Your go-to resource for financial wellbeing

Your resource for financial wellbeing

Our Latest Blogs

Latest Blogs

Debt Management

Small Steps Big Changes : Setting Realistic New Year Goals for Debt Relief

New Year resolutions about debt rarely stick because they are too big and too vague. Here is how to set realistic, achievable debt relief goals for the year ahead, broken into small steps that actually compound into real financial change.

By FREED India | 3 August 2026

Debt Management

Top 10 benefits of good credit score

Explore the key benefits of a good credit score, from lower interest rates to quick loan approvals. Know how a strong CIBIL score works in your favour.

By FREED India | 3 August 2026

Debt Management

How Do Multiple Credit Cards Affect Your Credit Score?

Have two or three credit cards and wondering if that is hurting your CIBIL score? The answer depends entirely on how you manage them. Here is a simple, honest breakdown of what multiple cards do to your score — for better and for worse

By FREED India | 3 August 2026

Recommended Reads

Debt Management

Small Steps Big Changes : Setting Realistic New Year Goals for Debt Relief

By FREED India | 3 August 2026

Debt Management

Top 10 benefits of good credit score

By FREED India | 3 August 2026

Debt Management

How Do Multiple Credit Cards Affect Your Credit Score?

By FREED India | 3 August 2026

Debt Management

6 Reasons Why Your Credit Score Is Not Increasing

By FREED India | 3 August 2026

Debt Management

Debt Management Plan vs Debt Settlement: What's the Difference?

By FREED India | 3 August 2026

Debt Management

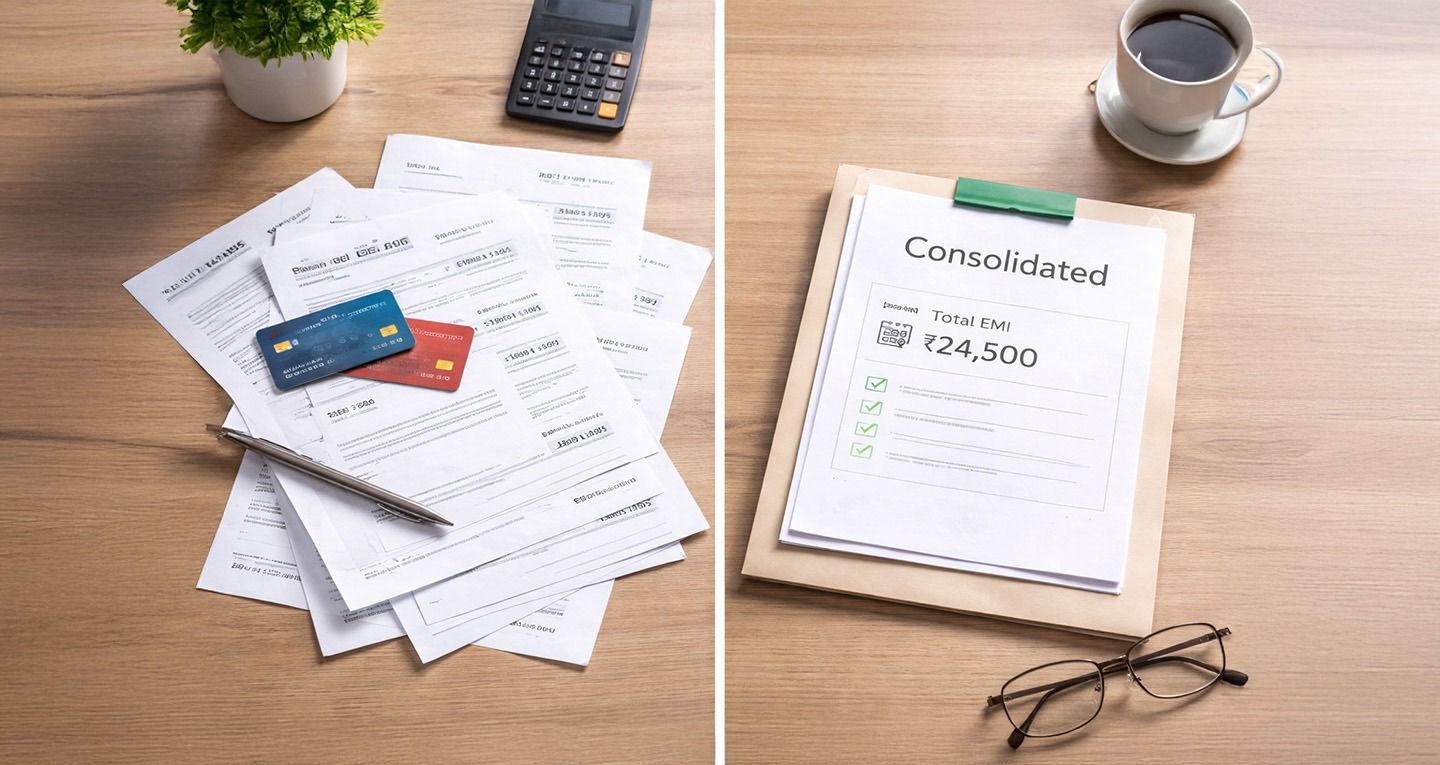

What is debt consolidation and how it helps reduce monthly financial stress

By FREED India | 3 August 2026

Debt Management

Financial Discipline: The First Step Towards a Secure Financial Future

By FREED India | 3 August 2026

Debt Management

Avoid These Common Credit Card Mistakes

By FREED India | 3 August 2026

Debt Management

Does Debt Relief Affect Your Credit Score?

By FREED India | 3 August 2026