How to Remove a Settlement Remark from CIBIL: A Step-by-Step Gu

The "Settled" remark on your CIBIL report cannot be erased by an agent, a paid service, or a dispute alone. There is one legal path to removing it, and several things you can do while waiting for it to age out. Here is the complete, honest picture.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

A "Settled" remark on the CIBIL report means the account was closed by paying less than the full outstanding amount. It stays on the report for up to 7 years from the date of first default.

The only legal way to change "Settled" to "Closed" is to pay the remaining balance that was waived at the time of settlement, obtain an NOC from the lender, and have the lender update the bureau.

No agent, no paid credit repair service, and no dispute process can remove a legitimate "Settled" remark without full repayment. Claims to the contrary are false and often fraudulent.

If the remark is genuinely incorrect, meaning you paid in full but the report still shows "Settled," that is an error that can and must be disputed with the bureau.

While the remark exists, consistent positive financial behaviour rebuilds the score progressively. Most people cross 700 within 24 to 36 months of sustained good behaviour after settlement.

What the "Settled" Remark Actually Means

When a loan or credit card is settled, meaning the lender accepted a negotiated lump sum less than the full outstanding as complete and final payment, the account is closed with the status "Settled" on the CIBIL report.

This is distinct from "Closed," which indicates the account was fully repaid and closed in good standing.

The "Settled" status signals to any lender reviewing the report that the borrower did not repay the full amount. Lenders treat this as a risk indicator. Home loans and vehicle loans from major banks become difficult to obtain with a recent settlement. Personal loans are possible but at higher rates. Credit card applications may be declined or approved with lower limits.

The remark stays on the report for up to 7 years from the date of the first default, not the date of settlement. An account that first defaulted in February 2023 and was settled in August 2024 will have the negative history visible until early 2030, regardless of when the settlement occurred.

The score impact of the "Settled" remark is real and significant. But it is not permanent, and it is not the only thing that determines creditworthiness. Lenders also look at recent payment behaviour, current utilisation, and the overall trajectory of the credit profile.

Why It Cannot Simply Be Removed

This is the most important thing to understand about the "Settled" remark: it is not a mistake. It is an accurate record of what happened. Because it is accurate, the normal dispute process cannot remove it.

Credit bureau disputes work by identifying information that is incorrectly recorded and requesting correction. A "Settled" remark on an account that was genuinely settled is not incorrect. The bureau is accurately reporting what the lender reported. There is nothing to dispute about the status itself.

What this means in practice: anyone offering to "remove your CIBIL settlement record" for a fee, without full repayment of the remaining balance, is either describing something illegal or is simply taking money without delivering results. These services are fraudulent. They cannot do what they claim. The CIBIL bureau only updates account status when instructed by the reporting member institution (the bank or NBFC). And institutions only update "Settled" to "Closed" when the remaining balance is paid.

The One Legal Way to Change "Settled" to "Closed"

The only way to legally change a "Settled" status to "Closed" on a CIBIL report is to pay the balance that was waived at settlement, obtain written confirmation from the lender, and have the lender instruct the bureau to update the account status.

This requires two things to be feasible: the funds to pay the remaining balance, and the lender's cooperation in accepting the payment and updating the bureau.

Not every lender will accept the remaining balance after a settlement has been completed. The settlement was a final agreement. Some lenders may decline further payment on an already-settled account. Others will accept it, particularly if approached with a clear request and the funds to pay.

The correct approach is to contact the lender formally, ask specifically what amount would be needed to upgrade the account status from "Settled" to "Closed," and obtain this confirmation in writing before making any payment.

Step-by-Step: How to Do It

Step 1: Pull your credit report.

Get the full credit report from the official CIBIL website or FREED Credit Insights. Identify every account marked as "Settled," noting the lender name, account number, and the outstanding balance shown at the time of settlement.

Step 2: Calculate the remaining balance.

The remaining balance is the amount that was waived at settlement, meaning the original total outstanding minus what was paid. This figure may be on the original settlement letter. If not, contact the lender for a current statement of account.

Step 3: Contact the lender in writing.

Write formally to the bank's customer service, Nodal Officer, or settlements department. State the account number and settlement date. Ask specifically: "What amount would be required to upgrade this account's status from 'Settled' to 'Closed' on the credit bureau?" Request the response in writing.

Step 4: Negotiate if possible.

Some lenders will accept the principal portion of the waived amount without requiring the full original outstanding (including all waived interest and charges). This is not guaranteed but worth requesting. The request should be specific: "I would like to pay the remaining principal amount to upgrade the account status to Closed."

Step 5: Make the payment after receiving written confirmation.

Once the lender confirms in writing what amount is required and that payment will result in the status being updated to "Closed," make the payment through the specified channel. Keep the payment receipt.

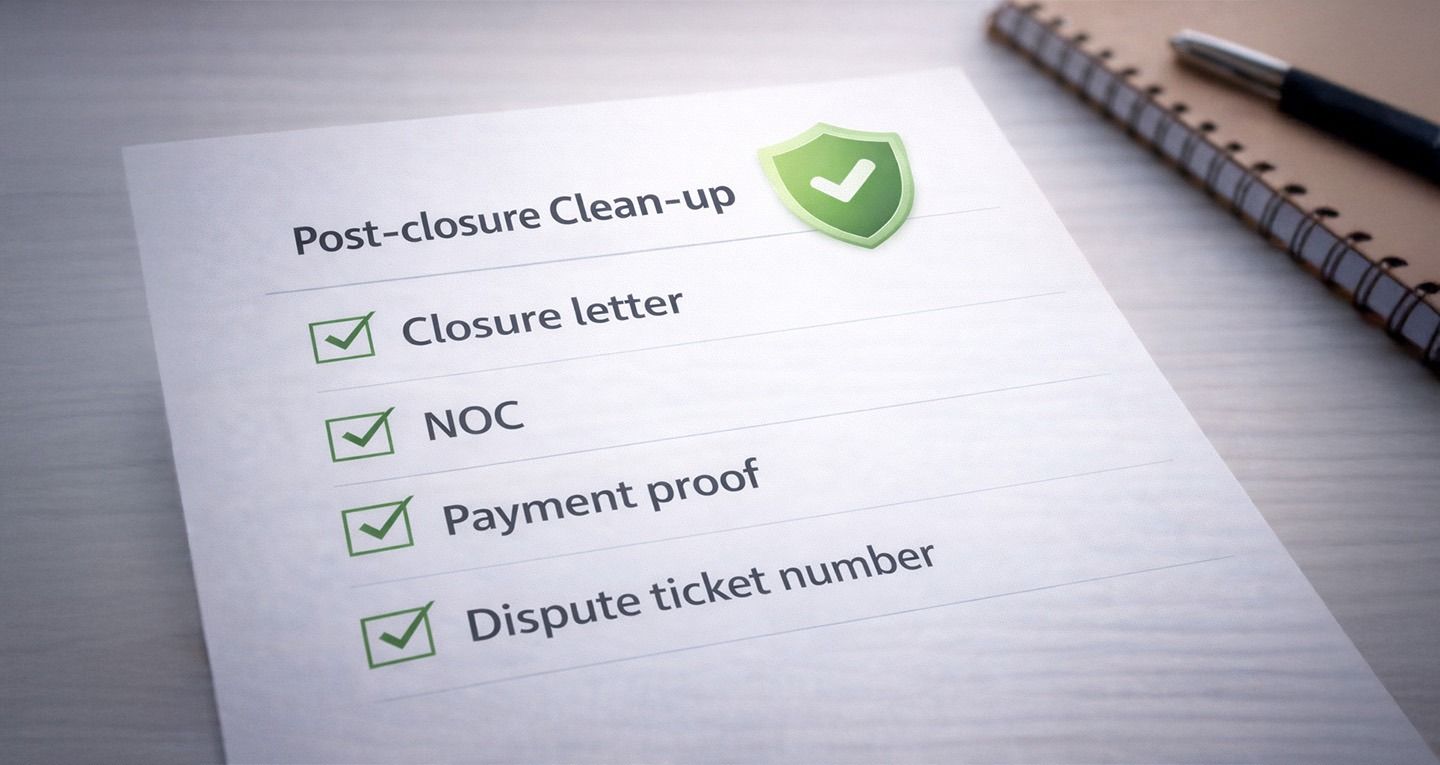

Step 6: Obtain the No Objection Certificate (NOC).

After payment, request a No Objection Certificate from the lender, confirming the account is now fully paid with no remaining dues. This document confirms that the lender has no further claim on the account.

Step 7: Confirm the bureau update.

Request written confirmation from the lender that the bureau update instruction has been sent. Under RBI guidelines, lenders are required to update credit bureaus within 30 days of a status change. If the update does not appear within 45 days, raise a formal dispute with CIBIL referencing the NOC and payment receipt.

Step 8: Check the report 30 to 45 days later.

Pull the credit report again to confirm the status has been updated to "Closed." If it still shows "Settled" despite full payment and the NOC, raise a formal dispute with CIBIL through their official dispute portal.

What to Do If You Cannot Pay the Remaining Balance

For many people who settled a loan, the reason they settled in the first place was genuine financial hardship. Paying the remaining balance to upgrade the status is simply not feasible at this point.

This is the more common situation. And the honest answer is: if the remaining balance cannot be paid, the "Settled" status will remain for up to 7 years from the date of first default. There is no workaround. But there is still meaningful progress available.

The score impact of the remark is not fixed. It is heaviest in the first one to two years after settlement and diminishes progressively as positive history accumulates on top of it. By year three or four, with consistent positive behaviour, most people find their score has recovered to a level where major credit products become accessible again, even with the "Settled" remark still visible.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

How to Rebuild Your Score While the Remark Exists

The "Settled" remark does not prevent score improvement. It is one negative factor among several, and its weight diminishes over time as positive factors accumulate.

Pay every active obligation on time, every month. Payment history is the highest-weighted factor. Twelve consecutive on-time payments on any active obligation, however small, build a positive trend that lenders can see alongside the settlement remark.

Keep credit card utilisation below 30%. If any credit card is active, keeping the balance below 30% of the limit demonstrates controlled credit usage that counteracts the settlement remark's negative signal.

Get a secured credit card. A secured credit card (issued against a fixed deposit) is accessible after settlement and builds positive payment history from the first month. Use it for small purchases. Pay in full every month. Within 12 months, meaningful positive history is visible on the report.

Avoid new hard enquiries. Every rejected credit application adds a hard enquiry and makes the profile worse. Wait until the score has recovered to a level where approval is likely before applying for unsecured credit.

Check the report every six months. Confirm that no new errors have appeared, that active accounts are being reported correctly, and that the positive behaviour is reflecting in the score trajectory.

Fraud Warnings: Services That Claim to Remove It Instantly

This section is important. There are many individuals and services in India that advertise the ability to remove CIBIL settlement remarks quickly, for a fee. These services are almost universally fraudulent.

No service can instruct a credit bureau to remove or change an accurate account record without the reporting lender's instruction. The bureau takes its update from the member institution (the bank). The bank only instructs an update when the borrower has paid the remaining balance and the account is legitimately closeable.

Any service claiming to remove a legitimate settlement record without full repayment, through "special contacts," "internal access," "legal loopholes," or any other mechanism is making a false claim. People who pay these services typically receive nothing of value and may have provided sensitive financial information to fraudulent operators.

The correct process is exactly as described above: pay the remaining balance, obtain the NOC, and have the lender instruct the bureau to update. There is no other legal path.

About FREED

FREED is India's leading debt resolution platform. We have helped over 60,000 Indians reduce, manage, and completely get out of debt, legally and without harassment.

We also help people understand and rebuild their CIBIL score after resolution through FREED Credit Insights, bureau dispute support, and step-by-step rebuilding guidance.

Your first consultation is always free. No hidden charges. No judgment.

Visit freed.care

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions