begin to see a positive trend.

6 to 12 months: Meaningful score recovery for moderate damage. A score that fell from 720 to 600 can typically get back above 680 with consistent effort in this window.

12 to 24 months: Significant recovery even from serious damage missed payments, defaults, or a settlement. Scores can return to 700 and above for most borrowers who maintain clean behaviour throughout.

24 to 36 months: Full recovery in most cases. The negative marks still exist on the report but their weight diminishes as positive history accumulates on top of them.

The timeline is longer if debt continues to cause problems during the recovery period. A month of on-time payments followed by a missed payment resets progress. Consistency is everything.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

When Debt Is Driving the Score Down

Some borrowers face a situation where improving their score through behaviour alone is not possible because the debt load prevents it.

When EMIs consume 60% or more of monthly income, there is not enough left to pay all dues on time. When credit card balances are maxed out, utilisation cannot be reduced without first reducing the balance. When multiple loan obligations are all competing for the same constrained income, something always falls through.

In these situations, improving the CIBIL score requires first addressing the debt -- not just managing individual habits.

FREED helps people in exactly this position. Through Debt Consolidation, we combine multiple high-interest obligations into one lower monthly payment that is actually manageable within the borrower's income. Through Debt Resolution, we help settle outstanding dues for less than the full amount, with proper documentation to support credit report correction afterward.

Both approaches reduce the financial pressure that is causing the score to fall, creating the conditions where behavioural improvement can actually work.

Over 60,000 Indians have used FREED to get out of this cycle. The first conversation is always free.

Is debt making it impossible to improve your score?

Let FREED address the root cause. Talk to a FREED Expert Free, no pressure.

Connect NowFREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions