Bank Loan Recovery Rules: What Banks Can and Cannot Legally Do

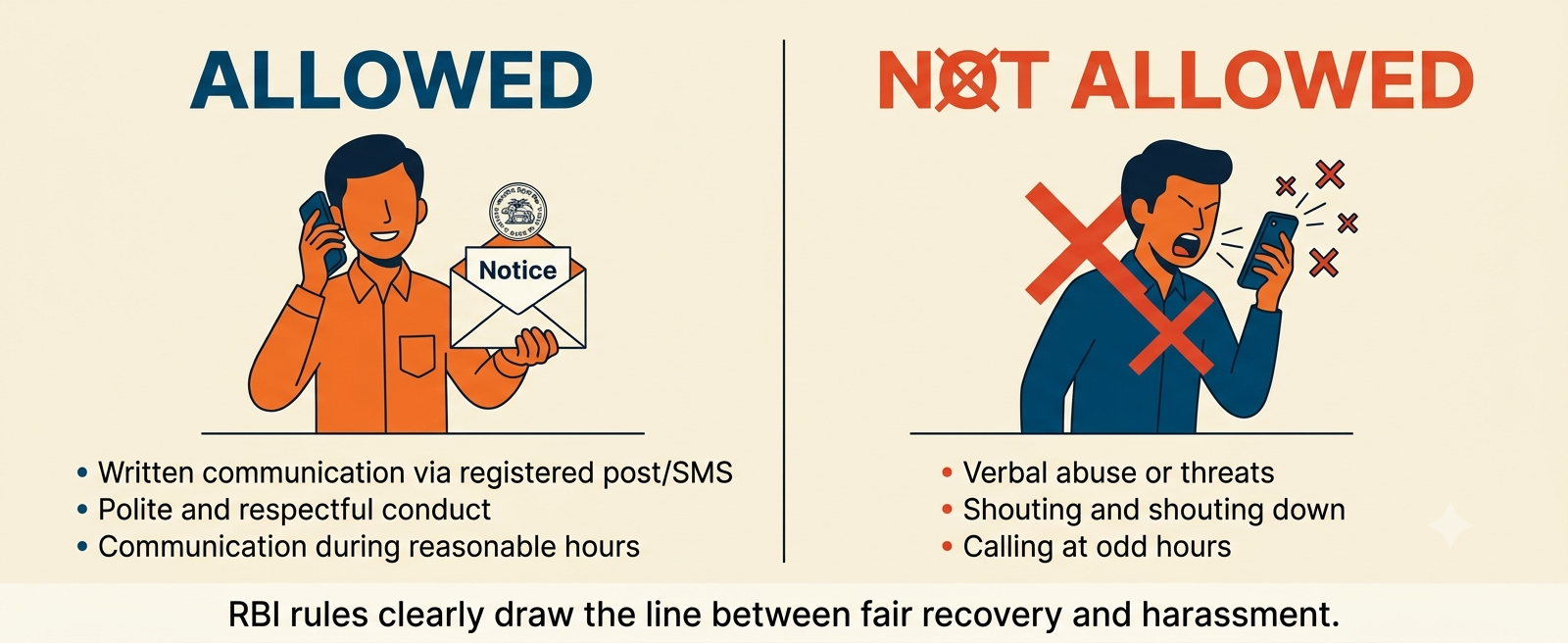

Banks can legally call, send notices & visit your home for loan recovery, but they cannot threaten, abuse, harass, or contact you outside 8AM–7PM. If the line is crossed, report it to the RBI Banking Ombudsman immediately.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

Bank loan recovery is governed by RBI rules. Every bank and NBFC must follow them.

Recovery agents cannot call before 8 AM or after 7 PM. They cannot abuse, threaten, or shame you.

For unsecured loans (credit card, personal loan, BNPL), banks cannot seize property without a court order.

Banks can file a civil case, send a legal notice, or report your default to CIBIL. They cannot take the law into their own hands.

If recovery turns abusive, you can file a complaint with the RBI Ombudsman, the police, or your bank's nodal officer.

What Are Bank Loan Recovery Rules?

Bank loan recovery rules are the legal guidelines set by the Reserve Bank of India (RBI) that every bank and NBFC (non-bank financial company) must follow when recovering a defaulted loan. They cover how recovery agents can behave, what banks can and cannot do, and what rights you have as a borrower.

These rules exist for one reason: to make sure that when a borrower misses payments, the process of getting that money back stays fair and human. These rules are designed to ensure recovery stays professional and respectful.

These rules apply to every regulated bank, every NBFC, and every fintech lender including loan apps registered with the RBI. If a loan provider is registered in India and lends to Indian borrowers, they must follow these rules. All regulated lenders are expected to follow these RBI guidelines.

What Banks CAN Legally Do for Loan Recovery

Banks have real and legal tools to recover money you owe. Here is what they are allowed to do.

Banks can send you written reminders about missed EMIs. These come by post, SMS, and email. They are legal and expected.

Banks can call you to discuss repayment but only between 8 AM and 7 PM. A polite call asking about your situation or offering a payment arrangement is allowed.

Banks can appoint a registered recovery agent to follow up on your account. That agent must carry a valid ID card issued by the bank. They must follow the same rules as the bank itself.

Banks can send you a legal notice through a lawyer. This notice formally demands repayment and usually gives you a window of around 60 days to respond. Receiving a legal notice is serious but it is not a court summons.

Banks can report your default to credit bureaus like CIBIL, Experian, and CRIF. Once reported, your credit score drops and future loan approvals become harder. This generally happens once the account crosses 90 days of missed payments.

Banks can file a civil case in court to recover the amount you owe. This is the last step in the process and happens only after other efforts have failed.

What Banks CANNOT Legally Do for Loan Recovery

This is where RBI rules draw a clear line. If any of the following has happened, the conduct may violate RBI recovery guidelines.

Cannot call before 8 AM or after 7 PM. Calls outside this window may violate RBI recovery guidelines. Save the record date, time, number and you have grounds to complain.

Cannot use abusive language, threats, or intimidation. Shouting, cursing, threatening physical harm, or using language meant to scare you is not allowed under any circumstances.

Cannot contact your family, employer, or neighbours about your loan without your written permission. Your loan is between you and the bank. It cannot be used as a weapon against the people around you.

Cannot visit your home without prior intimation. An unannounced visit especially at night or early morning is not allowed. Any visit must follow written notice.

Cannot seize your property, salary, or belongings without a court order. For unsecured loans (credit cards, personal loans, BNPL), the bank has no right to touch your assets unless a court has issued an order. Recovery agents cannot seize unsecured assets without legal process. Any agent who threatens to "take your things" is lying.

Cannot publicly shame you. Posting your name, photo, or personal details on social media, WhatsApp groups, or physical posters in your locality is illegal and actionable.

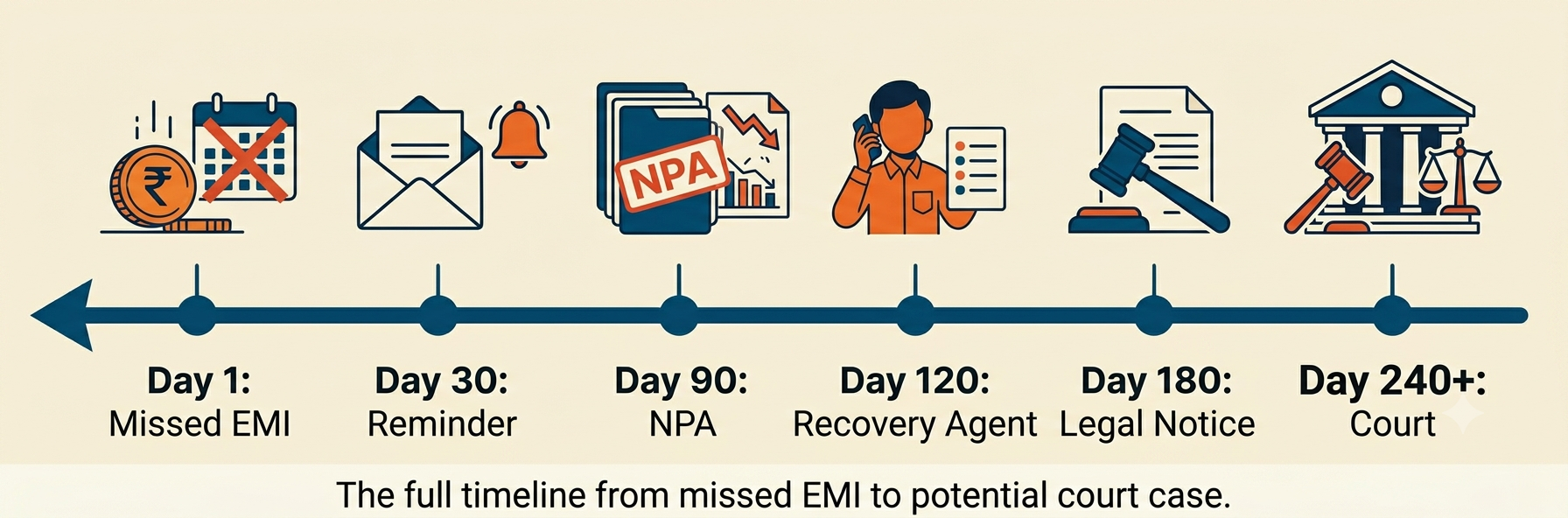

How Does the Bank Loan Recovery Process Work?

Step 01: You Miss an EMI The bank marks your account as overdue and sends a reminder by SMS or call.

Step 02: Bank Sends Repeated Reminders SMS, calls, and emails follow over the next 30 to 60 days.

Step 03: Account Marked as NPA After 90 days of missed EMIs, the loan is marked as a bad loan (NPA loan marked as bad by the bank after 90 days of missed payments).

Step 04: Recovery Agent Steps In The bank may assign a registered agent who must follow the same RBI rules as the bank.

Step 05: Legal Notice Sent A lawyer-issued notice gives you a final repayment window, usually around 60 days.

Step 06: Civil Suit or Settlement If unpaid, the bank may file a civil case in court or open the door to a settlement discussion.

What Are Your Rights as a Borrower During Loan Recovery?

RBI rules do not just restrict what banks can do. They give you specific rights. Know them.

- You have the right to be treated with dignity, no abuse, no shaming, no threats.

- You have the right to receive recovery contact only between 8 AM and 7 PM.

- You have the right to privacy. The bank cannot call your family or workplace about your loan.

- You have the right to receive a written notice before any legal action is taken against you.

- You have the right to dispute incorrect dues in writing and ask the bank to verify the amount before paying.

- You have the right to ask your bank for a settlement or change in repayment plan if paying in full has become genuinely difficult.

- You have the right to file a complaint with the RBI Ombudsman at cms.rbi.org.in free of charge, no lawyer needed.

FREED Expert Tip

If a recovery agent ever raises their voice or visits your home without notice, record the date, time, and what was said. Keeping records can support an RBI Ombudsman complaint if needed.

Talk to a FREED counsellor for freeWhen Can a Bank Take You to Court for Loan Recovery?

Banks usually move to court only after the loan has been overdue for several months and other recovery efforts have failed. For unsecured loans, credit cards, personal loans, and BNPL (buy-now-pay-later) products the bank files a civil suit asking the court to order repayment. This is a civil matter, not a criminal one, in most cases.

There is one exception: cheque bounce. If you issued a cheque that bounced, the bank can file a case under Section 138 of the Negotiable Instruments Act (the cheque bounce law- this can turn criminal). This is one situation where legal proceedings may involve criminal provisions in addition to civil recovery. One important note: SARFAESI (a law that lets banks seize property) applies only to secured loans like home loans or car loans. It does not apply to personal loans, credit cards, or BNPL.

What the Law Says

Under the RBI Fair Practices Code and the 2022 Master Direction on Outsourcing, recovery agents must identify themselves with a bank-issued ID, maintain dignified conduct, and avoid contact with anyone other than the borrower. Violation can lead to RBI action against the bank. You can file a complaint at cms.rbi.org.in free of charge.

Read the full RBI Fair Practices CodeAllowed vs. Not Allowed in Bank Loan Recovery

Banks ARE Allowed To

Call between 8 AM and 7 PM only

Send written reminders, SMS, email

Appoint a registered recovery agent with a valid ID

Visit your home but only after written intimation

Report your default to credit bureaus

File a civil case in court for money recovery

Banks Are NOT Allowed To

Call before 8 AM or after 7 PM

Use abusive, threatening, or shameful language

Contact your family, friends, or employer without permission

Show up at your door unannounced

Seize property, salary, or items without a court order (for unsecured loans)

Post your name, photo, or details on social media or WhatsApp

How to Respond if Bank Recovery Crosses the Line

Step 01: Stay Calm and Don't Argue Recovery agents try to provoke. A calm tone keeps the law on your side.

Step 02: Note Down Every Detail Date, time, agent name, what was said. Save SMSes and call recordings immediately.

Step 03: Write to the Bank's Nodal Officer First Every bank has one. Their email is published on the bank's official website.

Step 04: Escalate to the RBI Ombudsman If the bank does not respond in 30 days, file at cms.rbi.org.in it is free.

Step 05: File a Police Complaint if Threatened Threats, abuse, or physical visits at odd hours qualify as criminal conduct.

Step 06: Ask for a Resolution Plan A settlement or change in your repayment plan can stop the recovery chain entirely.

How FREED Helps You Handle Bank Loan Recovery

When recovery calls are happening and the pressure is building, having someone in your corner changes everything. FREED's counsellors handle the back-and-forth with your bank, help put your documents together, and work out a proper resolution plan so you don't have to face it alone.

Settlement is not something a borrower chooses out of preference. Banks and financial companies only consider it when you are in a genuine financial difficulty and are truly unable to repay the full amount. It is a last resort, not a shortcut.

Where settlement is the right step, FREED helps work with your banks to bring down your total debt by up to 50%* without you having to take any new loan. Where it isn't, FREED helps with changing your repayment plan, combining loans, or getting a short repayment break first.

Not sure if your bank's recovery action is legal? One free call with a FREED counsellor. Clear answers. No pressure. No judgment.

About FREED

FREED is India's first Loan Management Platform, founded in 2020 and based in Gurugram.

60,000+ Indians Helped | ₹3,200 Cr+ Debt Managed | 15,000+ Accounts Settled | 4.7★ Google Reviews

FREED negotiates settlements on unsecured loans like credit cards, personal loans, BNPL products, and loan apps on behalf of enrolled customers. Fees are charged only on successful settlement. FREED does not handle secured loans.

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions