The 50-30-20 Budget Rule: The Simplest Way to Take Control of Your Money

Not sure where your salary disappears every month? The 50-30-20 rule is the simplest budgeting framework that exists - and it works even on a modest income. Here is how to use it starting this month.

FREED India

Reviewed by FREED India, Debt Resolution Specialists

Key Takeaways

The 50-30-20 rule divides your take-home income into three simple buckets - 50% for needs, 30% for wants, and 20% for savings and debt repayment.

It is not a rigid formula. It is a starting framework. The percentages can be adjusted based on your income, life stage, and debt situation.

If your EMIs and loan repayments are already consuming more than 50% of your income, the budget rule alone will not fix the problem. The underlying debt needs to be addressed first.

Building the savings habit - even with a small amount - is more important than the percentage. Rs 500 saved consistently every month is better than an ambitious saving target that is never met.

FREED helps people whose debt burden makes a balanced budget impossible - through consolidation, settlement, or counselling.

What is the 50-30-20 Rule?

The 50-30-20 rule is a budgeting framework created by US Senator Elizabeth Warren and her daughter Amelia Warren Tyagi in their book All Your Worth. It has since become one of the most widely recommended personal finance tools globally - because it is simple, flexible, and works for most income levels.

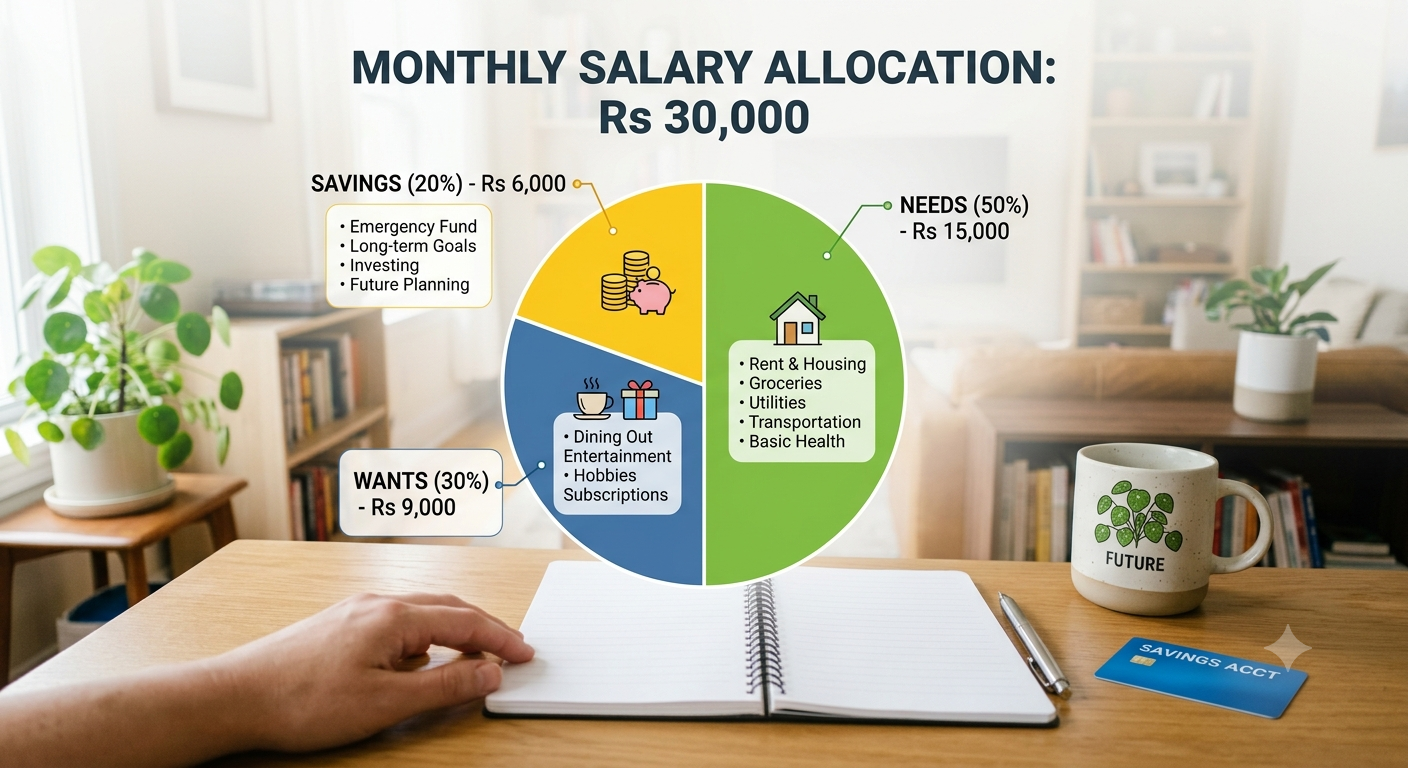

The idea is straightforward. Take your monthly take-home salary - after all deductions - and divide it into three parts:

50% goes to Needs - the things you must pay for to live and work.

30% goes to Wants - the things that make life enjoyable but are not essential.

20% goes to Savings and Debt Repayment - the part that builds your future.

That is the entire rule. No complicated spreadsheets. No tracking every single rupee. Just three buckets - and a conscious decision about how much goes into each one.

EMIs consuming most of your salary with nothing left to save?

Talk to a FREED Expert for free - we will help you reduce the burden so budgeting becomes possible.

Connect with FREED ExpertThe 50% - Needs

Needs are expenses you cannot avoid. They are non-negotiable obligations that would seriously disrupt your life if not paid.

What belongs in the Needs bucket:

Rent or home loan EMI. Food and groceries. Electricity, water, and other utilities. Phone and internet bills needed for work. School fees and child-related essential expenses. Any loan EMIs - personal loan, car loan, education loan. Health insurance premiums. Transportation costs to and from work.

What does not belong here: streaming subscriptions, eating out, shopping, entertainment, gym memberships. Those go in Wants.

For a person earning Rs 30,000 per month, the Needs bucket is Rs 15,000. If rent is Rs 7,000, groceries Rs 4,000, utilities Rs 1,000, and an EMI of Rs 3,000 - that is exactly Rs 15,000. The budget works.

The challenge arises when EMIs alone consume Rs 12,000 to Rs 15,000 out of a Rs 30,000 salary. At that point, the 50% bucket is already full before rent and food are paid. This is a debt problem - not a budgeting problem - and it needs a debt solution.

The 30% - Wants

Wants are the expenses that make life enjoyable but are not strictly necessary for survival or work.

What belongs in the Wants bucket:

Eating out and food delivery. Movies, concerts, and entertainment. Streaming subscriptions - Netflix, Prime, Hotstar. Gym membership. Shopping for clothes beyond essentials. Holidays and weekend trips. Gadgets and electronics upgrades. Hobbies and recreational activities.

The important distinction: a want is something where a free or cheaper alternative exists. You need food - but eating at a restaurant is a want because you can cook at home. You need a phone - but upgrading to the latest model every year is a want.

The 30% allocation for wants is not a permission to spend freely. It is a boundary. Once the wants bucket is full for the month - the spending stops. Any wants that exceed 30% push into the savings bucket - which is where most people quietly rob from without realising it.

For a Rs 30,000 salary, the Wants bucket is Rs 9,000 per month. That is Rs 300 per day. Enough for a comfortable life if managed thoughtfully - not enough for an unplanned, untracked lifestyle.

FREED Expert Tip

Track your wants spending for one month before applying the 50-30-20 rule. Most people find wants eating up 40-50% of income - not 30%. Real numbers make the adjustment easier to stick to.

Know moreThe 20% - Savings and Debt Repayment

This is the most important bucket - and the one most people neglect.

The 20% is split between two purposes:

Building savings - emergency fund, investments, retirement planning.

Paying off debt - any extra payment above the minimum due on loans and credit cards.

For a Rs 30,000 salary, the Savings bucket is Rs 6,000 per month.

The order of priority within this 20% matters. Emergency fund first - until you have at least 3 months of essential expenses saved. Then high-interest debt repayment - paying above the minimum on credit cards and personal loans. Then longer-term savings and investments.

The single most important rule within this bucket: pay yourself first. On the day your salary arrives, transfer the savings amount to a separate account before spending on anything else. Not whatever is left at the end of the month - that is usually zero. The first transfer of the month goes to savings.

How to Apply the Rule on a Low Income

The 50-30-20 rule is often criticised as being designed for higher incomes. On Rs 15,000 to Rs 20,000 per month, 50% barely covers rent and food - leaving little room for the other buckets.

The adjustment for lower incomes:

Start with 70-20-10 instead of 50-30-20. 70% for needs, 20% for wants, 10% for savings. Even saving 10% consistently builds a real foundation.

Or start even smaller - 80-15-5. Save just 5%. Rs 750 on a Rs 15,000 salary. The amount is less important than the habit.

The wants bucket shrinks significantly at lower incomes - and that is fine. The framework is flexible. What matters is that savings always get their allocation first - not whatever is left over after everything else.

As income grows, shift the percentages gradually. An income increase of Rs 3,000 per month: put Rs 1,500 into savings and Rs 1,500 into the lifestyle. Never increase wants in direct proportion to income increases.

What to Do When EMIs Are Already Above 50%

This is the situation FREED most commonly encounters.

A person earning Rs 35,000 per month with three loan EMIs totalling Rs 20,000. Before rent, food, or utilities are paid, 57% of income is already committed to loan repayments. The 50-30-20 rule does not apply - because there is no room to apply it.

In this situation, a budgeting framework is not the solution. The debt itself is the problem.

Two paths forward:

Debt Consolidation - if the CIBIL score is still above 650. FREED combines all loans into one lower EMI through lending partners. The consolidated EMI is lower than the combined current EMIs - freeing up cash that makes the 50-30-20 framework applicable again.

Debt Resolution - if payments have already been missed and full repayment is not realistic. FREED negotiates with lenders to settle for less than what is owed. On average, clients settle at 56% less. The debt is closed, the EMI burden ends, and the budget can finally be rebuilt.

Once the debt burden is reduced to a manageable level - ideally below 30% of income - the 50-30-20 rule becomes a powerful tool for staying out of debt going forward.

What the Law Says

Under RBI guidelines, banks must assess a borrower's repayment capacity before approving any loan - including checking that the total EMI burden does not exceed a reasonable proportion of monthly income. This is called the Fixed Obligation to Income Ratio (FOIR). Most banks cap this at 40 to 50% of monthly income. If you were approved for a loan that pushed your EMIs above this level - or if your circumstances have changed since the loan was approved - you have the right to approach your bank and ask about restructuring options. Restructuring is a legitimate, documented process - not a favour.

Enroll NowCommon Mistakes When Using the 50-30-20 Rule

Counting wants as needs. EMIs belong in needs because they are fixed obligations. But a streaming subscription is a want - not a need. Be honest about which bucket each expense truly belongs in.

Saving what is left over rather than saving first. If savings happen last, they almost never happen. Pay yourself first - move the savings amount on salary day, before any other spending.

Setting too aggressive a savings target. Aiming for 30% savings on a Rs 20,000 salary when rent alone takes 40% is unrealistic and leads to abandoning the system entirely. Start where you realistically can - and increase gradually.

Not adjusting the percentages to your life stage. Someone with young children and a home loan has different need ratios than a single professional. The 50-30-20 is a starting point - adjust it to fit your reality.

Giving up after one bad month. One month of overspending on wants does not mean the system does not work. It means one month was harder than usual. Reset and continue.

Are You in a Loan Trap? Quick Check

Move the slider to your total EMIs as a % of monthly salary. See your debt stress level instantly.

EMIs as % of Monthly Salary

FREED is India's trusted loan management platform. Founded in 2020 and headquartered in Gurugram, FREED has counselled 20 lakh+ people on personal loans, credit cards, and app loans. FREED charges fees only on successful settlement, not upfront. FREED does not handle secured loans (home loans, car loans, gold loans).

Media Mentions