5 Reasons Debt Relief Programs Are Actually Worth It Especially in India

Drowning in EMIs and don't see a way out? A debt relief program might be exactly what you need. Here's why thousands of Indians are choosing it and why it might be right for you too.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

A debt relief program helps you pay off debt in a structured, manageable way, often with reduced interest or negotiated settlements.

It is designed for people who are genuinely struggling, not those who just want to avoid paying.

The biggest benefit: it stops the cycle of debt growing faster than you can pay it.

It also gives you protection from aggressive recovery agents.

FREED's debt relief program has helped thousands of Indians get their life back.

What Is a Debt Relief Program?

A debt relief program is a structured plan that helps you get out of debt. It is not magic. It is not a scam.

It is a real process where an expert team works with you and sometimes directly with your lenders to find the best way to clear your debt.

This could mean:

- Negotiating a lower interest rate with your bank

- Combining multiple loans into one single payment

- Creating a month-by-month payoff plan based on your actual income

- In some cases, negotiating a partial settlement, but only when it makes sense

Think of it as having a financial expert in your corner, someone who knows how the system works and fights for your side.

Want to know if a debt relief program is right for you?

Talk to a FREED Expert for free. No pressure. No judgement. Just honest answers.

Connect with a FREED Expert- It's FreeWho Is It Actually For?

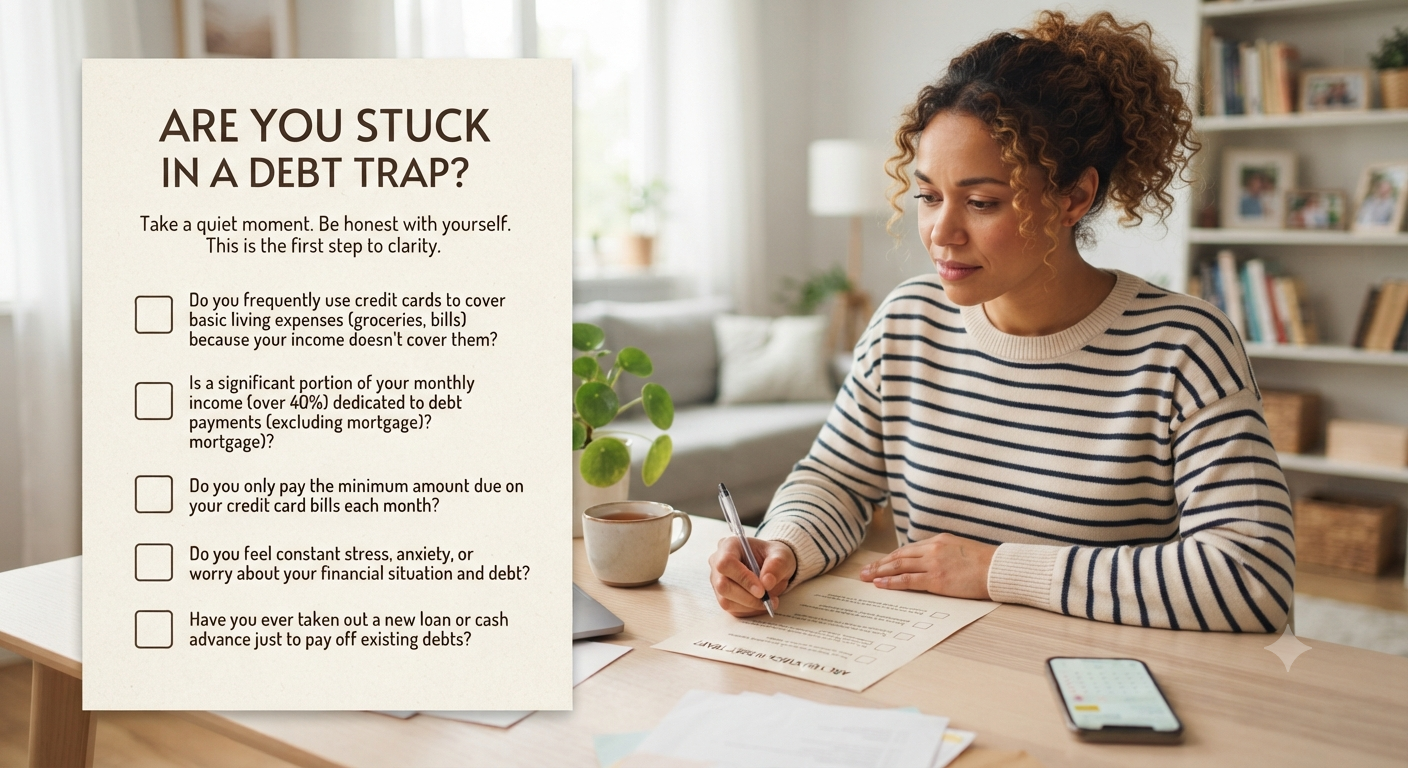

Debt relief programs are not just for people who are completely broke.

They are for anyone who feels like their debt is out of control.

Ask yourself:

Are your total EMIs more than 40-50% of your monthly income?

Do you use one credit card to pay another?

Are you getting calls from recovery agents?

Does it feel like no matter how much you pay, the debt doesn't reduce?

Have you stopped sleeping well because of money stress?

If you said yes to even two of these, a debt relief program is worth exploring.

You don't need to have hit rock bottom to ask for help.

Reason 1- It Stops Your Debt From Growing

This is the most important reason. And most people don't realise it until it's too late.

Here's the truth about debt in India:

Personal loans carry 12-24% interest per year. Credit cards carry 36-42% interest per year.

If you are only paying the minimum amount every month, your principal is barely moving. The interest keeps piling up.

Example: You owe ₹3,00,000 on a credit card at 40% annual interest. You pay ₹5,000 every month. At this rate, you will never fully pay it off. The interest is growing faster than your payment.

A debt relief program stops this cycle.

It negotiates lower interest, freezes penalties in some cases, and creates a payment structure where your debt actually goes down every month.

FREED Expert Tip

"If your total EMIs are eating up more than 50% of your salary every month, you are already in the danger zone. Don't wait for things to get worse. The earlier you act, the more options you have."

Reduce Your Monthly EMIsReason 2- One Simple Payment Instead of Many

Managing multiple debts is exhausting.

One personal loan EMI. One car loan. Two credit card bills. A loan from a friend. Maybe a gold loan too.

Different due dates. Different amounts. Different banks calling you.

It is mentally draining, even before you talk about the money.

A debt relief program, especially one that includes debt consolidation, brings all of this into one single monthly payment.

One amount. One date. One place.

This alone reduces stress significantly. It also reduces the chance of accidentally missing a payment, which protects your credit score.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

Reason 3- It Protects You From Harassment

If you have missed EMIs, you already know what recovery calls feel like.

Early morning calls. Late night messages. Calls to your family members. Agents showing up at your home or office.

It is humiliating. And a lot of it is illegal.

When you enrol in a debt relief program, a few things happen:

First, your program provider communicates directly with your lenders on your behalf.

Second, lenders are notified that you are working on a structured repayment, which reduces aggressive recovery activity.

Third, you get to understand your legal rights, what agents can and cannot do.

You stop being a scared person who doesn't pick up calls. You become someone with a plan, a team, and legal protection.

What the Law Says

RBI guidelines clearly state that recovery agents cannot call before 8 AM or after 7 PM. They cannot use abusive language, threaten you, or contact your employer or family members to pressure you. If they do, you can file a complaint with the RBI Banking Ombudsman. This is your legal right. Read about how to take action against loan recovery harassment.

Know Your RightsReason 4- It Is Faster Than Paying on Your Own

Most people dealing with debt have a rough plan:

"I'll just pay a little extra every month and eventually it'll clear."

The problem? High interest rates make this take years longer than it should.

A debt relief program can shorten your debt-free timeline significantly.

Here is a simple comparison:

Approach | Example Debt | Time to Pay Off |

Minimum payments only | ₹5,00,000 at 20% interest | 12-15 years |

Paying extra on your own | ₹5,00,000 at 20% interest | 6-8 years |

Structured debt relief program | ₹5,00,000 with negotiated rate | 2-4 years |

The difference is not small. It is years of your life.

Years of stress. Years of restricted spending. Years of not being able to plan for your family's future.

A debt relief program compresses that timeline by working smarter, not just harder.

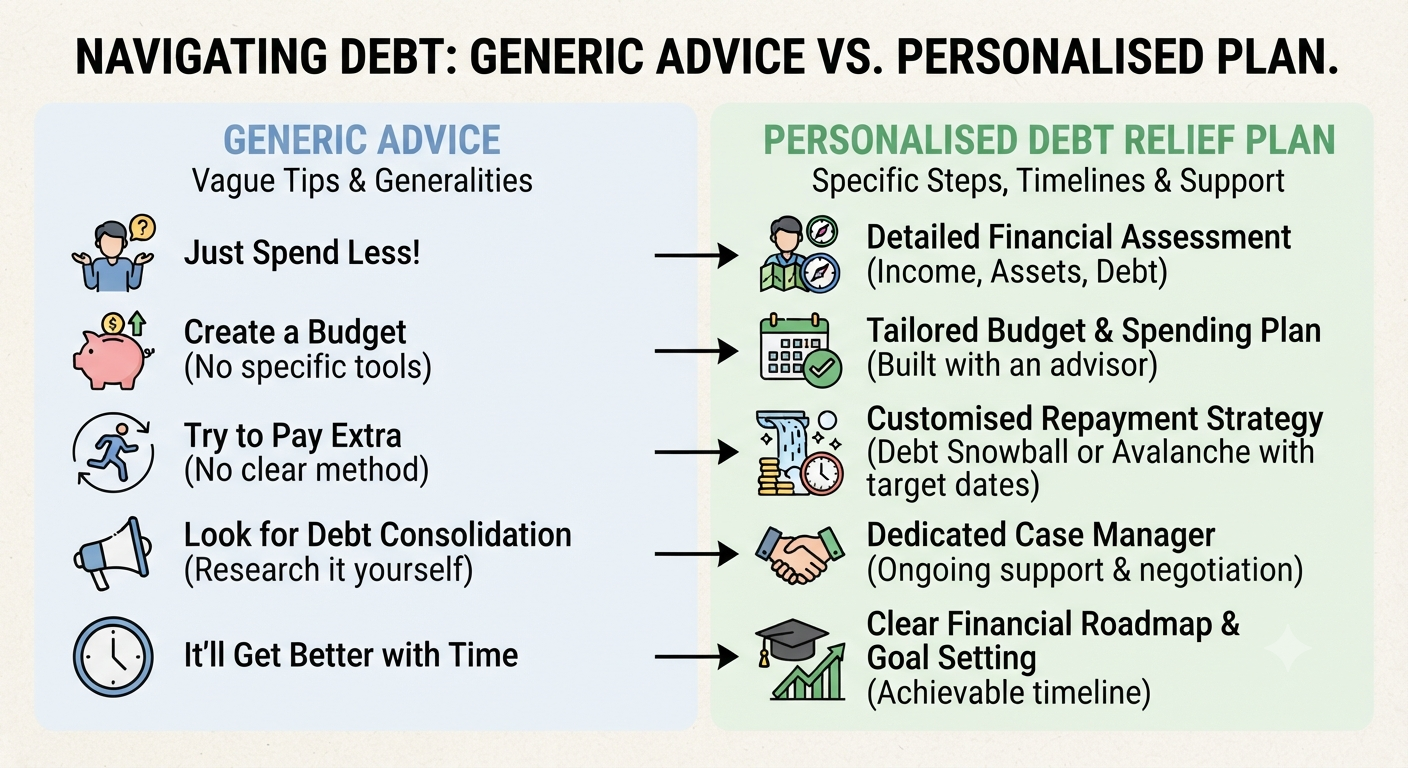

Reason 5- It Gives You a Real Plan, Not Just Advice

Here is something honest:

Reading articles about debt, watching YouTube videos, asking friends, none of it gives you a personalised plan.

Generic advice like "spend less" or "save more" doesn't tell you which loan to pay first, how to talk to your bank, or what to do if you can't make this month's EMI.

A debt relief program gives you exactly that.

A real plan built on your real numbers.

Your income

Your exact debts and interest rates

Your monthly expenses

Your family situation

Everything is factored in. You get a step-by-step roadmap, not motivation posters.

And you have a team behind you every step of the way.

Is There Any Downside?

Honesty matters. So yes, debt relief programs are not perfect for everyone.

Here are things to keep in mind:

It requires commitment. A debt relief program works only if you stick to the plan. If you keep taking new loans or miss the structured payments, it won't work.

It may involve a settlement in some cases. If your debt situation is severe, part of the resolution may involve a negotiated settlement. This can impact your credit score. A good program will always tell you this upfront and explain the trade-offs.

It is not instant. Debt relief takes time, typically 12 to 48 months depending on how much you owe. Anyone who promises to clear your debt in 30 days is lying.

Choose the right program provider. There are genuine platforms, and there are scams. A trustworthy provider will never ask for large upfront fees, will always explain every step, and will not make unrealistic promises.

FREED, for example, is fully transparent about process, timelines, and impact.

Check Where You Stand: FREED Financial Health Score Get a free assessment of your financial health in 2 minutes. See how serious your debt situation is and what the best next step is for your specific case.

Ready to see what a real debt relief plan looks like for your situation?

FREED will assess your debt, your income, and your options- completely free. No hidden charges. No obligation. Just clarity.

Get Your Free Debt Assessment from FREEDFREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions