Understanding the Grace Period for Credit Card Payments

Learn how to use the credit card grace period to your advantage. Avoid interest charges and manage your payments smartly to enjoy interest-free credit and maximise rewards.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

The grace period is the interest-free window between your billing cycle end date and your payment due date - usually 20 to 50 days in India.

You only get the grace period if you paid your previous month's bill in full. Even one month of partial payment cancels it.

Paying only the minimum due does NOT preserve your grace period interest is charged on the remaining balance immediately.

Cash advances on your credit card have zero grace period interest starting from the very first day you withdraw.

If you've already lost your grace period and debt is spiraling, FREED can help you explore settlement or consolidation options.

What is the Grace Period on a Credit Card?

The grace period is a free window of time that your credit card gives you.

During this window you can use your credit card and pay the bill later without paying any interest. The bank is essentially giving you a short-term, interest-free loan.

Think of it this way. You swipe your card on June 5th for ₹10,000. Your billing cycle ends on June 30th. Your payment due date is July 20th. If you pay the full ₹10,000 by July 20th, you paid zero interest. The bank gave you 45 days of free credit.

That's the grace period. And when used properly it is one of the most powerful features of a credit card.

But when misused or misunderstood it becomes the starting point of a debt spiral that can take years to recover from.

How Long is the Grace Period in India?

Most credit cards in India offer a total interest-free period of 20 to 50 days.

This total includes:

The billing cycle - typically 28 to 31 days. This is the period during which all your purchases are recorded.

The payment window - typically 15 to 20 days after the billing cycle ends. This is the time you have to pay the full bill.

Component | Typical Duration |

Billing cycle | 28–31 days |

Payment window after billing cycle | 15–20 days |

Total interest-free period | 20–50 days depending on when you swipe |

The actual interest-free days you get on any purchase depend on when in the billing cycle you swipe. A purchase made on the first day of the billing cycle gets the maximum interest-free days. A purchase made on the last day gets only the payment window - usually 15–20 days.

How Does the Grace Period Work? - A Simple Example

Let's walk through a real example so this is crystal clear.

Your credit card details:

- Billing cycle: June 1 to June 30

- Payment due date: July 20

- Last month's bill: Paid in full by June 20

Scenario: You swipe your card on June 5 for groceries - ₹3,000. You swipe again on June 20 for a phone case - ₹800. Your total bill for June: ₹3,800.

If you pay the full ₹3,800 by July 20 - you pay zero rupees in interest. That's 45 days of free credit on the June 5 purchase, and 30 days on the June 20 purchase.

Now the critical condition - this only works because you paid your May bill in full. If you had carried any balance from May - interest would start accruing on your June purchases from day one. No grace period at all.

When Do You Lose the Grace Period?

You lose your grace period the moment you do not pay the full outstanding balance by the due date.

This happens in two ways:

Way 1 - You pay only the minimum due The statement shows: Total Amount Due ₹15,000. Minimum Amount Due ₹750.

You pay ₹750. You think the grace period is protected. It is not.

The remaining ₹14,250 carries forward with full interest - at 36–42% annually. And your new purchases in the next cycle also attract interest immediately. No more free window.

Way 2 - You miss the due date entirely Even one day late means a late fee plus interest on the full outstanding. And your grace period is gone for the next cycle too.

Once you lose the grace period - getting it back requires paying the full outstanding balance across one or more complete billing cycles. Until then, every new purchase is interest-bearing from day one.

FREED Expert Tip

Set up auto-debit for the full statement amount - not just the minimum due. This one habit protects your grace period permanently, eliminates late fees, and keeps your CIBIL score healthy. Takes 10 minutes to set up with your bank. It is the single most impactful thing you can do with a credit card.

Talk to a FREED CounsellorThe Minimum Due Trap - Why It's the Biggest Mistake

This deserves its own section because it catches so many people off guard.

Your credit card statement shows two numbers every month:

Total Amount Due - what you actually owe Minimum Amount Due - usually 5–10% of the total

The minimum amount is designed to keep your account "active" and avoid an immediate late fee. That's it. It is not designed to help you manage your debt responsibly.

Here's what happens when you only pay the minimum:

Outstanding | Minimum Paid | Interest Added Next Month | Your Progress |

₹30,000 | ₹1,500 (5%) | ₹900 (36% annual) | Outstanding reduces by only ₹600 |

₹60,000 | ₹3,000 (5%) | ₹1,800 | Outstanding reduces by only ₹1,200 |

₹1,00,000 | ₹5,000 (5%) | ₹3,000 | Outstanding reduces by only ₹2,000 |

At this rate - clearing ₹1,00,000 of credit card debt by paying only the minimum takes over 10 years. And you end up paying almost ₹3,00,000 in total - three times the original amount.

And throughout all of this - you have no grace period. Every new purchase attracts immediate interest.

Always pay the full amount due. If you cannot - pay as much above the minimum as possible. Every extra rupee accelerates your journey out.

Cash Advances - No Grace Period, Ever

This is one of the least understood features of credit cards.

When you withdraw cash using your credit card at an ATM - that is called a cash advance. And it has absolutely no grace period.

Interest starts from the very first day - the day you withdraw. At rates of 36–42% per year, sometimes even higher specifically for cash advances.

You also get charged a cash advance fee - typically 2.5–3% of the amount withdrawn, with a minimum of ₹250–₹500.

Example: You withdraw ₹10,000 from an ATM using your credit card. Cash advance fee: ₹300 (charged immediately) Daily interest: approximately ₹10–₹12 per day By the time your statement comes - you've already paid ₹300 in fees plus ₹150–₹200 in interest.

Never use your credit card for cash advances except in a genuine emergency where absolutely no other option exists.

What the Law Says

Under RBI guidelines, credit card issuers must clearly disclose the interest rate, grace period terms, minimum payment requirements, and all fees in your card agreement and on every monthly statement. If your bank is not clearly showing you how interest is calculated on your outstanding balance - or is not disclosing the loss of grace period on partial payments - that is a violation of RBI's transparency guidelines. You have the right to ask your bank for a full written explanation of how your charges are calculated.

Talk to a FREED CounsellorHow to Protect and Maximise Your Grace Period

Follow these three habits and your grace period will work hard for you every month:

Habit 1 - Always pay the full statement amount, not the minimum. Not a partial amount. The full outstanding balance. Every month. On time. This is the only way to keep your grace period active and your interest cost at zero.

Habit 2 - Set up auto-debit for the full amount Human memory is unreliable. Life gets busy. You forget. One missed payment = late fee + lost grace period + CIBIL score damage. Auto-debit for the full statement amount removes all of this risk completely.

Habit 3 - Never use your card for cash advances This immediately kills the grace period on that amount and triggers immediate interest plus fees. Use your debit card or UPI for cash needs instead.

Bonus Habit - Time your big purchases smartly If you have a large purchase planned - try to make it at the start of your billing cycle rather than the end. A purchase on June 1st (with a July 20th due date) gives you 50 days interest-free. The same purchase on June 29th gives you only 21 days. Same card, same purchase - 29 extra free days by just timing it right.

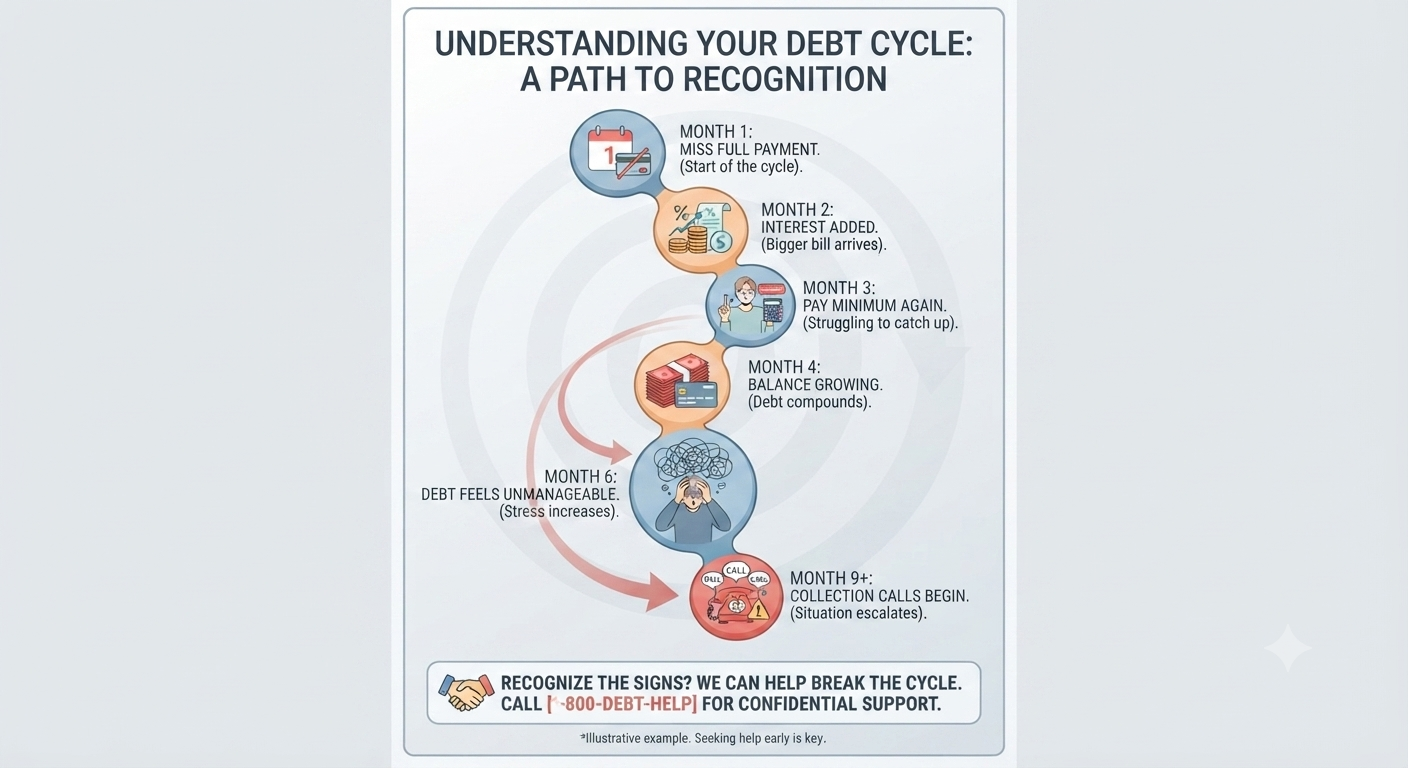

What Happens When the Debt Starts Spiralling?

Losing the grace period once is recoverable. Pay the full balance next month and it's back.

But for many people - one lost grace period leads to carrying a balance. The balance attracts interest. The interest makes the bill bigger. The bigger bill is harder to pay in full. So they pay the minimum again. The cycle repeats.

Month after month - the outstanding grows. The interest compounds. The stress builds. Eventually, the debt feels completely unmanageable.

This is the path from one missed full payment to a full credit card debt crisis. It moves slowly at first - and then very quickly.

If you find yourself in this situation right now - you are not alone. And there are real options available.

When to Get Help

If your credit card outstanding has been growing for several months despite making regular payments - the grace period alone won't fix the problem.

At that stage, you need a structured plan.

If you can still pay but the bills are overwhelming - Debt Consolidation. FREED can combine all your credit card dues into one lower EMI at a reduced interest rate. One payment. One date. Less total interest.

If you've already defaulted and genuinely cannot pay in full - Debt Settlement. FREED can negotiate with your bank to settle your credit card debt for less than what you owe. On average, clients settle at 56% less than their original outstanding.

If recovery agents are calling - FREED Shield. Activate FREED Shield instantly at freed.care/freed-shield. Our team takes over all creditor communication and handles any harassment immediately.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions